Global Gold Output to Hit New Record High in 2019

Gold production increased for the 10th consecutive year in 2018 to 107.3 million ounces (Moz), and is expected to reach a new record high of 109.6 Moz in 2019, according to the latest metals and mining research by S&P Global Market Intelligence. Although the year-over-year increase of just under 1% was the smallest in the last decade, output has risen by 40% since 2008.

Christopher Galbraith, Research Analyst at S&P Global Market Intelligence, www.spglobal.com, said, "We believe the forecast growth of 2.3 Moz in 2019 will be the strongest growth in the past three years, debunking commentary calling for peak gold. More than half of the increase is projected to come from new mines that are expected to come on stream this year or have recently commissioned."

"Looking at the current project pipeline, we expect output to stay steady until 2022 due to advancements at developing projects. From there on, gold production is expected to fall by over 3 Moz in 2023 and up to 5 Moz in 2024."

More than 15% of gold production by 2024 will be coming from mines that are not yet producing

More than half of the 2.3 Moz increase in 2019 is projected to come from new mines that are expected to come on stream in the year or have recently commissioned. Examples of those include Gruyere JV in Western Australia (50% Gold Fields Ltd., 50% Gold Road Resources Ltd.), which is expected early in the June quarter; Meliadine in Nunavut (Agnico Eagle Mines Ltd.); Sigma-Lamaque in Quebec (Eldorado Gold Corp.), which has already commissioned; and the restarted operations at Obuasi in Ghana (AngloGold Ashanti Ltd.) and Aurizona in Brazil (Equinox Gold Corp.), both of which have been idle since 2015.

The ongoing ramp-up at PJSC Polyus's Natalka and Nord Gold SE's commissioning at Gross are significant contributors to a continued increase in Russia's production in 2019. Russia's production is expected to essentially equal Australia's in 2020 and then surpass Australia. Meanwhile in Canada, the startup of Meliadine and continued ramp-up of Rainy River, Eleonore and Hope Bay, among others, drive some of the fastest national growth that is expected to last for several years. Canada is projected to surpass the U.S. in national gold production in 2019 to be the fourth-largest gold producing country.

New production coming on stream over the next five years is expected to produce as much as 4.3 Moz/y by 2024. Another 11.7 Moz/y is expected from projects currently undergoing feasibility studies or evaluating restarts. Falling production from depleted operations over the next several years will start outpacing that growth by as early as 2021. Current forecasts project 2020 production to increase as much as 0.4 Moz year over year. Then production is expected to fluctuate, with a roughly 0.7-Moz drop in 2021 followed by an increase again in 2022 due to advancements at developing projects. From there on, gold production is expected to fall by over 3 Moz in 2023 and up to 5 Moz in 2024. That latter drop will leave gold production 7%, or 7.2 Moz, lower than 2019 levels. If only half of the probable new production enters the market, gold production will be 13 Moz, or 12%, lower than 2019 levels.

Canada is the only major gold-producing country to continue significant increases in 5 years

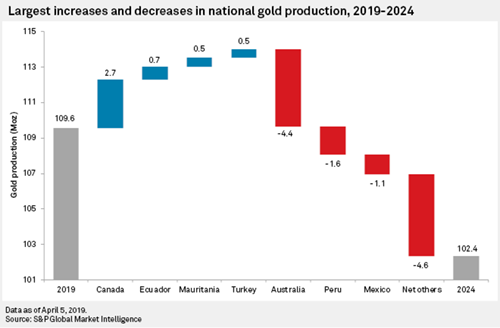

Although global production is expected to start decreasing, not all jurisdictions will have shrinking production. Of the 99 countries with gold production in 2018 or that will have production in 2024, 49 are expected to produce less, 27 to produce more and 23 are expected to maintain production.

Australia's production is expected to fall the most. The current second-largest gold producing nation behind China is expected to fall to fourth place globally in 2024. The underlying reason for Australia's fall is the depletion of several long-lived assets such as St Ives, Paddington, Telfer, Edna May, Southern Cross, Agnew/Lawlers and more. The expected commissioning of Mt Todd and reactivation of Union Reefs Operations Centre will partly mitigate the loss from those aforementioned closures.

Although Indonesia's gold production appears to fall substantially by 2024, 2018 production was anomalously high primarily due to the previously mentioned increase at Grasberg. Grasberg's gold production in 2024 is expected to be comparable to most other years; therefore, Indonesia's production at large is expected to be only slightly lower than previous years.

Peru's production, meanwhile, is clearly trending downward, with Orcopampa, La Zanja and Tambomayo all facing depletion before 2024. With closure only a few years further out, Lagunas Norte and Yanacocha will also be producing far less gold in 2024 than they have historically.

Among the countries expected to increase production, Canada is expected to have four times the production increase of second-closest Ecuador. Canada's still growing gold sector is showing no signs of abating five years in the future. Very few of the country's gold mines are facing depletion, and new ones continue to commission such as Eleanore in 2015, Brucejack in 2017, Rainy River in 2017 and Hope Bay in 2017; still more are expected, including the aforementioned Lamaque and Meliadine, plus Dublin Gulch in 2019 and Coffee in 2021.

It is of note, however, that Canada's production five years out includes several projects that have not started construction, including Casino with production expected in 2023, Brookbank in 2021, Blackwater in 2022, Horne 5 in 2022 and Back River in 2023. Those five projects account for 1.9 Moz of Canada's projected 2024 production, more than half the 2018-24 increase. Only Casino has had a production decision made. Therefore, delays on the other projects could diminish the country's production increases considerably.

Ecuador's projected increases come from a handful of new projects. The largest of them is Lundin Gold Inc.'s Fruta del Norte project, expected in 2020, while INV Metals Inc.'s Loma Larga project could be producing by 2021-22. Turkey and Mauritania's expected increasing production comes from projects owned by or involving major producer partners. In Turkey new production is expected from Oksut in 2020, Agi Dagi, Kirazli and Yenipazar in 2021; Hod Maden in 2022; and Gediktepe in 2023. Mauritania's increase comes exclusively at the projected commissioning of the Phase 2 expansion at Tasiast, 2020-21.

Gold grades fairly steady as throughput falls

As the gold price declined through 2016-17, it was increasingly important for producers to maintain an optimal grade profile. The environment of a falling gold price placed increased pressure on costs, and minimizing the processing of low-grade material was at least one means of obtaining the most return. From 2014 through 2018, throughput at primary gold mines increased by 1.2%. Meanwhile, the weighted-average gold grade increased by 4.5%, and as a result, gold production from primary gold mines increased by 6% during the period.Save for a subtle drop in 2018, the increase in grade is projected to continue through 2020 and maintain higher-than-current levels in the subsequent years. In 2021 we expect ore throughput to remain steady but grade to fall by 2% year over year. These two factors are expected to account for around 1.6 Moz in reduced production. By 2024 around 241 million tonnes less ore is expected to be fed at gold mills compared to 2019, while the gold grade will be almost 2% higher. Owing to that drop in throughput, the related drop in production from primary gold mines will be almost 9 Moz.

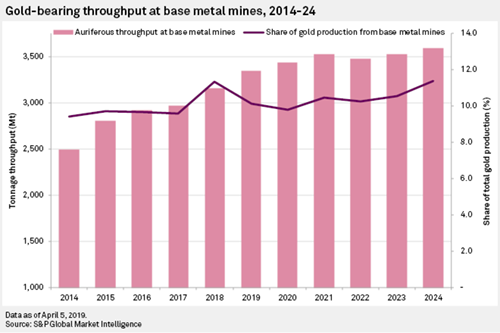

As gold production starts to fall, growing share of production will come from base metal mines.

In 2018, more than 11% of global gold production came from polymetallic base metal mines - a considerable increase of 2 Moz over the 9.6% in 2017 - with more than 1 Moz of that coming from Grasberg. That increase will, however, be short-lived, as Grasberg's gold production is expected to fall by 0.9 Moz in 2019 as gold grades decrease. Increased gold content from Kazzinc Consolidated, Batu Hijau, Oyu Tolgoi and Escondida contributed another 0.7 Moz to 2018 production, but all of those operations are expected to see gold production fall in 2019.

As those polymetallic mines experience only a brief interval of gold-rich ore, gold production from those mines will fall in 2019 and 2020. Past 2020 though, polymetallic mines' gold production is expected to increase gradually. With falling production from primary gold mines after 2020 and minor increases from polymetallic mines, a growing share of the world's gold production will come from sources where gold is a byproduct. Less than 10% of the world's production is expected to come from secondary sources in 2020, but this amount is expected to grow to more than 11% by 2024.