February 23, 2026

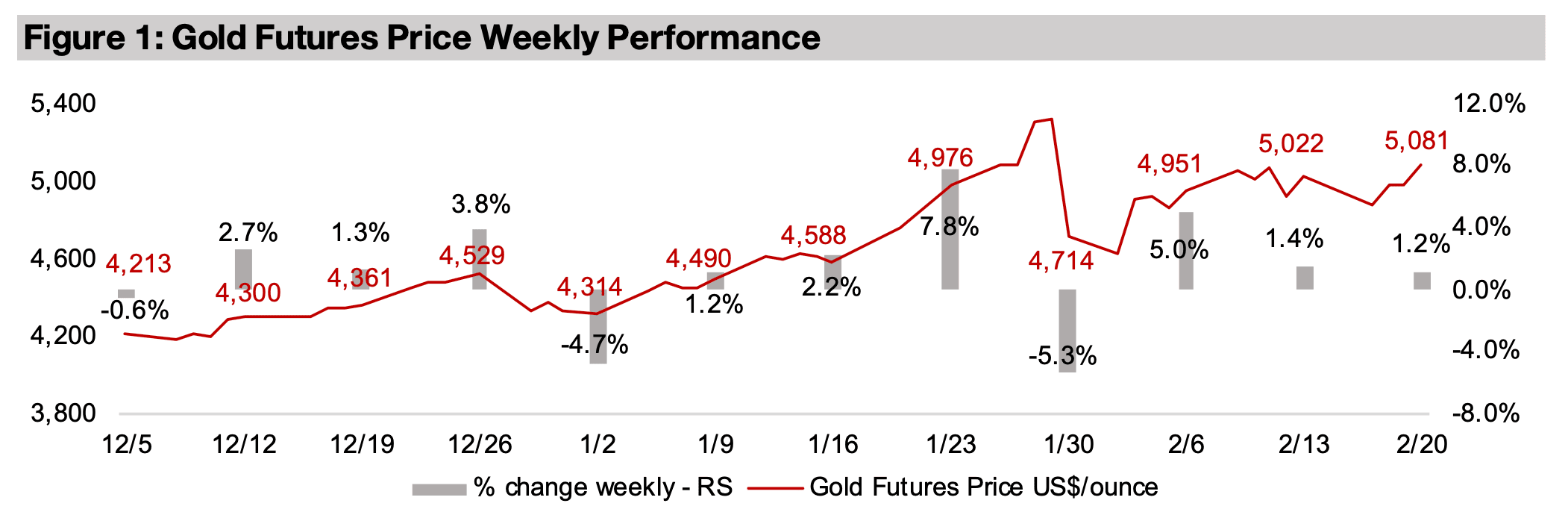

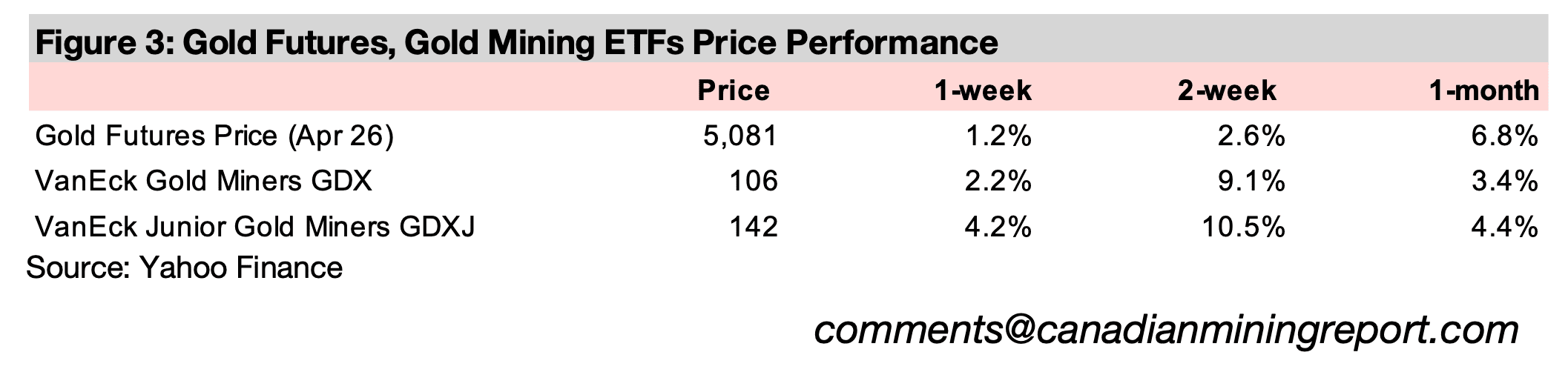

Gold rose 1.2% to US$5,081/oz, back above the key US$5,000/oz benchmark for a third time, after seeing resistance and dropping below this level twice over the past month, with the main economic driver this week the resurgence of US tariff concerns.

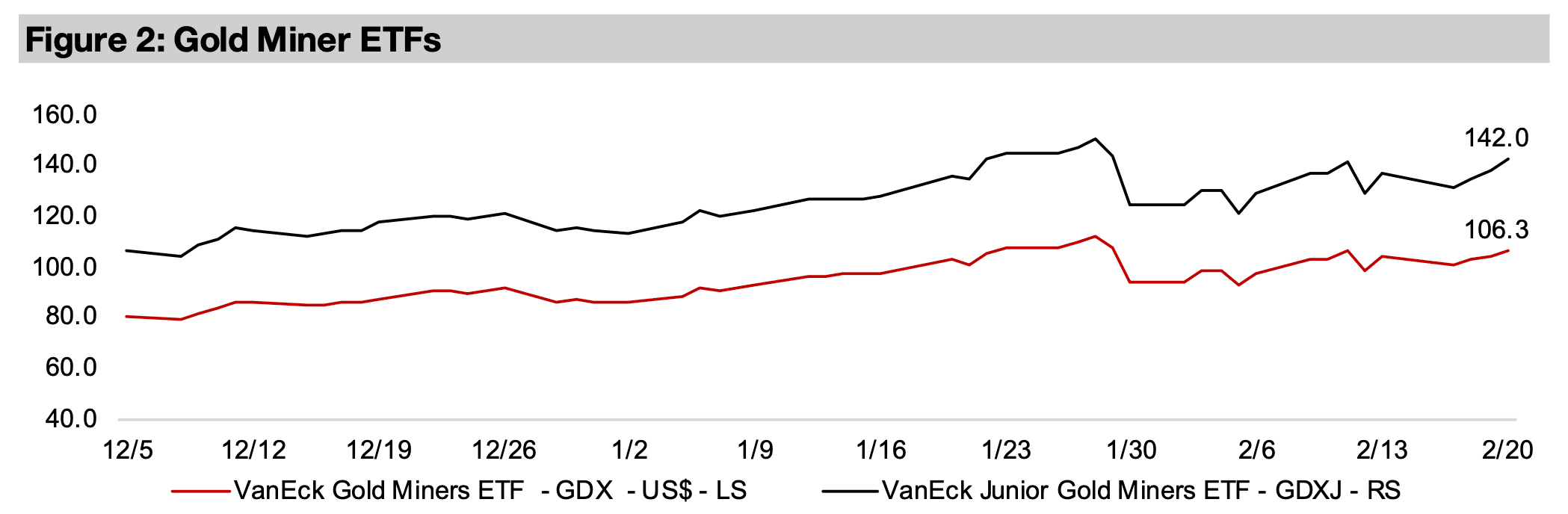

The gold stocks rose, with the majors beat by the juniors, as the GDX increased 2.2% and GDXJ gained 4.2%, surpassing the increase in equity markets with the S&P 500 up 1.1%, the Nasdaq rising 0.9% and Russell 2000 gaining 1.7%.

The gold price rose 1.2% to US$5,081/oz, getting above the key US$5,000/oz

benchmark for third time, after breaking through twice over the past month only to

drop back below this level. The main economic driver was new US tariff risks, as the

Supreme Court ruled against many of the tariffs imposed earlier this year. The equity

markets responded well to this, with the S&P 500 increasing 1.1%, the Nasdaq rising

0.9% and Russell 2000 gaining 1.7%. However, with gold also rising, it implies that

the market is continuing to hedge risk on moves, and this issue is unlikely to be fully

resolved, as the President responded to the decision with global tariffs of 15% to

replace those that that the Supreme Court struck down.

While the gold stocks rose, they were mixed, with the majors lagging as the GDX rose

just 2.2%, partly from a decline in Newmont on its Q4/25 results, outpaced by the

gold juniors, with the GDXJ rising 4.2%. There was a return of extreme volatility to

the other precious metals, after a brief cooling period over the past two weeks, with

silver surging 13%, platinum jumping 6.6%, and palladium up 3.2%. The gains

appeared to have been mainly driven the court ruling on the US tariffs, which also

saw a 2.1% and 1.8% gain for the week, respectively, in copper and aluminum.

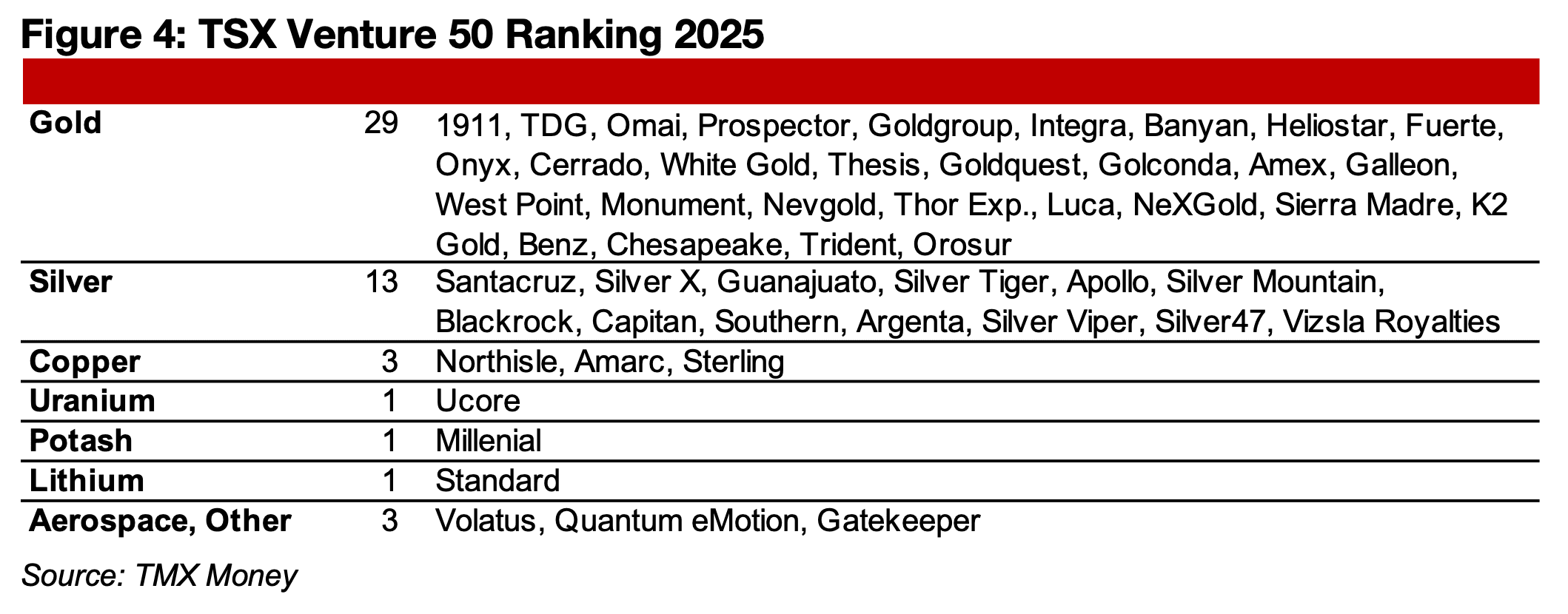

The TSX Venture 50 for 2025 was announced by TMX Money, ranking the top stocks on an equal weighting of share price gains, the increase in market cap and trading volume. Gold stocks dominated the list, as would be expected given the surge in the gold price, comprising 29 out of 51 stocks (with two tied, adding one to the Top 50). Silver stocks had the second highest number of stocks in the ranking, driven by the late 2025 rally in the metal price. While the copper price was reasonably strong in absolute terms last year, it significantly lagged gold and silver, leaving the sector with only three companies in the ranking. The uranium, potash and lithium sectors had only one company each on the list, and there were just three non-mining companies.

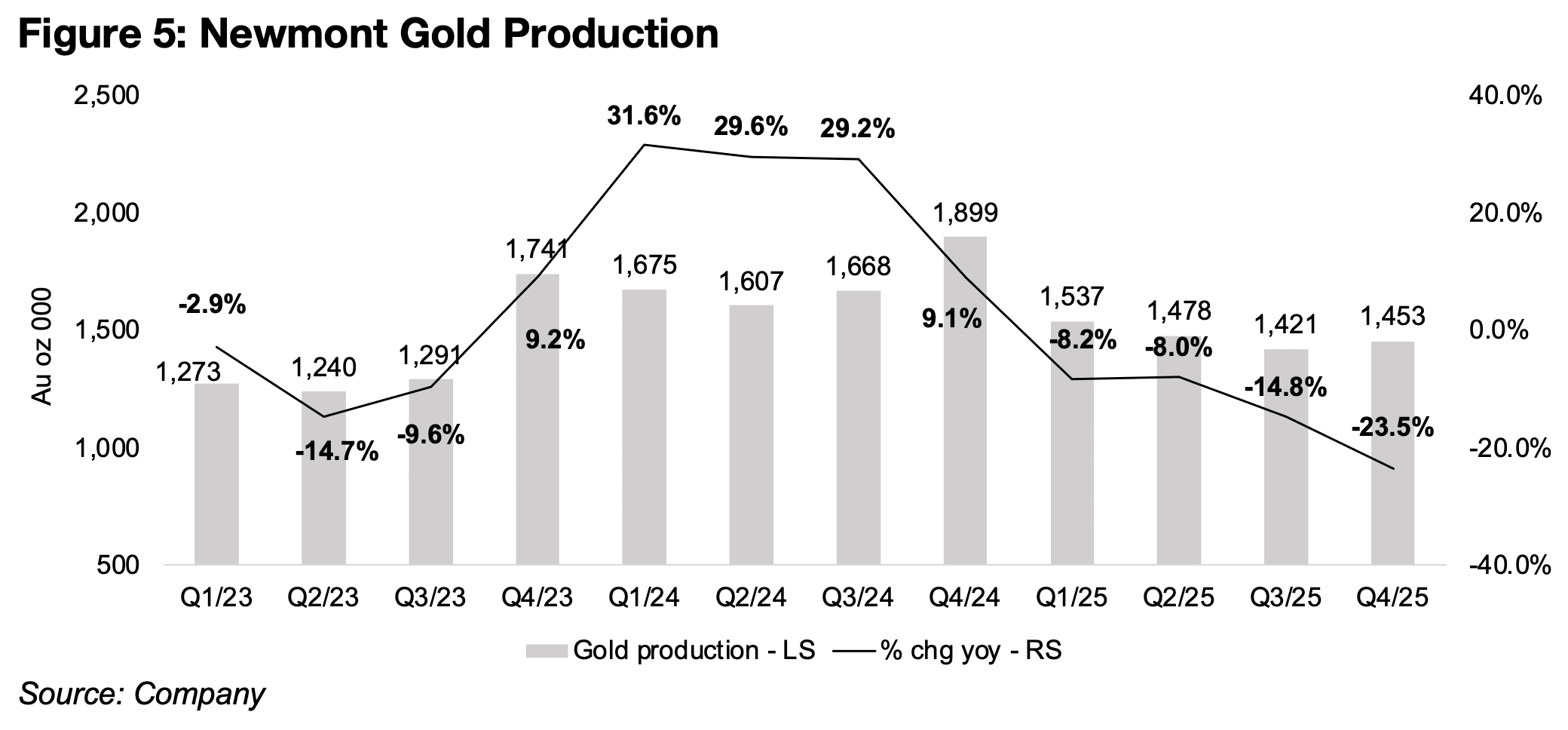

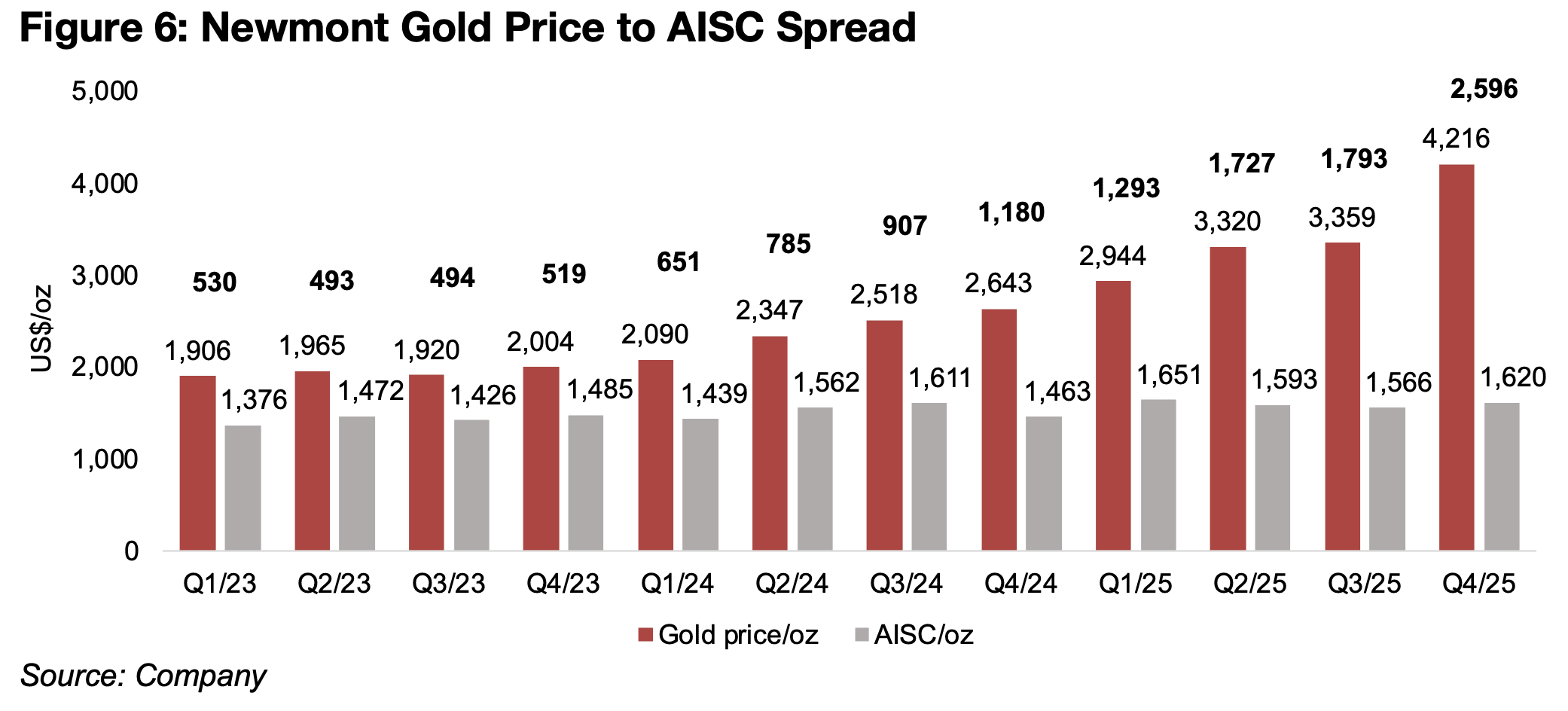

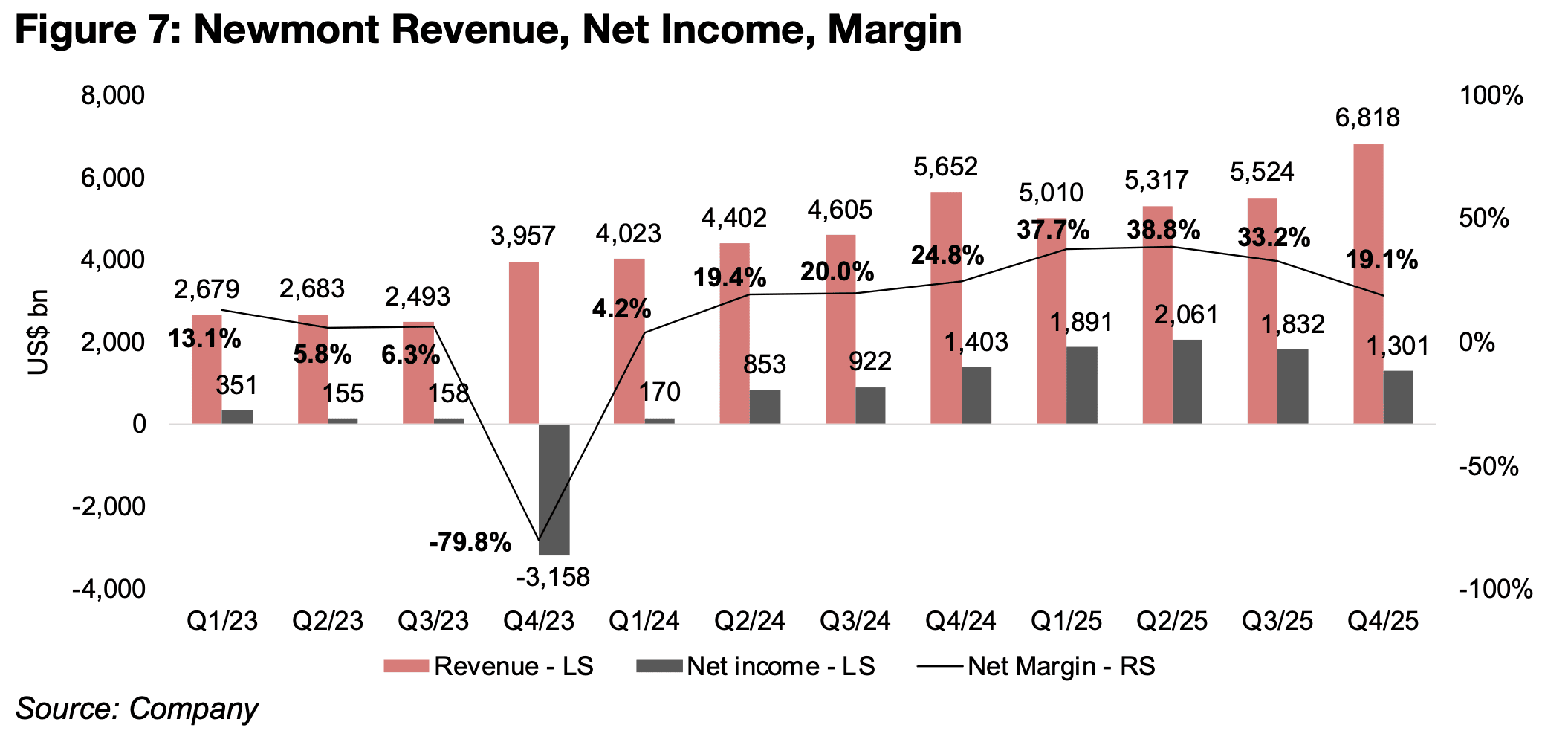

The last of the three Big Gold companies to report Q4/25, Newmont, released results this week. Production growth continued to trend down to -23.5% yoy in Q4/25, from a peak of 31.6% in Q1/24, with output down to 1.45 mn oz Au, off highs of 1.89 mn oz in Q4/24 (Figure 5). There was a decline in output yoy in the quarter especially at Ahafo South, down 92k oz Au, or -43% yoy, but also from several other major mines, including Lihir, Cadia and Boddington, offset somewhat by large increases from Yanacocha and Nevada Gold Mines. However, this decline in production was far offset by the surge in the realized gold price to US$4,216/oz for Q4/25, up 59.5% yoy from US$2,643/oz in Q4/24 (Figure 6). All-in-sustaining costs per oz remained relatively low at US$1,620/oz Au, up 10.7% yoy, but down from the recent peak of US$1,651/oz in Q1/25. This led to an expansion in the realized gold price to AISC spread to US$2,596/oz, up US$803/oz from Q3/25 and US$1,416/oz in Q4/25.

While the rising spread drove strong gains at the operating level yoy, net income

declined qoq to US$1.30bn from US$1.83bn in Q3/25, the second consecutive quarter

of decline from a peak of US$2.06bn in Q2/25 (Figure 7). This contrasts substantially

with the other two Big Gold companies, with Barrick and Agnico Eagle seeing major

net income gains qoq for the past two quarters. Newmont’s net income has weakened

because of significant non-operating items, with Barrick and Agnico Eagle not having

faced major exceptional expenses since 2022 and 2023.

In Q4/25 Newmont reported a high income and mining tax expense of US$2.07bn,

jumping 163% qoq, partly from the higher gold price, but also from taxes on

undistributed foreign earnings of US$384mn from Papua New Guinea and US$165mn

from Ghana. There was also a US$779mn impairment charged mainly on a decision

to indefinitely postpone the Yanacocha project, and a smaller US$8mn loss in

divestments in Q4/25 versus a US$39m gain in the previous quarter. In Q2/25

Newmont’s net income was boosted by a US$699mn gain on assets for sale, but this

declined to a US$99mn gain in Q3/25, which drove a considerable decline in earnings.

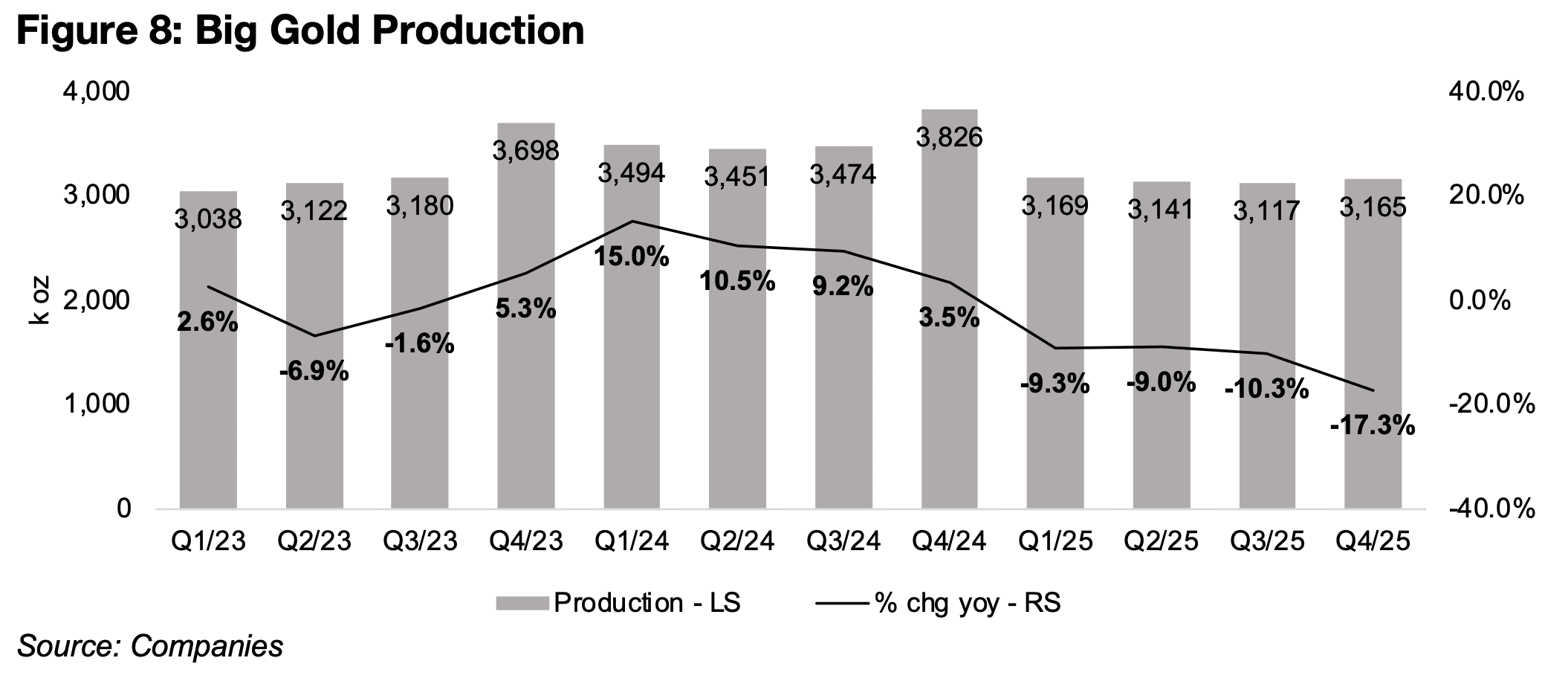

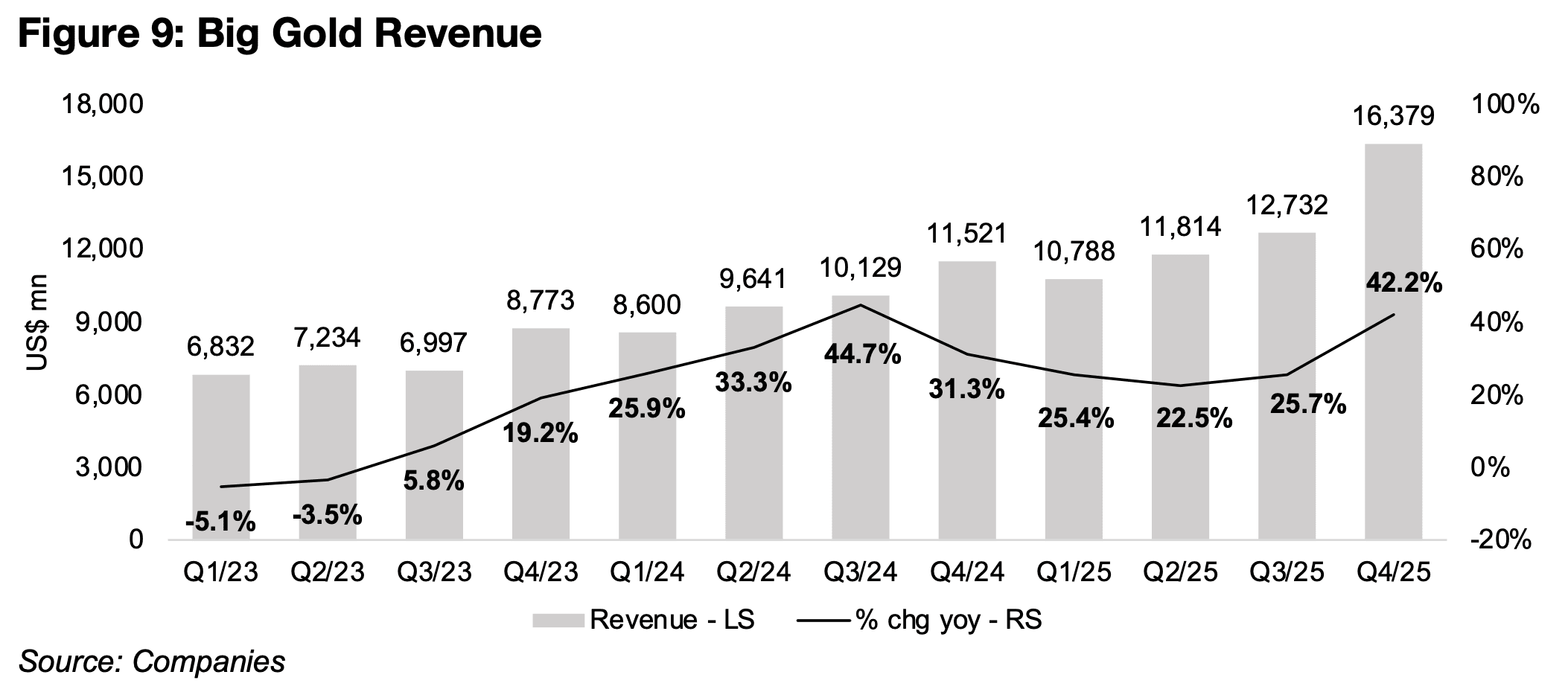

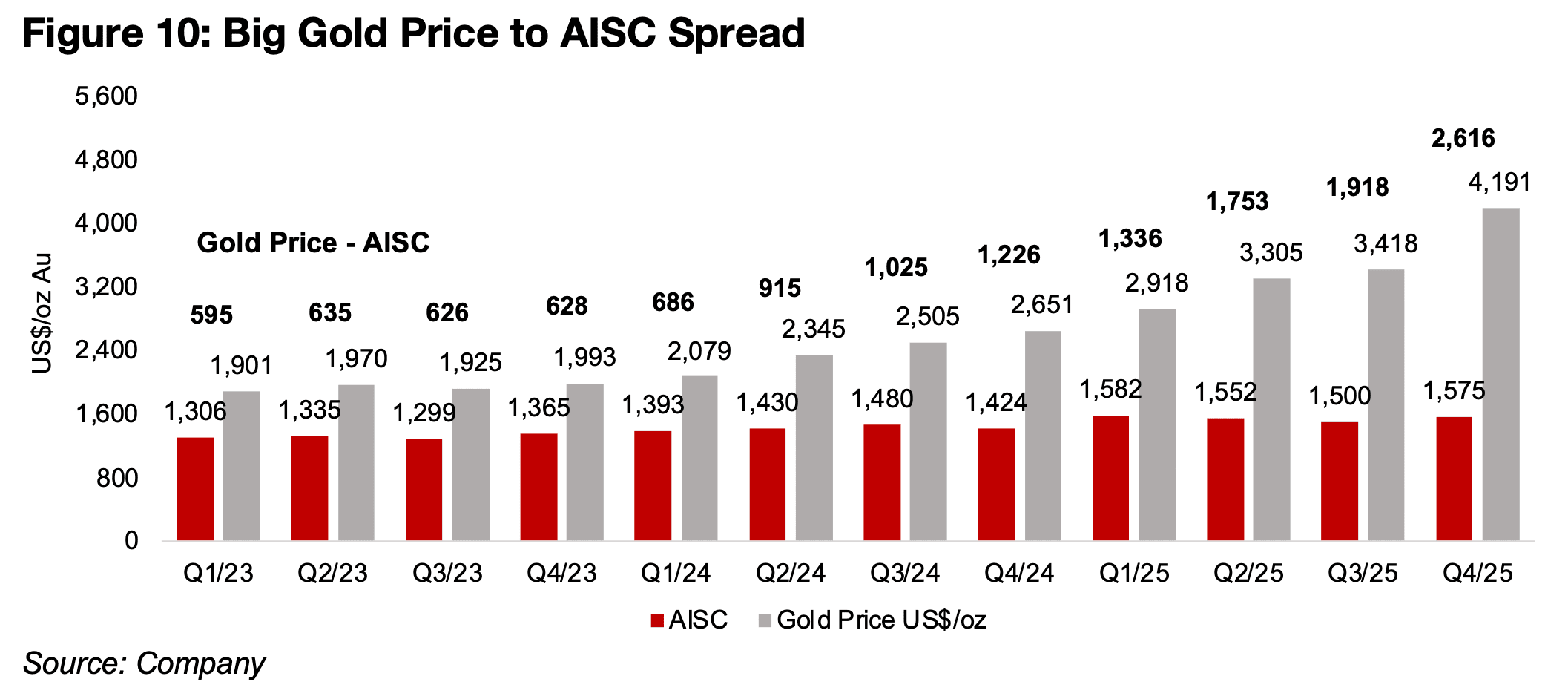

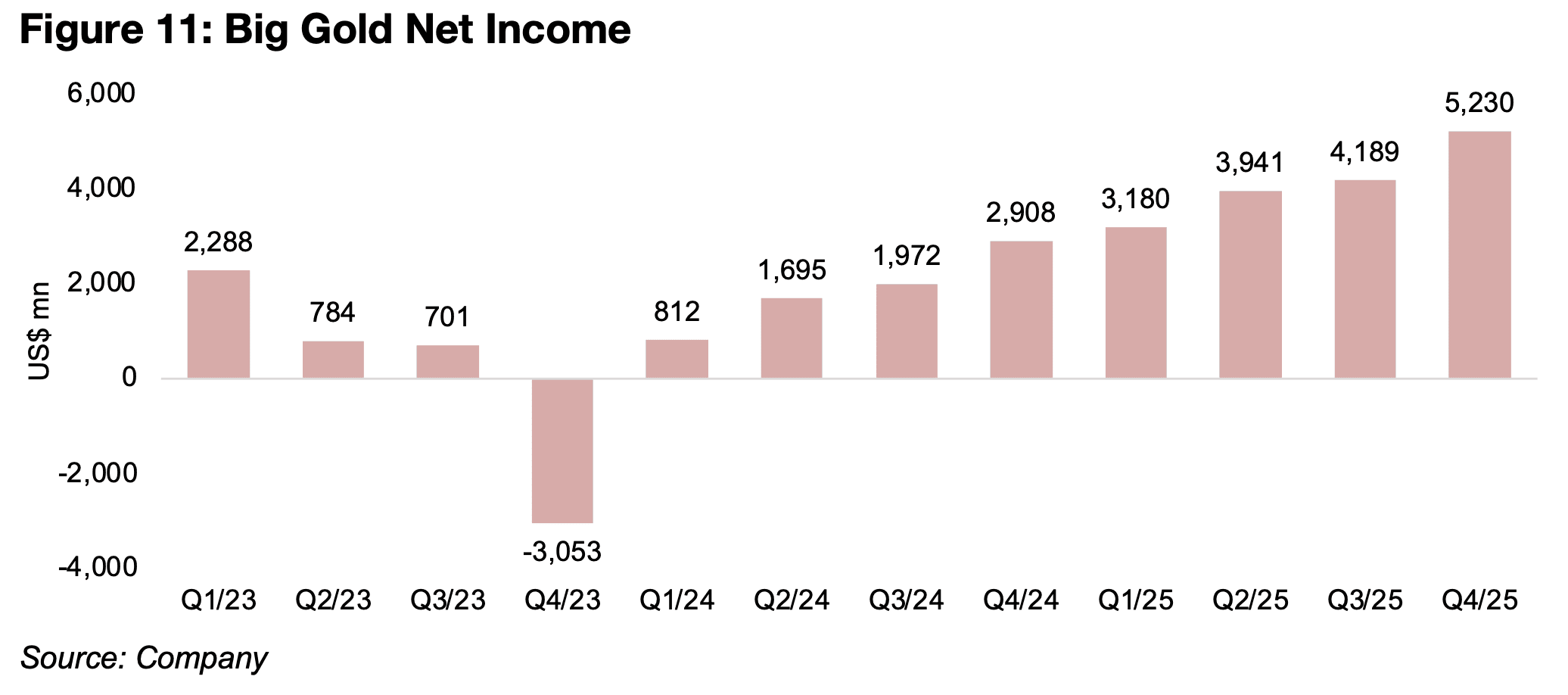

Overall Big Gold production has weakened significantly in 2025, down around -10%, with Newmont and Barrick especially facing considerable declines and Agnico Eagle’s (Figure 8). Revenue has continued to grow, with the production drop offset by the rising gold price, with the rate picking up over H2/25 after declining in H1/25, with the Q4/25 rise of 42.7% back near the recent peak of 44.7% in Q3/24 (Figure 9) Costs have remained reasonably flat with the average AISC of US$1,575/oz up only 10.6% yoy from US$1,242/oz, and trending down through mid-2025 from Q1/25 highs before a moderate rise qoq in Q4/25 (Figure 10). The net income for Big Gold has increased significantly in every quarter since the start of 2024 (Figure 11).

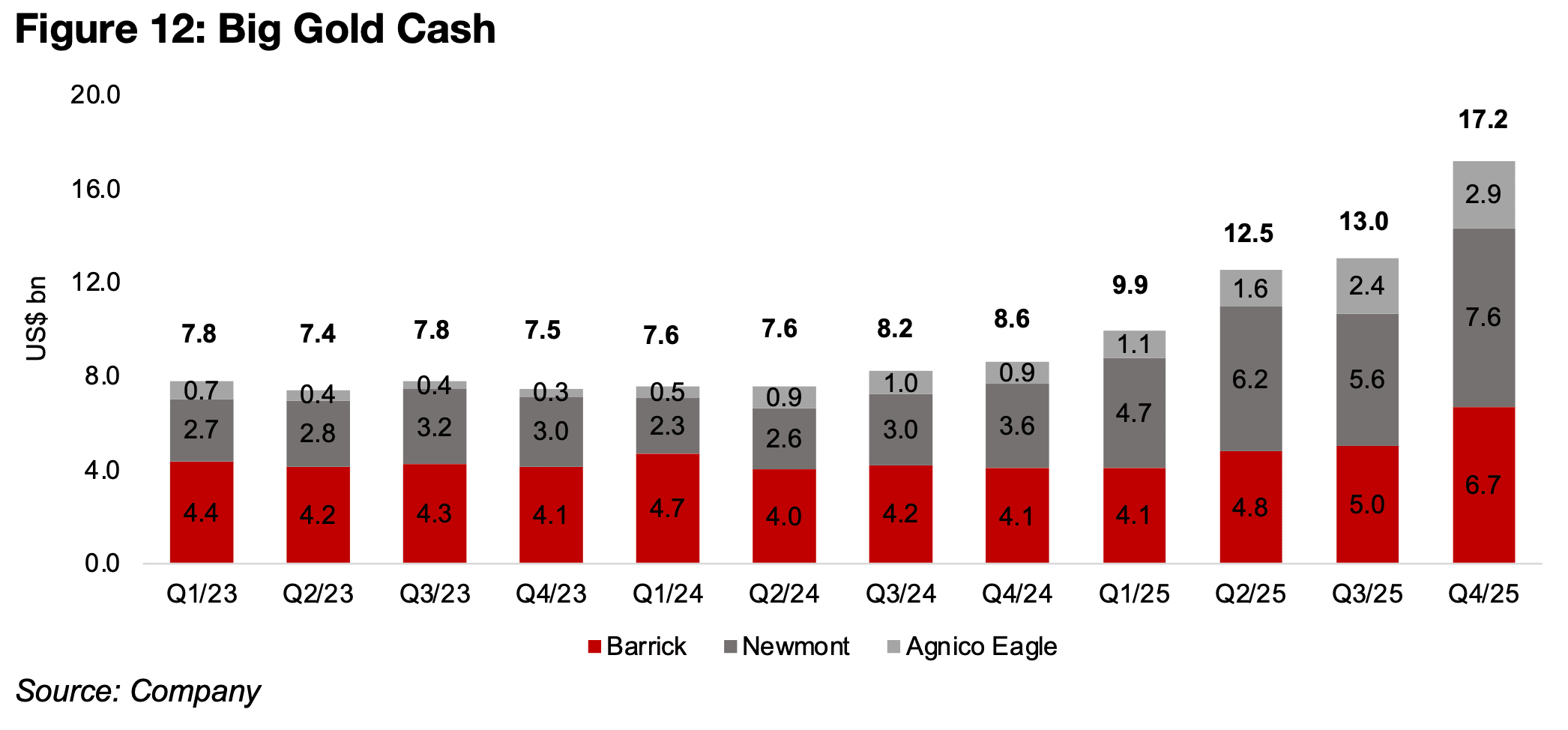

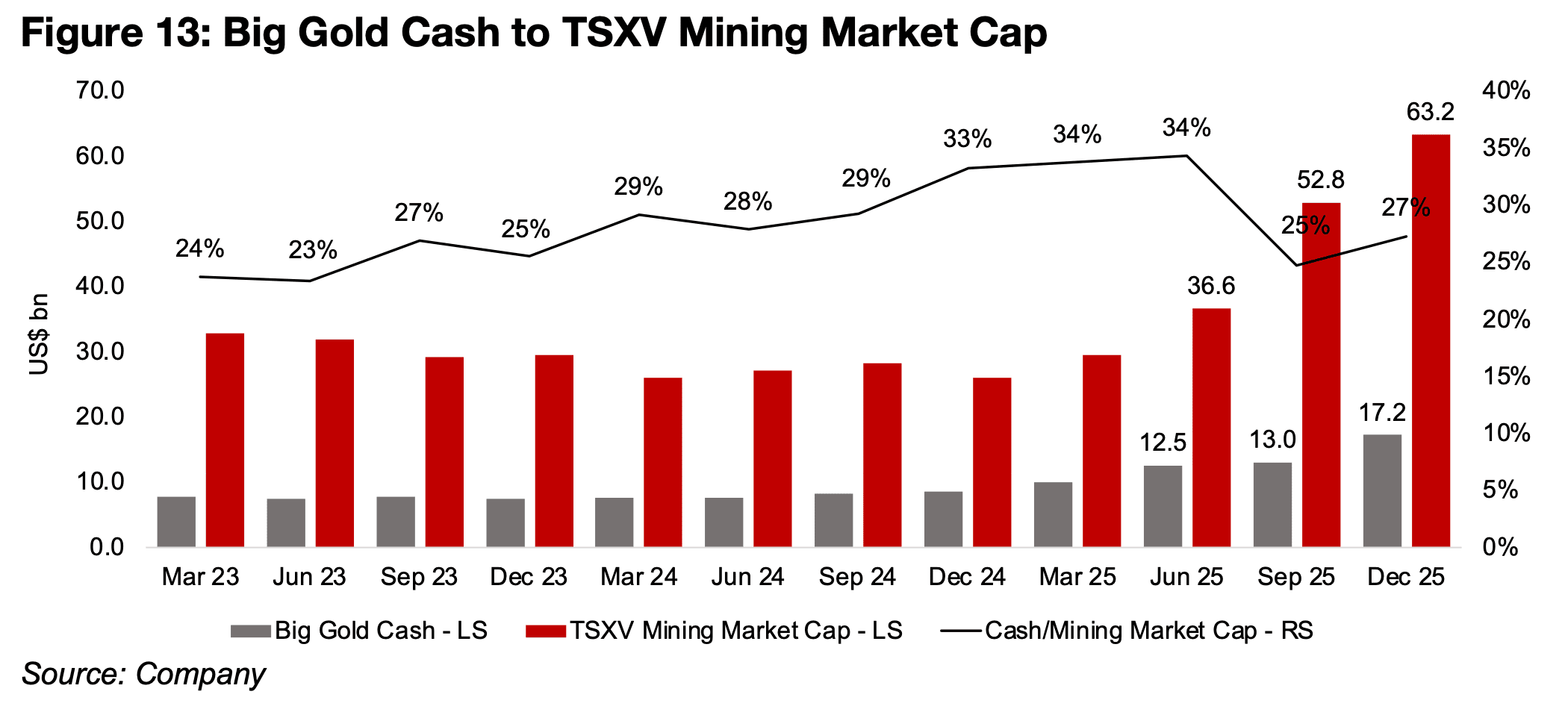

Newmont’s cash jumped by US$2.0bn in just Q4/25 and has now reached US$7.6bn, with the total for Big Gold having reached US$17.2bn, with US$6.7bn for Barrick, and even Agnico Eagle, which through 2023 and 2024 had a relatively low cash balance, now at US$3.0bn. This implies that we could be seeing higher dividends or buybacks and M&A from these companies, especially since the gold price could spend the rest of this year averaging at least at Q4/25 levels, if not higher, and Big Gold will continue to accumulate an even higher cash pile. They are unlikely to be able to completely use up this cash by dividends or buybacks over a reasonable period and return on equity could suffer if a large proportion of the asset base is making a low payout in short to medium-term financial instruments.

This will very likely see the companies turn to M&A, especially given the recent decline in production and the perpetual need for the major producers to replenish depleting reserves. This could benefit some of the stronger juniors on the TSXV, with just Newmont, Barrick and Agnico Eagle alone able to purchase 27% of the entire TSXV Mining market cap with their current combined cash (Figure 13). The are at least another ten mid-tier juniors which also have reasonably large market caps and will have been building up significant cash over the past few quarters, likely driving them to also seek out significant acquisitions.

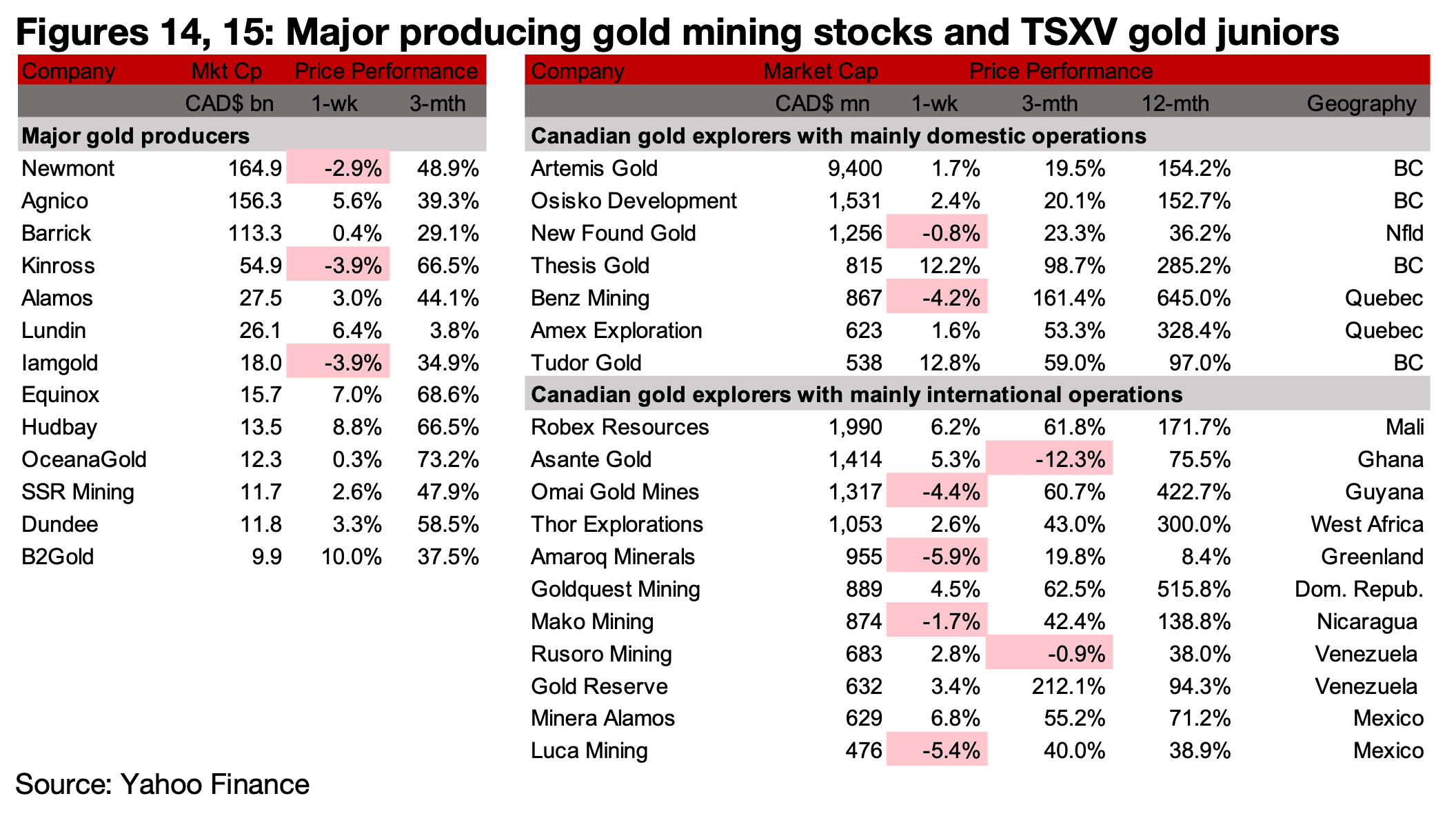

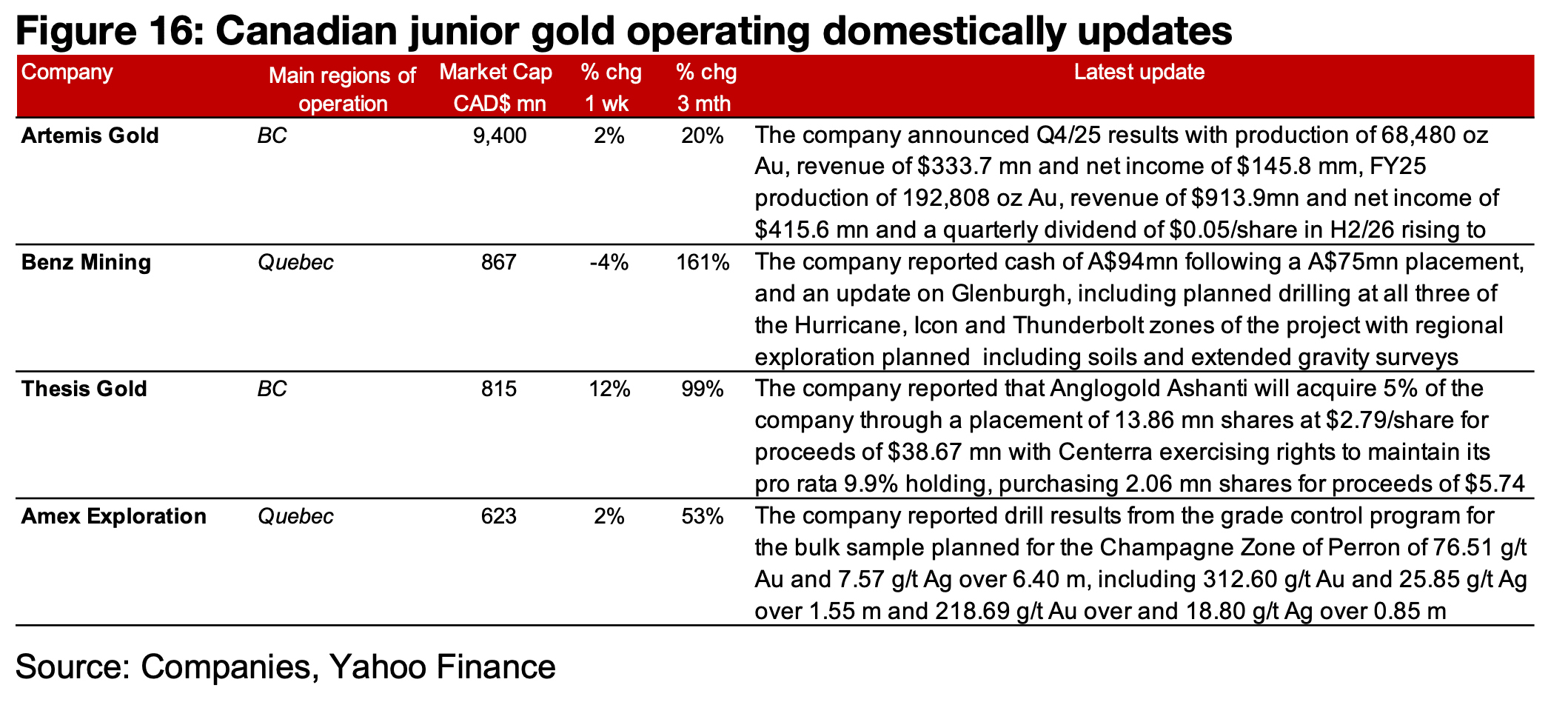

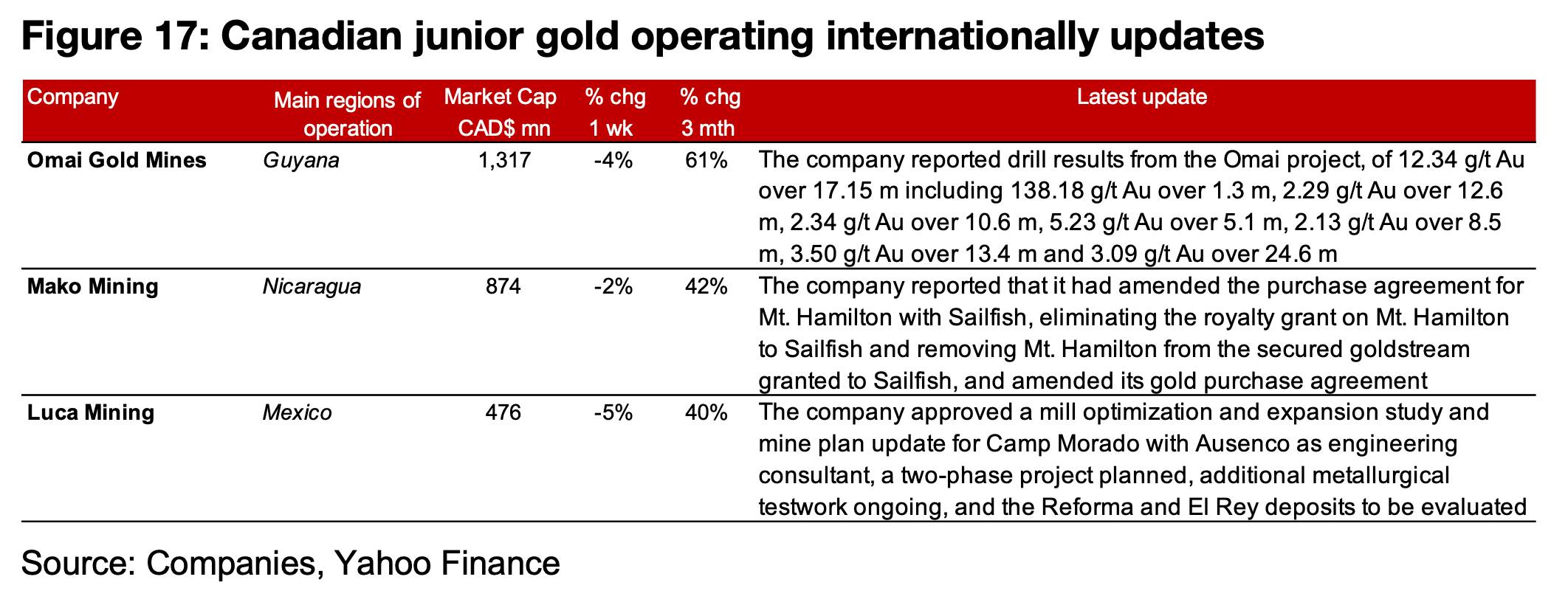

Some of the major producers declined, including Newmont, after Q4/25 results, while TSXV gold was mixed (Figures 14, 15). For the TSXV gold companies operating mainly domestically, Artemis Gold reported Q4/25 results and its dividend policy, Benz provided an operational update on Glenburgh, Thesis announced the acquisition of a 5% stake by Anglogold Ashanti and placement to Centerra to maintain its stake and Amex released drill results from Champagne at Perron (Figure 16). For the TSXV gold companies operating mainly internationally, Omai reported drill results from the Omai project, Mako amended its purchase and gold purchase agreements for Mt. Hamilton with Sailfish, and Luca approved a mill optimization and expansion study and mine plan update for Camp Morado (Figure 17).

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.

Author

Ben McGregor authors the Weekly Roundup at CanadianMiningReport.com, providing sharp analysis of the metals and mining sector. With a talent for spotting trends, Ben distills complex market shifts into clear, engaging insights on TSXV junior miners. His weekly updates cover gold, copper, uranium, and more, blending data-driven perspectives with a knack for identifying opportunities. A vital resource for investors, Ben’s work navigates the dynamic junior mining landscape with precision.