McEwen Copper announces results of an updated Preliminary Economic Assessment (PEA) on a copper leaching phase of development at the Los Azules project in San Juan, Argentina

The PEA includes an updated independent mineral resource estimate, which increased to 10.9 billion (B) lbs. Cu (Indicated, grade 0.40%) and 26.7 B lbs. Cu (Inferred, grade 0.31%)

Base Case Highlights (Open-pit, Heap Leach, SX/EW, Nameplate capacity of 175 ktpa Cu Cathodes):

- Average annual copper (Cu) cathode production of 401 million lbs. (182,100 tonnes) during the first 5 years of operation, and 322 million lbs. (145,850 tonnes) over the 27-year life of the mine (LOM)

- Total Cu recoverable to cathode of 8.68 billion lbs. (3.94 million tonnes), based on the LOM extraction of mineralized material containing approximately 11.90 billion lbs. of total Cu (5.40 million tonnes), and average copper recovery of 72.8%

- After-tax net present value (NPV8%) of $2.659 billion(1), internal rate of return (IRR) of 21.2%, and a payback period of 3.2 years – at $3.75 per lb. Cu.

- Initial capital expenditure of $2.462 billion, and a project capital intensity of $7.66 per lb. Cu ($16,880 per tonne Cu)(2)

- Average C1(2) cash costs of $1.07 per lb. Cu and all-in sustaining costs(2) of $1.64 per lb. Cu (AISC Margin of 56%)(2)

- Average EBITDA(3) per year of $1.101 billion (Years 1-5) and $692 million (Years 6-27)

- Estimated carbon intensity of 670 kg CO2 equivalent per tonne of Cu (CO2-e/t Cu)(4) for Scope 1&2 GHG Emissions, well below the industry average of 1,980 kg CO2-e/t Cu(5). McEwen Copper’s goal at Los Azules is to be carbon neutral by 2038, a target which is achievable through the use of emerging technologies and offsets

- Estimated site-wide water consumption of 137 liters per second (L/s) from years 1 to 10, increasing to 163 L/s from years 11 to 27, this compares to approximately 600 L/s(6) for a conventional mill producing copper concentrate

- 1.182 billion tonnes of mineralized material placed on heap leach pad with in-situ total copper grade of 0.46% and in-situ soluble copper grade of 0.31%(7)

TORONTO, June 20, 2023 (GLOBE NEWSWIRE) -- McEwen Mining Inc. (NYSE: MUX) (TSX: MUX) is pleased to provide results of the updated Preliminary Economic Assessment (the “2023 PEA”) on the Los Azules Copper Project in San Juan Argentina (the “Project”). Los Azules is 100% owned by McEwen Copper Inc., which is 52% owned by McEwen Mining.

The 2023 PEA Technical Report is prepared in accordance with the requirements set forth by Canadian National Instrument 43-101 (“NI 43-101”) for the disclosure of material information and is intended to meet the requirements of a Preliminary Economic Assessment (PEA) level of study and disclosure as defined in the regulations and supporting reference documents. The effective date of the report is May 9, 2023. All currency shown in this report is expressed in Q1 2023 United States Dollars unless otherwise noted.

This study is preliminary in nature and includes 26% inferred mineral resources in the conceptual mine plan. Inferred mineral resources are considered too speculative geologically and in other technical aspects to enable them to be categorized as mineral reserves under the standards set forth in NI 43-101. There is no certainty that the estimates in this PEA will be realized.

Study Contributors

The 2023 PEA technical report was prepared by Samuel Engineering Inc., with contributions from Knight Piésold Consulting, Stantec Consulting International Ltd, McLennan Design, Whittle Consulting Pty Ltd, and SRK Consulting UK Limited under the supervision of David Tyler, McEwen Copper Project Director. The 2023 PEA technical report has been filed on SEDAR and on the Company’s website: https://www.mcewenmining.com/investor-relations/reports-and-filings/default.aspx

2023 PEA vs 2017 PEA

The base case development strategy selected in the 2023 PEA is distinctly different from that presented in the prior PEA published in 2017. In 2017, the strategy was to construct a mine with a conventional mill and flotation concentrator producing a concentrate for export to international smelters. The 2023 PEA proposes a heap leach (leach) project using solvent extraction-electrowinning (SX/EW) to produce copper cathodes (LME Grade A) for sale in Argentina or international markets. There are three principal reasons why the implementation strategy was changed to leach in the 2023 PEA:

- Environmental Footprint: Fresh water consumption is reduced by approximately 75% (150 vs. 600 L/s). Electricity consumption is reduced by approximately 75% (57 vs. 230 MW). GHG emissions are reduced by approximately 57% (670 vs. 1,560 CO2-e/t Cu Scope 1&2), with paths to further reductions by implementing new technologies, with the goal of reaching net-zero carbon by 2038 with some offsets. Los Azules copper cathodes will thus be attractive to end-users seeking to measurably reduce their upstream environmental impacts.

- Reduced Permitting Risk: When proposing any mega-project development, it is vital to understand the local standards and sensitivities around permitting. The Project uses technology (heap leach) that is in operation in San Juan today. It also eliminates tailings and tailings dams, conserves scarce water resources, and reduces the overall complexity of the mine, optimizing the permitting process.

- Producing Cathodes: The leach process produces LME Grade A copper cathodes, which can be directly used in industry, including within Argentina reducing export taxes. This eliminates reliance on 3rd party foreign smelters for the processing of concentrates into refined copper products. It also eliminates significant GHG emissions associated with transportation, and pollution associated with smelting. Counterparty and pricing risks are also reduced.

McEwen views the progress made with the 2023 PEA towards reducing our environmental footprint and greater environmental and social stewardship sets the Project apart from other potential mine developments, which appropriately justifies certain economic trade-offs. The primary trade-offs to achieve these environmental benefits is lower overall copper recovery, slightly higher unit costs, and less immediate cashflow due to extended leach cycles. Nevertheless, the leach project remains very robust. Furthermore, McEwen believes that some of these drawbacks can be mitigated by implementing developing technologies such as Nuton™, discussed below.

Property Description

The Los Azules deposit is a classic Andean-style porphyry copper deposit. The large hydrothermal alteration system is at least 5 kilometers (km) long and 4 km wide and is elongated in a north-northwest direction along a major structural corridor. The Los Azules deposit area is approximately 4 km long by 2.2 km wide and lies within the alteration zone. The limits of the mineralization along strike to the North and at depth have not yet been defined. Primary or hypogene copper mineralization extends to at least 1,000 meters (m) below the surface. Near surface, leached primary sulfides (mainly pyrite and chalcopyrite) were redeposited below the water table in a sub-horizontal zone of supergene enrichment as secondary chalcocite and covellite. Hypogene bornite appears at deeper levels together with chalcopyrite. Gold, silver, and molybdenum are present in small amounts, but copper is the economic driver at Los Azules.

A New Vision and Approach

We developed regenerative guiding principles to reframe the approach to sustainable innovation and set forth high-reaching goals that explore all facets of the mining processes considered for Los Azules. The project development seeks to significantly reduce the environmental footprint of mining operations and their associated GHG emissions by integrating the latest renewable and environmentally responsible technologies and processes. The Project aims to obtain 100% of its energy from renewable sources (wind, hydro, and solar) in a combination of offsite and onsite installations. The Project is also seeking to have long-term net positive impacts on the greater Andean ecosystem, local flora and fauna, the lives of miners, and of the other citizens of nearby communities, while contributing positively to the local and national economy of Argentina. Refer to the full 2023 PEA Technical Report for more information about our regenerative approach.

Metal Price Assumption

The copper price use in the 2023 PEA was $3.75 per pound (except for the mineral resource estimate), in line with analysts’ consensus projections for long-term copper prices that range between $3.25 and $4.25 per pound, with a mean price of $3.75 per pound.

Study Highlights

This 2023 PEA development strategy begins with processing of resources associated with the oxide and supergene copper mineralization in the near surface portion of the deposit using heap leaching methods. This approach results in low average C1 costs of $1.07 per lb. Cu ($0.88 per lb. in the first 8 years) and an attractive 3.2-year payback period. Copper cathode production during the first 5 years of operation averages 401 million lbs. per year (182 ktpa), and average over the 27-year LOM is 322 million lbs. per year (146 ktpa).

A nominal copper cathode production capacity of 385 million lbs. per year (175 ktpa) is met or exceeded during the first 11 years of mining and was selected as the Base Case, with a smaller Alternative Case presented at 275 million lbs. per year (125 ktpa) of copper cathodes. The 2023 PEA financial model does not include potential future development phases focused on primary copper mineralization found beneath the supergene copper layer but some of these opportunities are discussed in the report, including the potential of deploying Nuton™ technologies.

The processing facility will function through to the completion of mining in Year 23 with stockpile reprocessing and residual leaching operations to Year 27. Mining operations ramp up over the proposed mine life from approximately 80 million total tonnes per year to 150 million tonnes per year through the life of the project as copper grades decrease, and material movements increase.

Summary results for the Base Case and Alternative Case are provided in Table 1.

| Table 1: Summary Results | |||||||

| Project Metric | Units | Base Case 175 ktpa | Alternative Case 125 ktpa | ||||

| Mine Life | Years | 27 | 32 | ||||

| Tonnes Processed | Billion tonnes | 1.182 | 1.182 | ||||

| Tonnes Waste Mined | Billion tonnes | 1.366 | 1.366 | ||||

| Strip Ratio | 1.16 | 1.16 | |||||

| Total Copper Grade | % Cu | 0.457% | 0.457% | ||||

| Soluble Copper Grade (CuSOL) | % CuSOL | 0.311% | 0.311% | ||||

| Copper Recovery (Total Copper) | % | 72.8% | 72.8% | ||||

| Soluble Copper Recovery(8) | % | 107% | 107% | ||||

| Copper Production (LOM avg.) | tonnes/yr | 145,820 | 123,060 | ||||

| Copper Production (Yr 1-5) | tonnes/yr | 182,100 | 136,100 | ||||

| Copper Production – cathode Cu | ktonnes | 3,938 | 3,938 | ||||

| Initial Capital Cost | USD Millions | $2,462 | $2,153 | ||||

| Sustaining Capital Cost | USD Millions | $2,243 | $2,351 | ||||

| Closure Costs | USD Millions | $180 | $180 | ||||

| C1 Cost (Life of Mine) | USD/lb Cu | $1.07 | $1.11 | ||||

| All-in Sustaining Costs (AISC) | USD/lb Cu | $1.64 | $1.67 | ||||

| Before Taxes | |||||||

| Net Cumulative Cashflow | USD Millions | $15,820 | $15,679 | ||||

| Internal Rate of Return (IRR) | % | 26.5% | 22.9% | ||||

| Net Present Value (NPV) @ 8% | USD Millions | $4,436 | $3,278 | ||||

| After Taxes | |||||||

| Net Cumulative Cashflow | USD Millions | $10,240 | $10,159 | ||||

| Internal Rate of Return (IRR) | % | 21.2% | 18.4% | ||||

| Net Present Value (NPV) @ 8% | USD Millions | $2,659 | $1,929 | ||||

| Pay Back Period | Years | 3.2 | 3.4 | ||||

Sensitivity Analysis

The Base Case project economics are reasonably robust (>15% post-tax IRR) at a copper price above $3.00 per pound and are similarly resistant to an increase in LOM capital expenditure of up to 30% and an increase in operating expenses of up to 60%. Table 2 below shows the sensitivity of the Base Case project economics to the Copper Price (+/- 20%) on a post-tax basis. The project NPV8% is breakeven at a copper price of $2.34 per pound.

| Tables 2: Base Case (175 ktpa) Copper Price Sensitivity | |||||||

| Sensitivity (%) | Metal Pricing | Post-Tax | |||||

| Copper Price | NPV | IRR | Payback | ||||

| $ Cu/lb | $M | % | Years | ||||

| -20%% | $3.00 | $1,277 | 15% | 5.48 | |||

| -15% | $3.19 | $1,624 | 17% | 4.84 | |||

| -10% | $3.38 | $1,969 | 18% | 4.24 | |||

| -5% | $3.56 | $2,314 | 20% | 3.68 | |||

| 0% | $3.75 | $2,659 | 21% | 3.18 | |||

| 5% | $3.94 | $3,003 | 23% | 2.90 | |||

| 10% | $4.13 | $3,346 | 24% | 2.75 | |||

| 15% | $4.31 | $3,689 | 25% | 2.61 | |||

| 20% | $4.50 | $4,032 | 27% | 2.49 | |||

Table 3 below show the sensitivity of the Base Case project economics to initial and sustaining capital expenditure escalation on a post-tax basis.

| Table 3: Base Case (175 ktpa) Initial & Sustaining CAPEX Sensitivity | ||||||

| Sensitivity (%) | Post-Tax | |||||

| NPV | IRR | Payback | ||||

| $M | % | Years | ||||

| 0 | $2,597 | 21% | 3.18 | |||

| 5% | $2,484 | 20% | 3.54 | |||

| 10% | $2,372 | 19% | 3.94 | |||

| 15% | $2,260 | 18% | 4.25 | |||

| 20% | $2,148 | 17% | 4.56 | |||

| 25% | $2,036 | 17% | 4.88 | |||

Table 4 below show the sensitivity of the Base Case project economics to operating expenditure escalation on a post-tax basis.

| Table 4: Base Case (175 ktpa) OPEX Sensitivity | ||||||

| Sensitivity (%) | Post-Tax | |||||

| NPV | IRR | Payback | ||||

| $M | % | Years | ||||

| 0 | $2,597 | 21% | 3.18 | |||

| 5% | $2,496 | 21% | 3.28 | |||

| 10% | $2,396 | 20% | 3.38 | |||

| 15% | $2,295 | 20% | 3.49 | |||

| 20% | $2,195 | 19% | 3.62 | |||

| 25% | $2,095 | 19% | 3.75 | |||

Capital Costs Estimates

The Project includes the development of an open pit mine with muti-stage crushing and screening, a heap leach pad, and a copper solvent extraction-electrowinning (SX/EW) facility with a nominal production capacity of 175 ktpa copper cathodes. There is also a sulfuric acid plant and other associated infrastructure to support the operations. Initial capital infrastructure for the Base Case includes the following facilities:

- Mine development and associated infrastructure

- Coarse rock storage and handling (crushing, conveying, agglomeration)

- Heap leach pads and conveyor stacking systems

- SX/EW facility

- Sulfuric acid plant

- On-site utilities and ancillary facilities including a construction camp

- Off-site infrastructure: power transmission line (outsourced), access roads, and permanent camp

The project initial capital costs are based on budgetary quotes for major equipment, recent in-house cost information and installation factors, and regional contractor inputs and facilities obtained between Q4 2022 and Q1 2023. The capital costs for the project are summarized in Table 5 and should be viewed with the level of accuracy expected for a preliminary analysis.

The approximate construction cost of the 132 kV power supply line to site is $155 million and has not been included in the capital estimate because it is assumed that YPF Luz, a large Argentinean power utility company, will be constructing the line at their expenses pursuant to a long-term renewable power purchase agreement.

| Table 5: Initial Capital Costs by Case | ||||

| Capital Cost | Base Case | Alternative Case | ||

| 175k tpa Cu ($) | 125k tpa Cu ($) | |||

| Mining | $65,600,000 | $65,600,000 | ||

| Ore Storage & Handling | $234,500,000 | $192,500,000 | ||

| Heap Leaching | $158,500,000 | $142,100,000 | ||

| SX/EW Facilities | $250,400,000 | $167,700,000 | ||

| Acid Plant | $94,900,000 | $79,900,000 | ||

| Ancillary Facilities | $23,300,000 | $23,300,000 | ||

| Site Development & Yard Utilities | $126,300,000 | $112,200,000 | ||

| Off-Sites | $167,400,000 | $167,400,000 | ||

| Total Direct Costs | $1,120,900,000 | $950,700,000 | ||

| Common Indirect Costs | $379,200,000 | $323,800,000 | ||

| Owners Costs | $466,700,000 | $455,900,000 | ||

| Subtotal | $1,966,800,000 | $1,730,400,000 | ||

| Contingency | $495,000,000 | $423,100,000 | ||

| Total Capital Cost | $2,461,800,000 | $2,153,500,000 | ||

Operating Costs Estimates

Table 6 summarizes the LOM project operating costs per tonne of material processed and per pound of copper produced.

| Table 6: LOM Cash Costs | ||||

| Base Case 175 ktpa | Alternative Case 125 ktpa | |||

| Description | LOM Cost/tonne ($) | LOM Cost/lb. ($) | LOM Cost/tonne ($) | LOM Cost/lb. ($) |

| Mining | 4.14 | 0.56 | 4.27 | 0.57 |

| Processing | 2.73 | 0.37 | 2.74 | 0.37 |

| General & Administrative | 0.94 | 0.13 | 1.11 | 0.15 |

| Selling Expenses | 0.15 | 0.02 | 0.15 | 0.02 |

| LOM C1 Costs | 7.96 | 1.07 | 8.27 | 1.11 |

Royalties and Taxes

The 2023 PEA includes all government and private royalties on production, export taxes, as well as income taxes and banking taxes. Royalty calculations vary, however royalties and retentions based on net smelter return (NSR) total approximately 9.2%. In the financial model it was assumed that 10,000 tonnes per year of copper cathodes are sold within Argentina and consequently they are not subject to export taxes. 95% of VAT is assumed to be recoverable after two years. A 0.2% portion of the bank tax is recoverable in the following year.

| Table 7: Royalties and Taxes (All Cases) | ||||

| Income Tax | Argentine Corporate Income | % Profit | 35% | |

| VAT Taxes | Argentine Value Added Tax | % on Capital | 10.5% | |

| % on Operating | 21% | |||

| Royalties | San Juan Province | % “Mine Mouth” | 3% | |

| TNR Royalty | % NSR | 0.4% | ||

| McEwen Mining Royalty | % NSR | 1.25% | ||

| Export Retentions | Argentine Export Retention | % NSR | 4.5% | |

| Bank Tax | Debit and Credit Bank Tax | % on Operating | 1.2% | |

Nuton Opportunity

Nuton LLC is a copper heap leaching technology venture of Rio Tinto that became a strategic partner in 2022. Its Nuton™ suite of proprietary technologies provide opportunities to leach both primary and secondary copper sulfides, providing significant opportunity to optimize the mine plan and the overall mining and processing operations. In addition, Nuton™ provides significant other benefits, such as lower overall energy consumption, allowing earlier conversion to renewable energy sources, and lower water consumption than conventional sulfide mineralization treatment processes.

Based on preliminary scoping testing, Nuton™ technologies offer the potential for copper recoveries of more than 80% from predominantly chalcopyrite, depending on the specific mineralogy make-up of the mineral resource. At Los Azules, Nuton™ has the potential to economically process the large primary sulfide copper resource as an alternative to a concentrator, with low incremental capital following the oxide and supergene leach, no tailings requirement, and a smaller environmental footprint. Producing copper cathode with Nuton™ on-site also has the advantage of simplifying outbound logistics for copper concentrates and offers a finished product to the domestic and international market.

The outcomes modelled using the Nuton proprietary computational fluid dynamics model, are very encouraging and indicate that unoptimized copper recovery to cathode from primary material should range from 73% to 79%. Furthermore, Nuton recovery from secondary material is high, ranging from 80% to 86%. This could provide a significant opportunity to optimize the mine plan and the need for selective mining, as simultaneous stacking of both secondary and primary mineralization will not impact on the copper recovery from either material type. Based on the current resource estimate, this could have a significant positive impact on the expected life of the mine, without significantly increasing the initial capital investment required.

Nuton is currently validating modelled data with column leach tests. Column leaching of the composite samples at their facilities is underway and expected to be completed in Q1 2024. Validation of the modelled results could be obtained much sooner, depending on the trends provided by the actual column leach results.

McEwen Copper does not currently have a commercial arrangement with Nuton that enables it to deploy their technologies at Los Azules, and there is no guarantee that such an agreement will come to fruition, however McEwen Copper and Nuton intend to work in good faith toward such an arrangement. The results in Table 8 below assume that Nuton™ technologies are implemented without including costs associated with technology licensing or some other commercial cost structure.

| Table 8: Nuton™ Opportunity Economic Summaries | ||

| Project Metric | Units | Base Case-Nuton 175 ktpa |

| Mine Life | Yr | 39 |

| Strip Ratio | 1.43 | |

| Tonnes Processed | Billion tonnes | 1.737 |

| Copper Grade (Total) | % Cu | 0.409 |

| Copper Production – cathode Cu | ktonnes | 6,411 |

| Initial Capital Cost | USD Millions | $2,444 |

| Sustaining Capital Cost | USD Millions | $2,793 |

| C1 Cost (Life of Mine) | USD/lb Cu | $1.04 |

| All-in Sustaining Costs (AISC) | USD/lb Cu | $1.54 |

| After Taxes | ||

| Internal Rate of Return (IRR) | % | 23.9% |

| Net Present Value (NPV) @ 8% | USD Millions | $3,701 |

| Pay Back Period | Yr | 2.7 |

Project Development Schedule

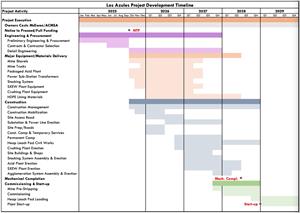

The Gantt chart below presents a conceptual project development timeline based on regional contractor inputs and long-lead equipment and materials delivery assumptions provided by vendors. The schedule assumes that the feasibility study work is completed by the end of 2024, finalization of the environmental permitting process (IIA/DIA) and other necessary permits to begin work are completed during the proposed feasibility study and preliminary timeframe and financing are in place to achieve the scheduled milestones. Following this conceptual schedule, the SX/EW plant start-up could occur in Q1 2029.

McEwen Copper Capital Structure

McEwen Copper is a Canadian-based private company with 28,885,000 common shares issued and outstanding. Its current shareholders are McEwen Mining Inc. 51.9%, Stellantis 14.2%, Nuton 14.2%, Rob McEwen 13.9%, Victor Smorgon Group 3.5%, other management and shareholders 2.3%.

Updated Mineral Resource Estimate

The database for resource estimation has a cutoff date December 31st, 2022. An additional 22,252 m of drilling (mostly infill) from 49 holes, completed in 2023 to date, were not included in the resource estimate.

The mineral resources have been classified according to guidelines and logic summarized within the Canadian Institute of Mining, Metallurgy and Petroleum (CIM 2019) Definitions referred to in NI 43-101. Resources were classified as Indicated or Inferred by considering geology, sampling, and grade estimation aspects of the model. For geology, consideration was given to the confidence in the interpretation of the lithologic domain boundaries and geometry. For sampling, consideration was given to the number and spacing of composites, the orientation of drilling and the reliability of sampling. For the estimation results, consideration was given to the confidence with which grades were estimated as measured by the quality of the match between the grades of the data and the model.

Mineral resources are determined using an NSR cut-off value to cover the processing cost for each recovery methodology. For supergene and primary material using sulfuric acid leaching and SX/EW recovery the cutoff was $2.74/t. The supergene and primary material can be treated in a float mill with NSR cutoffs of $5.46/t and $5.43/t, respectively. NSR values are based on a copper price of $4.00/lb, gold at $1,700/oz, and silver at $20/oz, where applicable. Variable pit slopes between 30° and 42° were applied depending on depth.

The current database is adequate for the preparation of a long-range model that serves as the basis for the 2023 PEA. The extent of mineralization along strike exceeds 4 kilometers and the distance across strike is approximately 2.2 kilometers. The deposit is open at depth and to the North. Over the approximately 2.5 km strike length where mineralization is strongest, the average drill spacing is approximately 150 m to 200 m but there are localized areas where drilling is on 100-m spacing. The assay database includes 56,528 m of assay interval data from 162 drillholes. Resource estimation work was performed using Datamine Studio modeling software.

Resources disclosed in Table 9 are reported in two categories related to processing amenability:

1) materials that are suited for processing in a commercially proven conventional, ambient conditions, copper bio-leaching scheme (Leach); and

2) materials that are better suited to processing either in a more advanced bio-leaching scheme such as Nuton™ technologies or traditional milling/concentrator approach (Mill or Leach+).

| Table 9: Mineral Resource Estimate | ||||||||||

| Million tonnes (MT) | Average Grade | Contained Metal | ||||||||

| Cu% - tot | Cu% - sol | Au (g/t) | Ag (g/t) | Cu (Blbs) | Au (Moz) | Ag (Moz) | ||||

| Indicated | Supergene | Leach | 944.2 | 0.46 | 0.30 | - | - | 9.54 | - | - |

| Mill or Leach+ | 73.0 | 0.13 | - | 0.09 | 1.10 | 0.21 | 0.20 | 2.58 | ||

| Primary | Mill or Leach+ | 218.1 | 0.25 | - | 0.036 | 1.06 | 1.19 | 0.25 | 7.43 | |

| Total | Mill or Leach+ | 291.1 | 0.22 | - | 0.049 | 1.07 | 1.40 | 0.46 | 10.01 | |

| Total Indicated | Leach & Mill or Leach+ | 1,235.3 | 0.40 | 10.94 | 0.46 | 10.01 | ||||

| Inferred | Supergene | Leach | 695.7 | 0.32 | 0.19 | - | - | 4.91 | - | - |

| Mill or Leach+ | 525.6 | 0.30 | - | 0.05 | 1.44 | 3.45 | 0.87 | 24.40 | ||

| Primary | Mill or Leach+ | 3,288.0 | 0.25 | - | 0.03 | 1.18 | 18.35 | 3.37 | 124.67 | |

| Total | Mill or Leach+ | 3,813.6 | 0.26 | - | 0.035 | 1.22 | 21.79 | 4.24 | 149.07 | |

| Total Inferred | Leach & Mill or Leach+ | 4,509.3 | 0.31 | 26.70 | 4.24 | 149.07 | ||||

Table 9 Notes:

- Mineral resources, which are not mineral reserves, do not have demonstrated economic viability. The estimate of mineral resources may be materially affected by environmental, permitting, legal, title, socio-political, marketing, or other relevant factors.

- The quantity and grade of reported inferred mineral resources in this estimation are uncertain in nature and there is insufficient exploration to define these inferred mineral resources as an indicated or measured mineral resource; it is expected that further infill drilling will result in upgrading some of this material to an indicated or measured classification.

- Reasonable prospects of eventual economic extraction are demonstrated by using a calculated NSR value in each block to evaluate an open pit shell using both Indicated and Inferred blocks in Geovia Whittle™ pit optimization software.

- NSR was calculated using the following: metal prices of $4.00/lb for copper, $1,700/oz. for gold and $20/oz. for silver, processing costs of $4.17/t, total freight costs of $150/t, selling costs of $0.02/lb for copper and a constant recovery of 95% applied.

- An NSR cut-off of $2.74/t was used based on extraction of the resource from the enriched zone using sulfuric acid leaching and SX/EW recovery; 100% of the soluble copper and 15% of the non-soluble copper grade is recovered in the heap-leach method.

- The supergene and primary material can potentially be treated in a mill/concentrator with NSR cut-offs of $5.46/t and $5.43/t respectively. This has the added benefit of also recovering the gold and silver present in the resource. Additional parameters are used for the NSR calculation for this scenario.

- Depending on the potential depth of the pit, total pit slope angles ranged from 42° near surface to 32° below 1000m depth. Overburden slopes were set at 30°.

- Composites of 2 m length were capped where needed; the capping strategy is based on the distribution of grade which varies by location (i.e. domain or proximity to controlling structures) and the associated potential metal removal. The resource estimate is based on uncapped copper grades; local capped grades are used for gold and silver.

- Block grades were estimated using a combination of ordinary Kriging and inverse distance squared weighting depending on domain size.

- Model blocks are 20m x 20m x 15m in size.

End Notes:

(1) All dollar amounts are United States Dollars (USD) unless otherwise stated.

(2) Project capital intensity is defined as Initial Capex ($) / LOM Avg. Annual Copper Production (lbs. or tonnes). C1 cash costs per pound produced is defined as the cash cost incurred at each processing stage, from mining through to recoverable copper delivered to the market, net of any by-product credits. All-in sustaining costs (AISC) per pound of copper produced adds production royalties, non-recoverable VAT and sustaining capital costs to C1. AISC margin is the ratio of AISC to gross revenue. Capital intensity, C1 cash costs per pound of copper produced, AISC per pound of copper produced, and AISC margin are all non-GAAP financial metrics.

(3) Annual earnings before interest, taxes, depreciation, and amortization (EBITDA). EBITDA is a non-GAAP financial measure.

(4) Kilograms of Carbon Dioxide Equivalent per tonne of Copper Equivalent produced. Carbon Dioxide Equivalent means having the same global warming potential as any another greenhouse gas.

(5) Wood Mackenzie Limited average Scope 1&2 emissions intensity for 394 assets during the period between 2022 and 2040.

(6) 2017 NI 43-101 Technical Report on Los Azules Project, Hatch Engineering (Throughput of 120,000 tpd of mineralized material).

(7) The sequential assay method used at Los Azules for both the resource assay and metallurgical programs provides an indication of the copper mineralization present in the form of acid soluble copper and cyanide soluble copper, both assays combined provide an approximation for ‘soluble’ copper.

(8) Soluble copper recovery exceeding 100% implies partial leaching of material which was not categorized as “soluble” based on the sequential assaying method and data available.

Qualified Persons

Technical aspects of this news release, excluding mineral resource disclosure, have been reviewed and verified by James L. Sorensen – FAusIMM Reg. No. 221286 with Samuel Engineering, who is a qualified person as defined by National Instrument 43-101– Standards of Disclosure for Mineral Projects.

Disclosure related to the updated Los Azules mineral resource estimate has been reviewed and approved by Allan Schappert, CPG #11758, SME-RM, with Stantec Consulting, who is Qualified Persons as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43- 101”).

CAUTION CONCERNING FORWARD-LOOKING STATEMENTS

This news release contains certain forward-looking statements and information, including "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. The forward-looking statements and information expressed, as at the date of this news release, McEwen Mining Inc.'s (the "Company") estimates, forecasts, projections, expectations or beliefs as to future events and results. Forward-looking statements and information are necessarily based upon a number of estimates and assumptions that, while considered reasonable by management, are inherently subject to significant business, economic and competitive uncertainties, risks and contingencies, and there can be no assurance that such statements and information will prove to be accurate. Therefore, actual results and future events could differ materially from those anticipated in such statements and information. Risks and uncertainties that could cause results or future events to differ materially from current expectations expressed or implied by the forward-looking statements and information include, but are not limited to, effects of the COVID-19 pandemic, fluctuations in the market price of precious metals, mining industry risks, political, economic, social and security risks associated with foreign operations, the ability of the Company to receive or receive in a timely manner permits or other approvals required in connection with operations, risks associated with the construction of mining operations and commencement of production and the projected costs thereof, risks related to litigation, the state of the capital markets, environmental risks and hazards, uncertainty as to calculation of mineral resources and reserves, foreign exchange volatility, foreign exchange controls, foreign currency risk, and other risks. Readers should not place undue reliance on forward-looking statements or information included herein, which speak only as of the date hereof. The Company undertakes no obligation to reissue or update forward-looking statements or information as a result of new information or events after the date hereof except as may be required by law. See McEwen Mining's Annual Report on Form 10-K for the fiscal year ended December 31, 2022, Quarterly Report on Form 10-Q for the three months ended March 31, 2023, and other filings with the Securities and Exchange Commission, under the caption "Risk Factors", for additional information on risks, uncertainties and other factors relating to the forward-looking statements and information regarding the Company. All forward-looking statements and information made in this news release are qualified by this cautionary statement.

The NYSE and TSX have not reviewed and do not accept responsibility for the adequacy or accuracy of the contents of this news release, which has been prepared by management of McEwen Mining Inc.

ABOUT MCEWEN MINING

McEwen Mining is a gold and silver producer with operations in Nevada, Canada, Mexico and Argentina. In addition, it owns approximately 52% of McEwen Copper which owns the large, advanced stage Los Azules copper project in Argentina. The Company’s goal is to improve the productivity and life of its assets with the objective of increasing its share price and providing a yield. Rob McEwen, Chairman and Chief Owner, has personal investment in the company of US$220 million. His annual salary is US$1.

| WEB SITE | SOCIAL MEDIA | |||||

| www.mcewenmining.com | McEwen Mining | Facebook: | facebook.com/mcewenmining | |||

| LinkedIn: | linkedin.com/company/mcewen-mining-inc- | |||||

| CONTACT INFORMATION | Twitter: | twitter.com/mcewenmining | ||||

| 150 King Street West | Instagram: | instagram.com/mcewenmining | ||||

| Suite 2800, PO Box 24 | ||||||

| Toronto, ON, Canada | McEwen Copper | Facebook: | facebook.com/mcewencopper | |||

| M5H 1J9 | LinkedIn: | linkedin.com/company/mcewencopper | ||||

| Twitter: | twitter.com/mcewencopper | |||||

| Relationship with Investors: | Instagram: | instagram.com/mcewencopper | ||||

| (866)-441-0690 - Toll free line | ||||||

| (647)-258-0395 | Rob McEwen | Facebook: | facebook.com/mcewenrob | |||

| Mihaela Iancu ext. 320 | LinkedIn: | linkedin.com/in/robert-mcewen-646ab24 | ||||

| info@mcewenmining.com | Twitter: | twitter.com/robmcewenmux | ||||

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/11da1d4f-c360-4f1a-bcbc-735be326d58d

![]()

Figure 1