BHP's $20B Canadian potash dilemma: To build or not?

BHP Group may be heading for another clash with investors as the world's biggest miner gets closer to a decision on whether to build, sell or mothball its $20 billion potash project.

The Jansen mine in Canada is aimed at giving the company exposure to rising global food demand and represents one of its few big growth prospects. BHP has already spent about $2.7 billion on the project, according to an October filing, and Chief Executive Officer Andrew Mackenzie last month spoke enthusiastically about the outlook for potash, a crop nutrient.

Yet investors and analysts are skeptical. The big-ticket project in the prairie province of Saskatchewan means getting into a new commodity dominated by a small handful of producers.

The world's largest miners are still on probation for spending decisions made during the last commodity boom and BHP has a poor record of capital allocation, including a disastrous $20 billion foray into shale. While BlackRock Inc. and others have flagged they'll back some projects, particularly in copper, there's less appetite for riskier investments.

"There's no case to be made where they throw good money after bad," said Brenton Saunders, a Sydney-based analyst at Pendal Group Ltd., which holds BHP shares. While the outlook for potash has improved, Jansen "is not a project that at this stage we think deserves serious consideration," he said. "It should be shelved or sold."

![]()

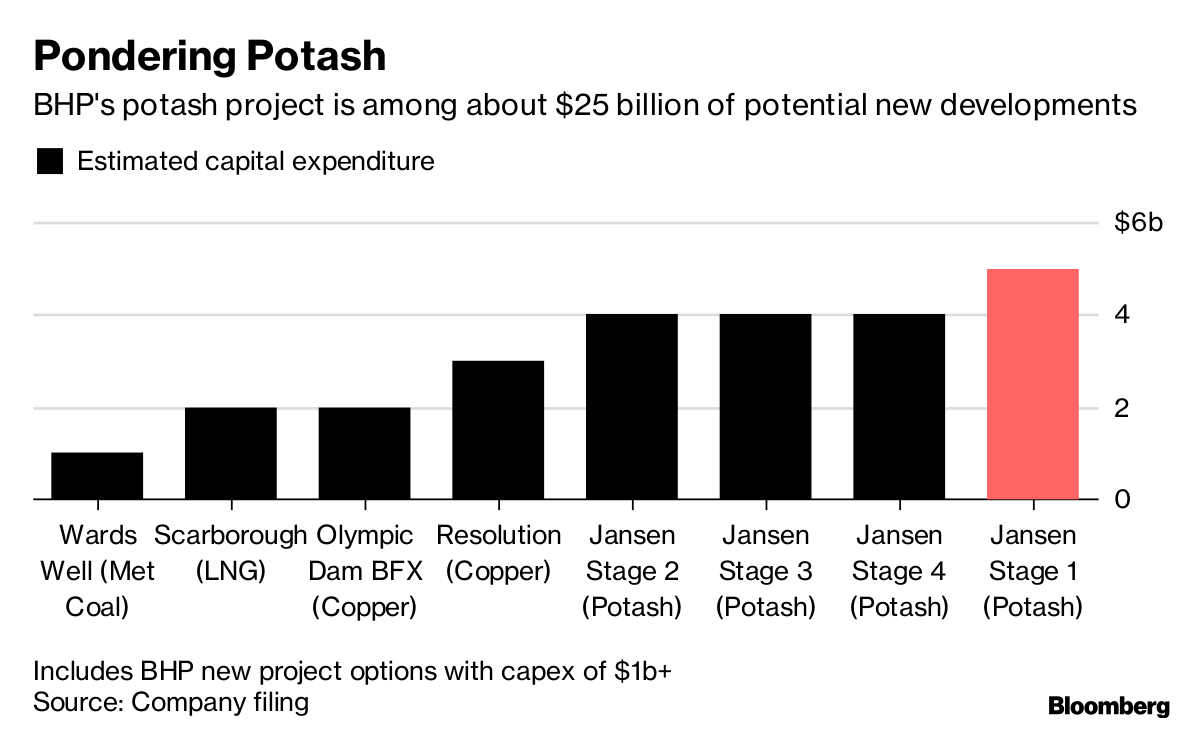

One way or the other, a decision is likely next year. BHP is nearing completion on two 1,000-meter (3,300-feet) deep shafts, which it has said will be a trigger to decide whether to press ahead with an initial $5 billion development. BHP has also been seeking a partner for Jansen since at least 2013.

The company last year delayed plans to seek board approval for the project, citing a weaker market outlook. It also followed investor criticism, including from activist Elliott Management Corp. New York-based Elliott declined to comment on its current position on Jansen.

BHP is continuing to investigate "all options to enhance returns and improve capital efficiency," and won't take the project to the board until it meets capital allocation hurdles, spokeswoman Bronwyn Wilkinson said in an emailed statement.

In a webcast last month, CEO Mackenzie was positive on the outlook for potash and BHP's assets. A rising global population and shrinking amount of land devoted to food production means the agricultural sector needs to lift efficiency, boosting the long-term outlook for fertilizers, he said.

BHP believes it has the world's best undeveloped potash assets and the business could eventually rival its iron ore unit in scale, Mackenzie said. Iron ore is BHP's top earner and accounted for almost 40 percent of underlying earnings in the 12 months to June 30.

Beyond a first stage development at Jansen, there's scope for three further expansions over a period of over more than 15 years at a cost of about $4 billion each, BHP said in a November presentation. Completing all four stages could take total investment in the project to almost $20 billion.

The company has better growth options to pursue in its portfolio, including expansions of existing coal to copper assets, said Andy Forster, a Sydney-based senior investment officer at Argo Investments Ltd., which holds BHP.

BHP advanced 1.9 percent in Sydney trading Thursday, as competitor Rio Tinto Group jumped 2.2 percent.

![]()

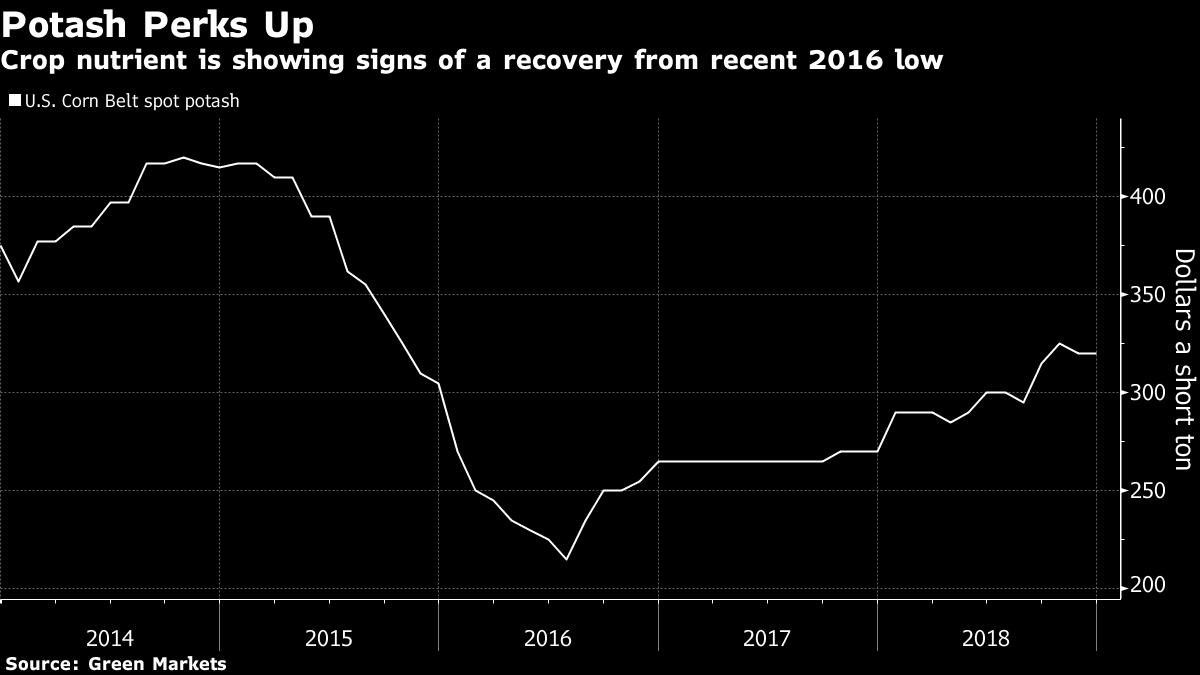

After spending the better part of a decade in a downward spiral, prices of potash have finally turned around. Stronger demand has come just as Canadian producers idle some mines, while new capacity has been added at a slower pace than expected.

BHP argues Jansen would enter production into a tighter market in the mid-2020s and that it could apply techniques from the oil industry to cut operating costs.

"If they can present a really compelling case, then we will judge it at the time," said Lou Capparelli, manager, equities at Melbourne-based UniSuper Management Pty, which has about A$70 billion ($50 billion) under management, and holds BHP shares. "There's inherent risk with those projects, but that's the nature of what a resources company does."

Still, new potash projects are tough to justify at current prices, according to Sanford C. Bernstein & Co.

"Demand growth is not stellar, supply is abundant, there's plenty of idled capacity that seems to be waiting in the wings," said Paul Gait, a London-based analyst at Bernstein. For BHP "it's very hard to see a case where people see this as the best use of capital versus just giving it back to shareholders," he said.

(By David Stringer, Thomas Biesheuvel, and Jen Skerritt)