March 09, 2026

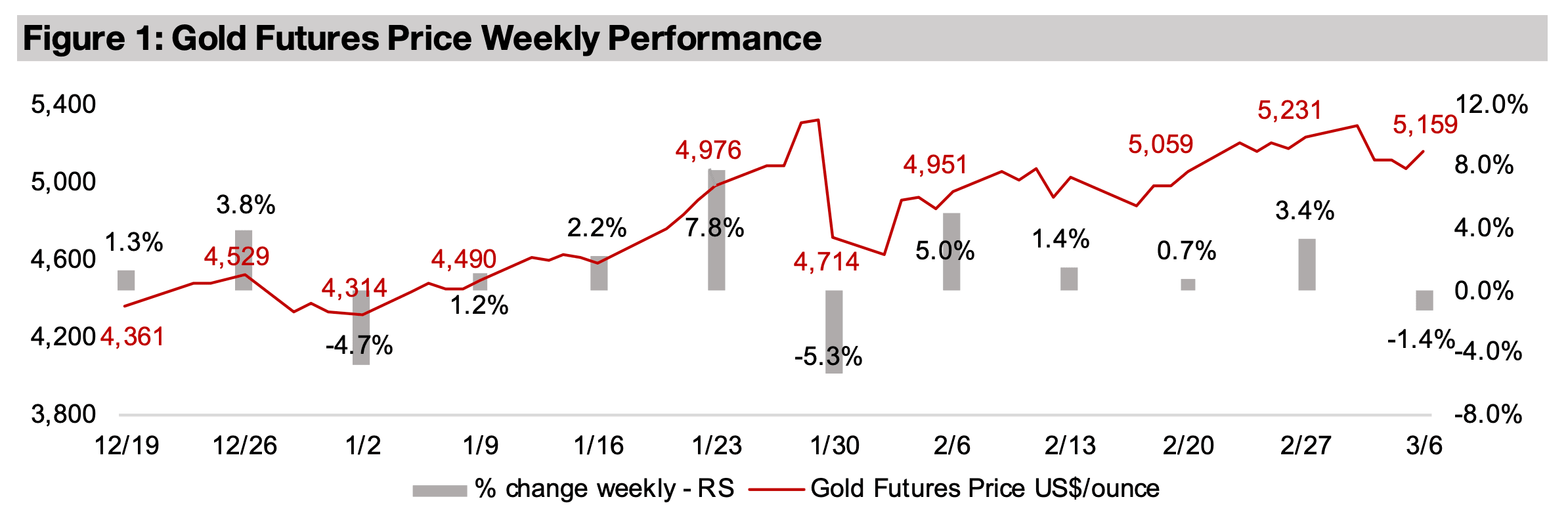

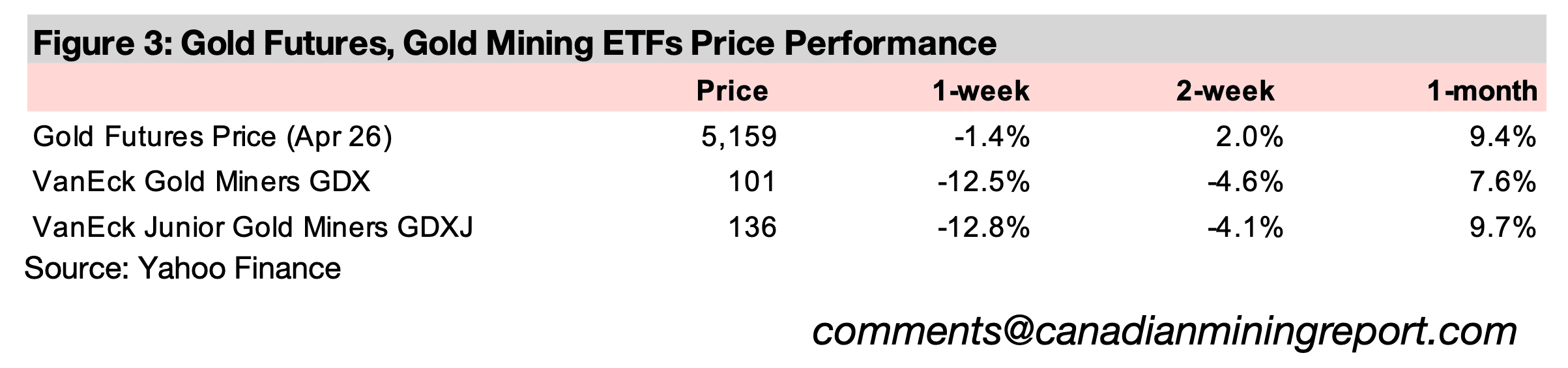

Gold declined -1.4% to US$5,159/oz, partly from a rise in the US$, which seems to have resumed its role as a safe haven following a continued escalation of the Middle East conflict, that saw oil surge 35.6%, strongly outperforming other major assets.

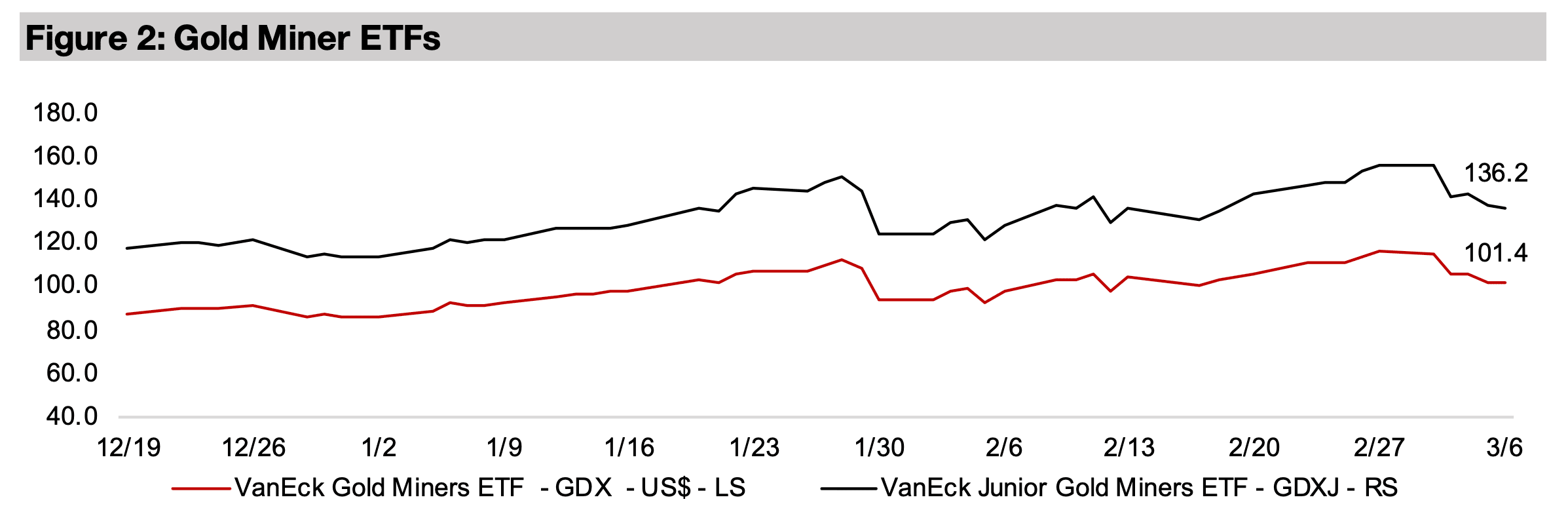

The gold stocks plunged, with the GDX down -12.5% and GDXJ off -12.8%, likely partly on rising cost concerns on the jump in oil, underperforming the equity markets, with the S&P down -1.2%, Nasdaq up 0.3% and Russell 2000 losing -3.2%.

The gold price dropped -1.4% to US$5,159/oz, partly from a 1.4% rise in the US$ on

the continued escalation of the conflict in the Middle East. After an extended period

of relatively weak market support left the US$ down -4.7% over the past year, the

surge in geopolitical risk has apparently been enough for the currency to again be

viewed as a safe haven. Oil saw the biggest gain by far of the major assets, with the

WTI price surging 35.6% on supply disruptions from the conflict. The Straits of

Hormuz, a key shipping route, are already closed to many Western countries, and

there have been direct attacks on tankers and refineries in several countries in the

Middle East which have limited oil transport and production.

The rising oil price was likely a key driver of the drop in many metals prices, given

that this could imply a major rise in mining costs, with fossil fuels a very large

proportion of total expenses for the sector. The other precious metals slumped, with

silver and palladium both down -11.9% and platinum off -12.9% and copper was

down -5.2%. Gold’s significant outperformance of these metals, with only a slight

decline, may partly be from the market expecting a decline in global economic growth,

and a potential increase in the money supply in response, which is a key driver for

the metal. The other precious metals also had a much stronger rise than gold over

the past six months, so their declines could partly be from an unwinding of some

speculative excesses, with the copper price possibly facing a similar situation.

However, some major metals actually rose significantly, including aluminum, jumping

8.9%, as a high proportion of its processing capacity is in the Middle East, while iron

ore gained 2.9%. Gold stocks slumped, as expectations of rising costs were likely a

major driver, with the GDX down -12.5% and the GDXJ losing -12.8%. The gold

sector notably had quite muted cost gains overall for the past year, especially in

contrast to the rising the gold price, but expenses could rise substantially starting this

quarter if the conflict continues. The gold stocks far underperformed overall equity

markets, which held up relatively well given the surge in risk, with the S&P 500 down

-1.2%, the Nasdaq actually gaining 0.3% and the Russell 2000 declining -3.2%.

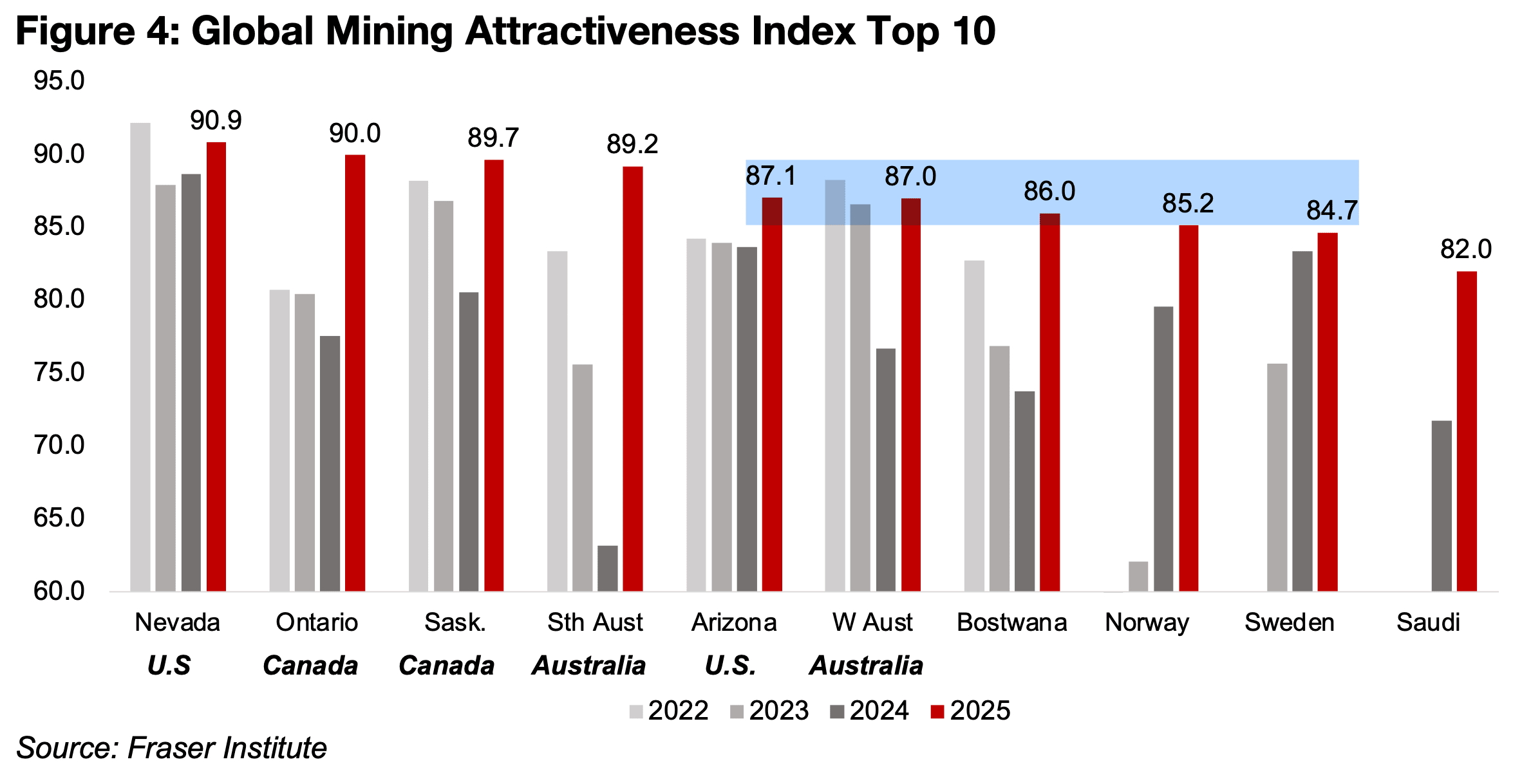

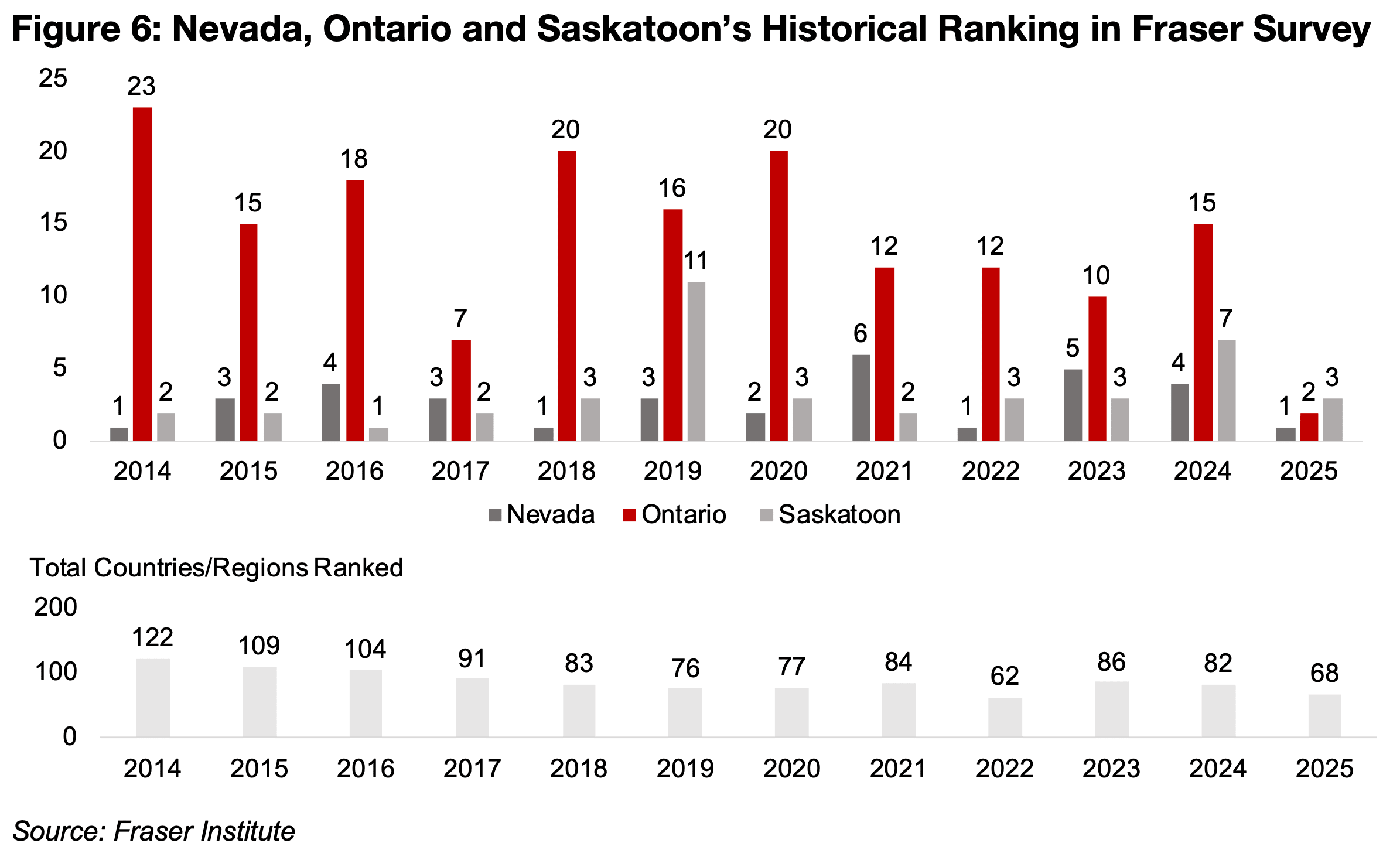

The Fraser Institute has released its Survey of Mining Companies for 2025, with

Canada ranking highly for the Mining Investment Attractiveness Index, with Ontario

and Saskatchewan taking the second and third spots, with Nevada in the U.S. the

leader (Figure 4). The US had another state in the top ten, Arizona, at fifth, with

Australia also having two high ranking states at fourth and sixth place. Both Africa

and Europe had two countries in the top ten, with Botswana and Saudi at seventh

and tenth place, and Norway and Sweden ranking eighth and ninth, respectively.

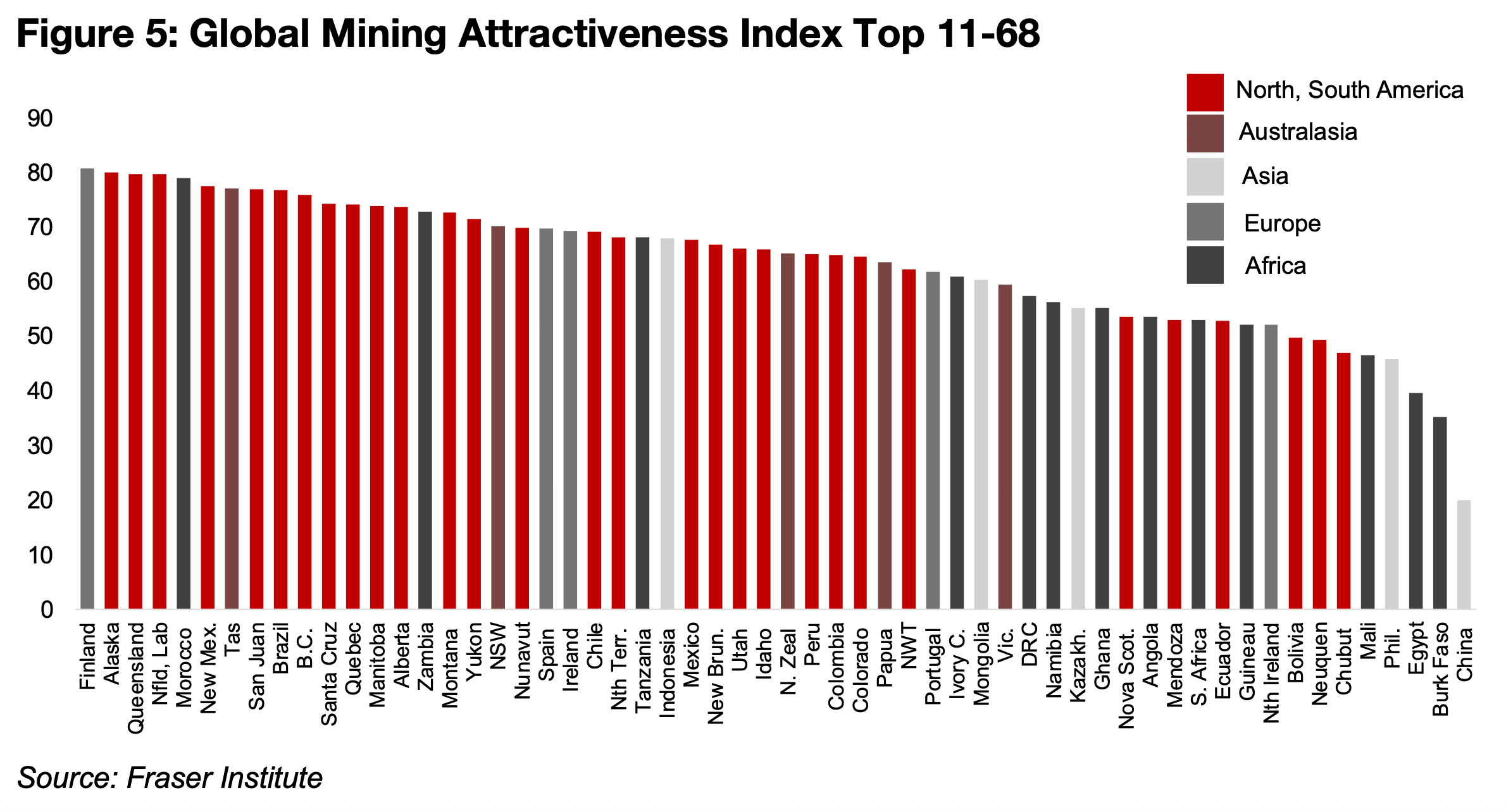

Outside of the top ten, North and South America were by far the most represented in

the Index given the concentration of mining activity in those regions, tending towards

higher rankings, but also with some jurisdictions seeing low scores (Figure 5).

Most of the African countries were towards the lower end of the ranking, mainly from

issues with political stability. Australasia, mostly comprising Australian provinces,

was reasonably evenly distributed in the top three quarters of the ranking, with no

jurisdictions in the bottom quartile. Europe was also represented relatively evenly

through the ranking, with Asia jurisdictions mainly in the bottom half. While Nevada

has consistently ranked in the top five for the Survey since 2014, and Saskatchewan

often placed highly, Ontario being near the top is a new development, with it mostly

out of the top ten and sometimes at 20 or lower (Figure 6).

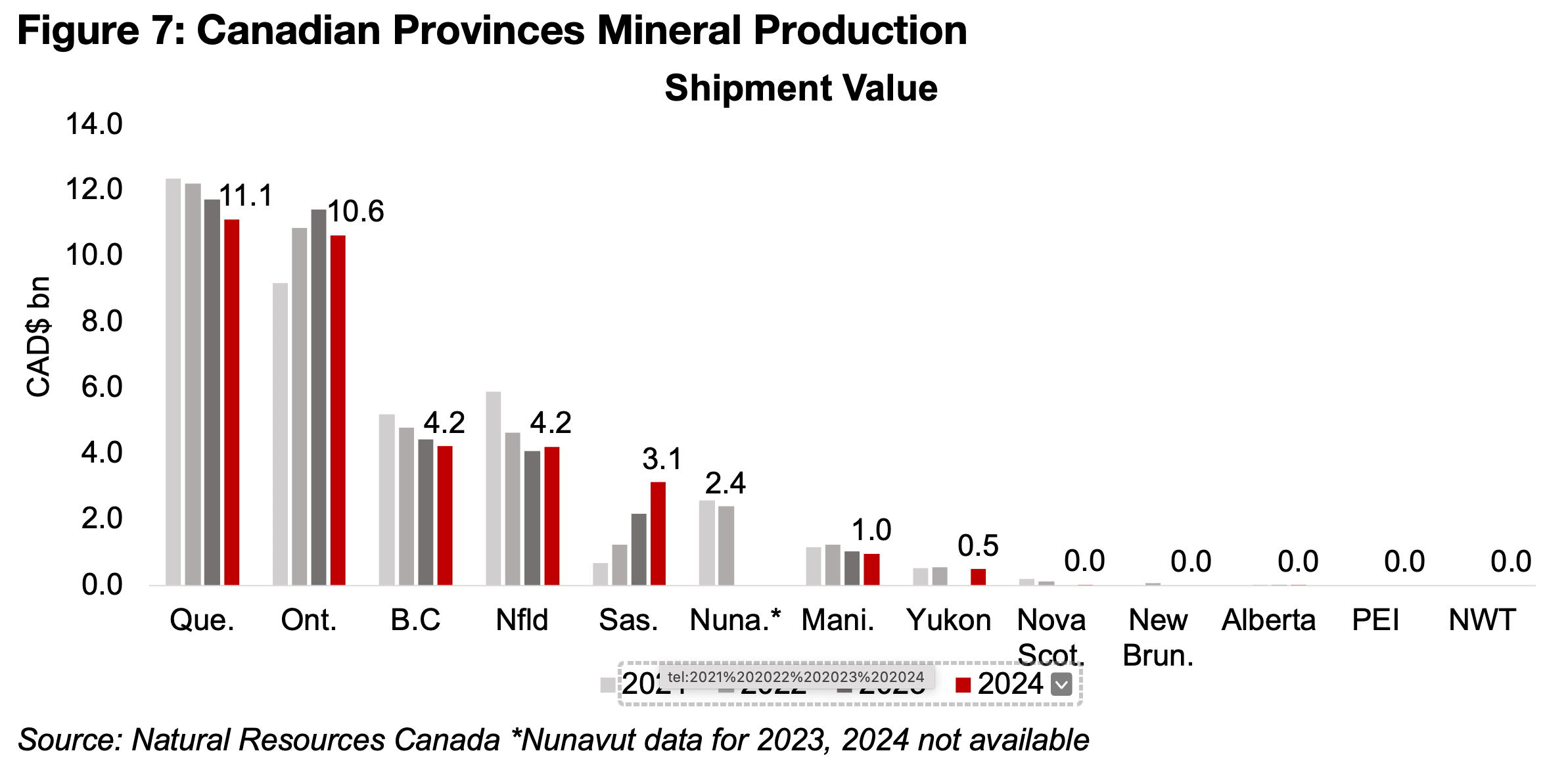

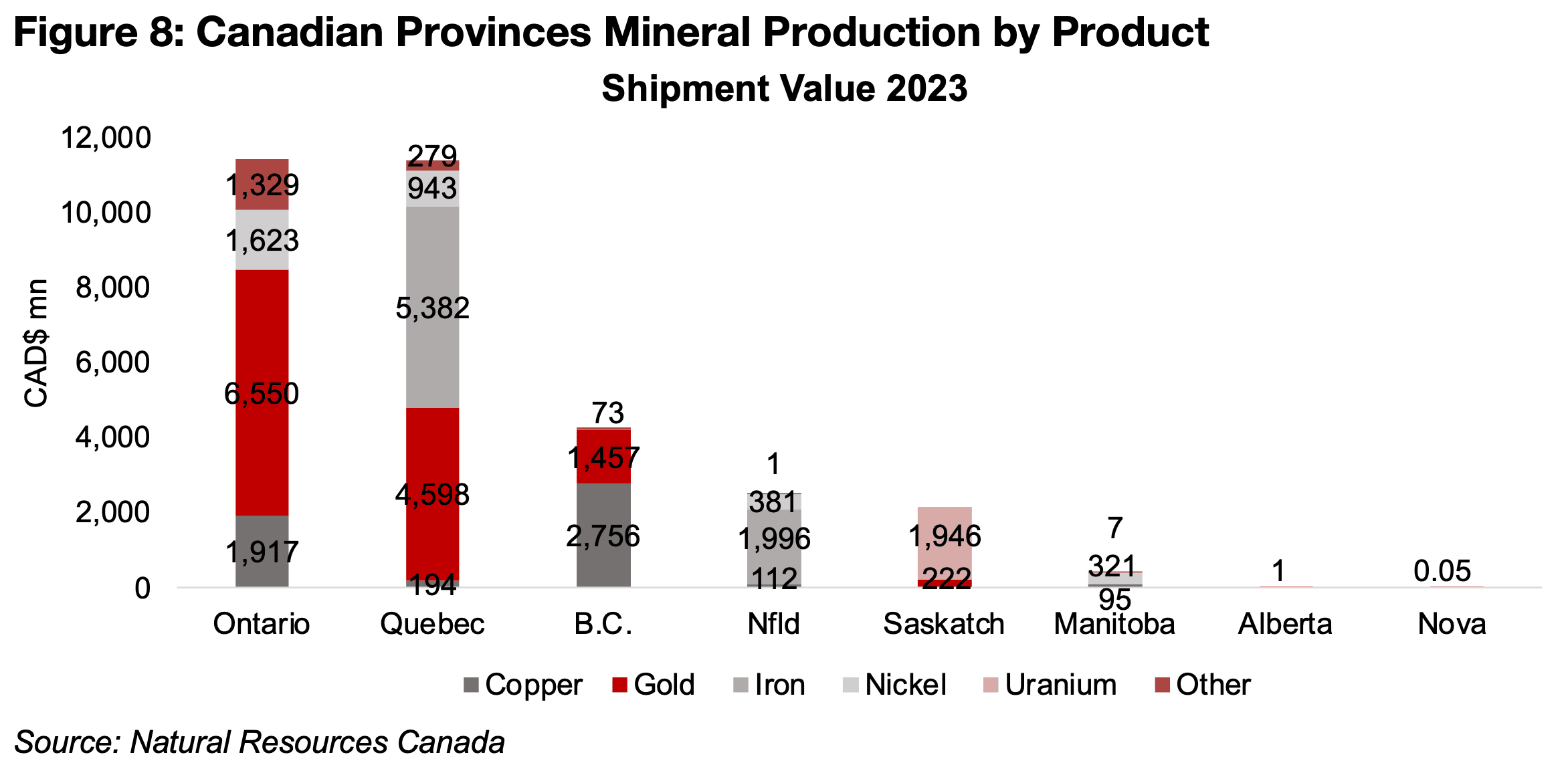

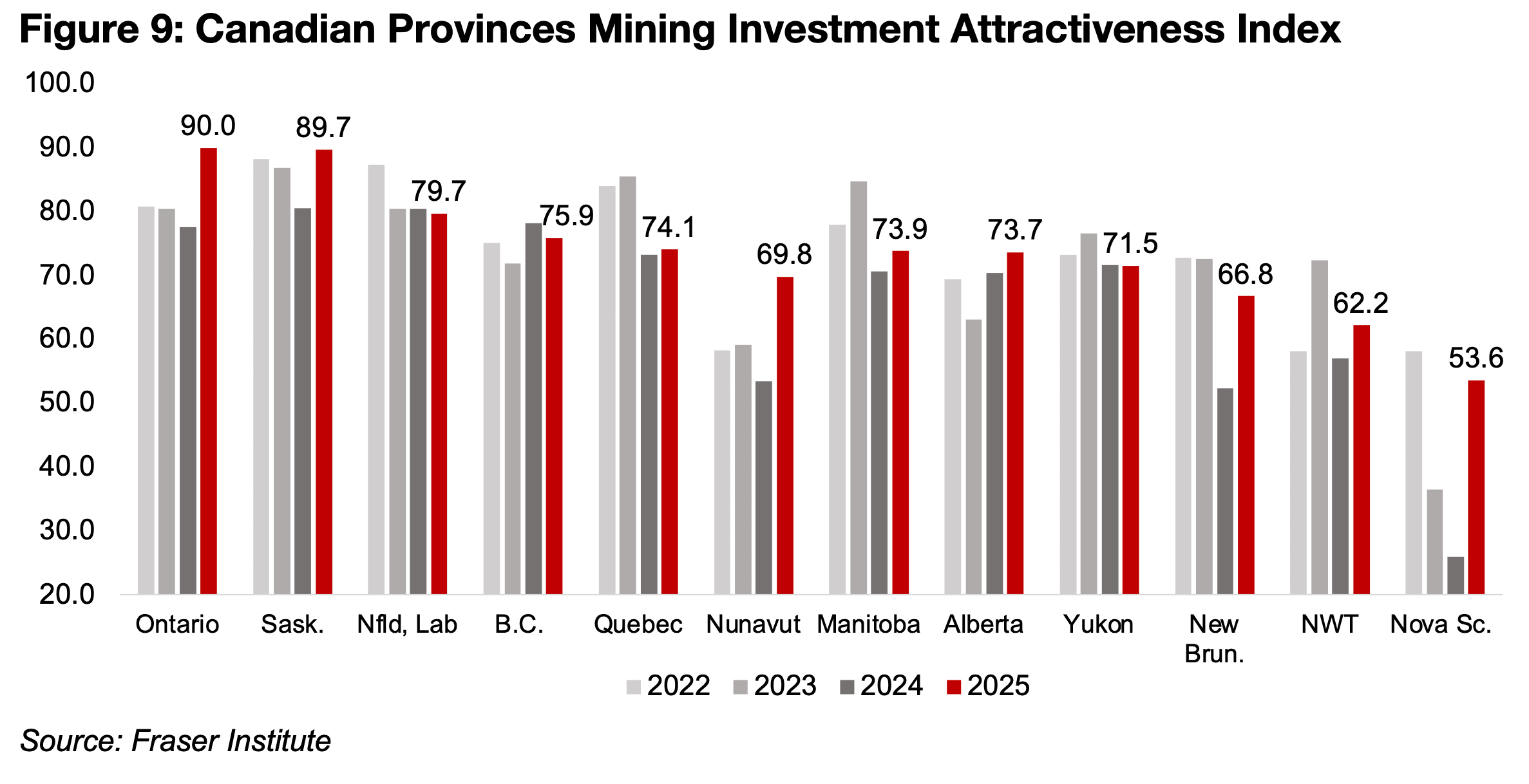

While Ontario is a leading province for mineral production, with shipment value at CAD$10.6bn in 2024, second to Quebec, at CAD$11.1bn, Saskatchewan is a relatively small player, with shipment value of CAD$3.1bn, the fifth largest (Figure 7). Ontario’s shipments were heavily concentrated in gold, with contributions also from copper and nickel, while Saskatchewan’s revenue is mainly from uranium (Figure 8). There are several provinces in the Survey that are not major mineral producers, Nova Scotia, New Brunswick, Alberta, Prince Edward Island and the Northwest Territories.

The Fraser Survey’s Investment Attractiveness Index is a combination of the Best Practices Mineral Potential Index, which has a 60% weight, and the Policy Perceptions Index, with a 40% weight. The Survey highlighted that the jump in Ontario’s ranking has been driven especially by an improvement in its Policy Perceptions Index, with concerns over taxation issues, skilled labour availability and political stability in the province decreasing significantly (Figure 9). For Saskatchewan, the Survey highlights the strong Policy Perception ranking for the province, with concerns decreasing over skilled labor availability, taxation and security.

For the other major mineral producing provinces, Newfoundland’s Investment

Attractiveness Index ranking has remained relatively flat since a decline in 2023, with

a slight decline in 2025 on issues regarding regulations and the legal system,

including duplication, inconsistencies, administration and enforcement. B.C. is near

its 2022 levels, with uncertainty over protected areas, disputed land claims and

environmental regulations holding down the index. Quebec edged up in 2025 after a

major decline in 2024, with lower concerns over the province’s tax and legal systems

and environmental regulations. Nunavut saw a major increase from a relatively weak

level for the index from 2022-2024.

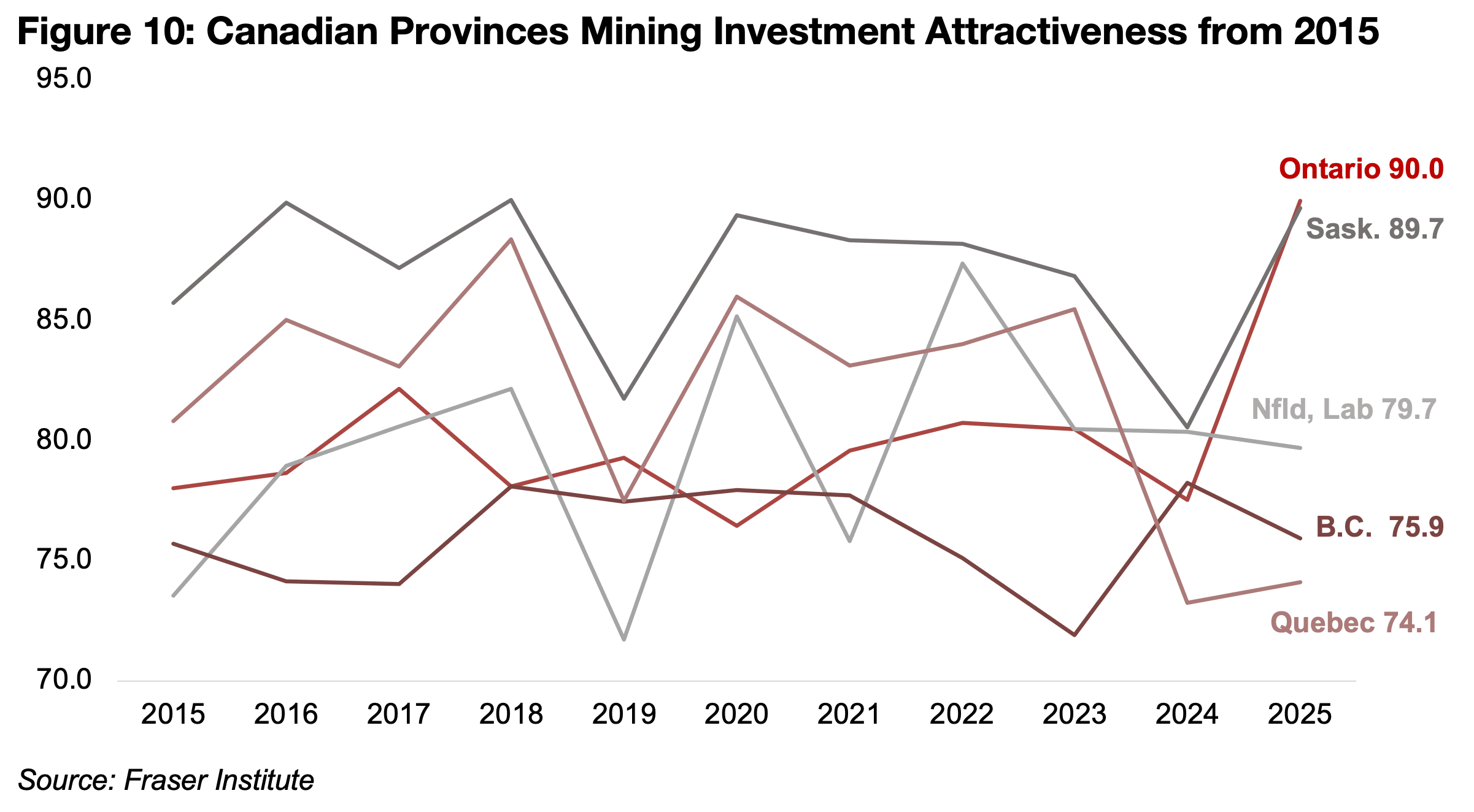

The Mining Investment Attractiveness Index for Ontario reaching 90.0 particularly

stands out, as it had rarely been above 80.0 from 2015 to 2025, while Saskatchewan

had reached similar levels to 2025 in several previous years (Figure 10). The decline

for Quebec to just 74.1 has been significant as it generally was well above 80.0 for

the previous ten years. Newfoundland’s index has been more volatile, ranging from

just above 70.0 to over 85.0, with its level in 2025 near the middle of this range, and

British Columbia’s lower ranking of 75.9 is actually towards the higher end of the past

ten years.

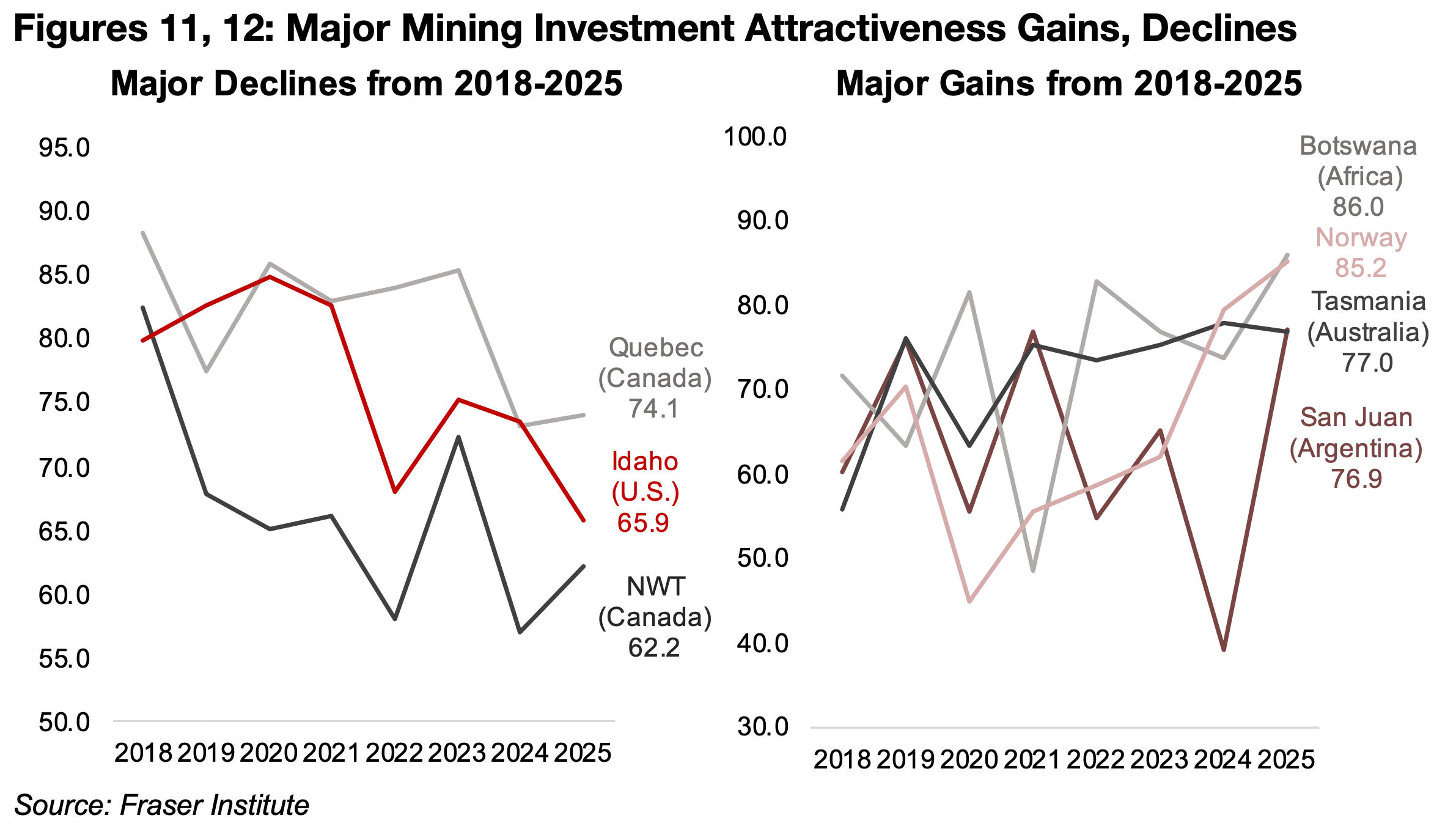

In the medium-term two Canadian provinces have had some of the most major

declines in their Investment Attractiveness Indices for regions with consistent data

from 2018 to 2025. Quebec has had third largest decline, from nearly 90.0 in 2018 to

just 74.1 in 2025, while the Northwest Territories has had the largest point drop in the

survey, by 26.2, from 82.5 to 62.2 (Figure 11).

Idaho in the US has also seen a major decline in its Investment Attractiveness Index

from 79.9 in 2018 to 65.9 in 2025. The biggest gainers from 2018 to 2025 have been

Botswana, up from 71.7 to 86.0 and Norway from 61.7 to 85.2, with both moving into

the top ten for the first time last year. Tasmania in Australia, up from 60.3 to 77.0 and

San Juan in Argentina, rising from 55.9 to 76.9, have also made substantial gains over

the period (Figure 12).

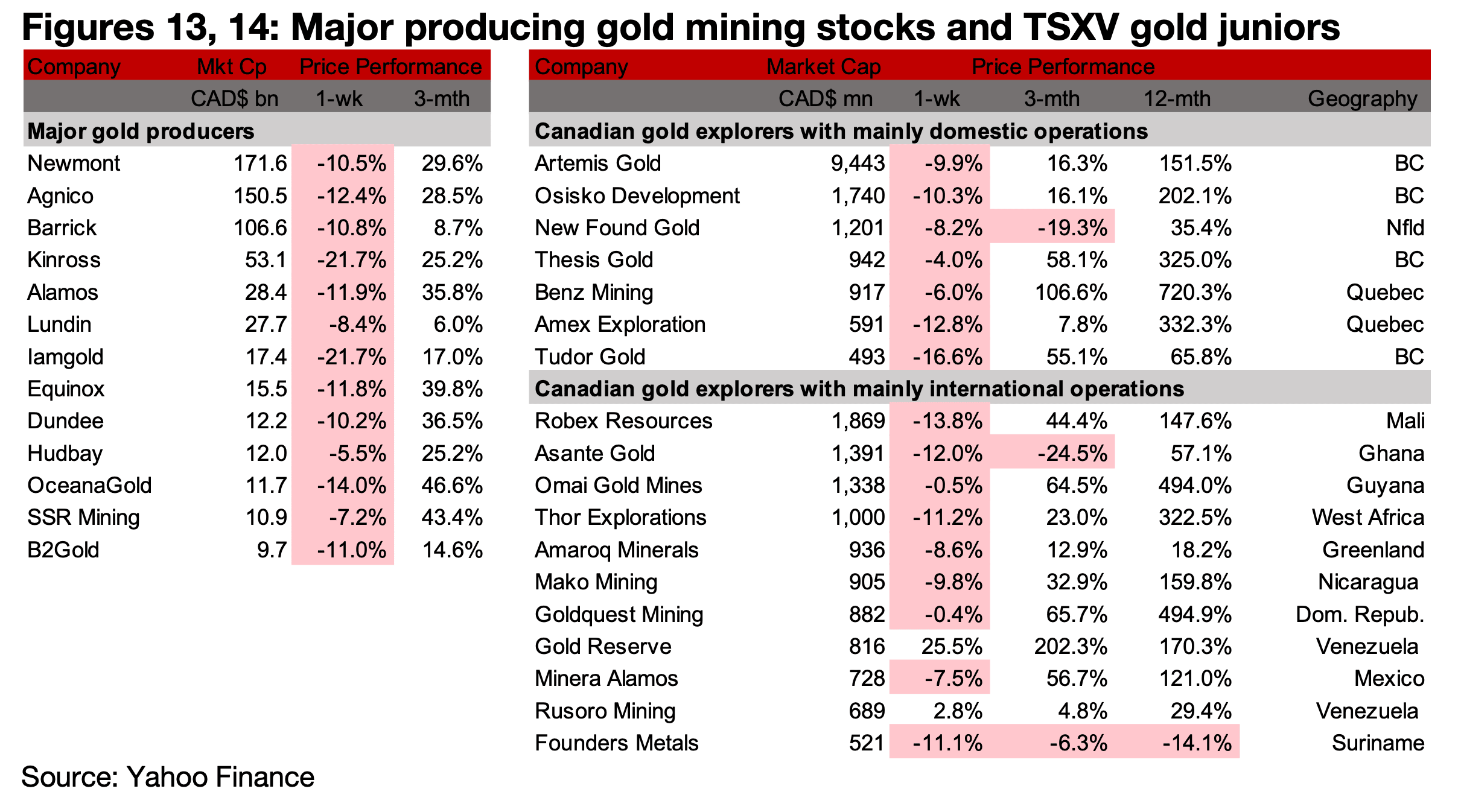

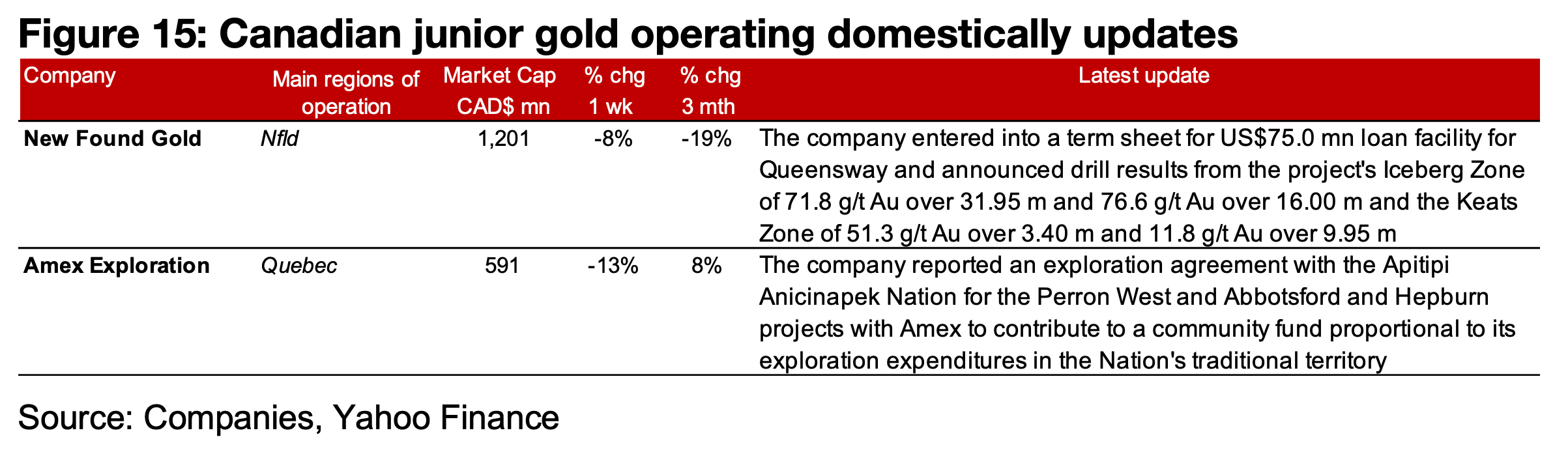

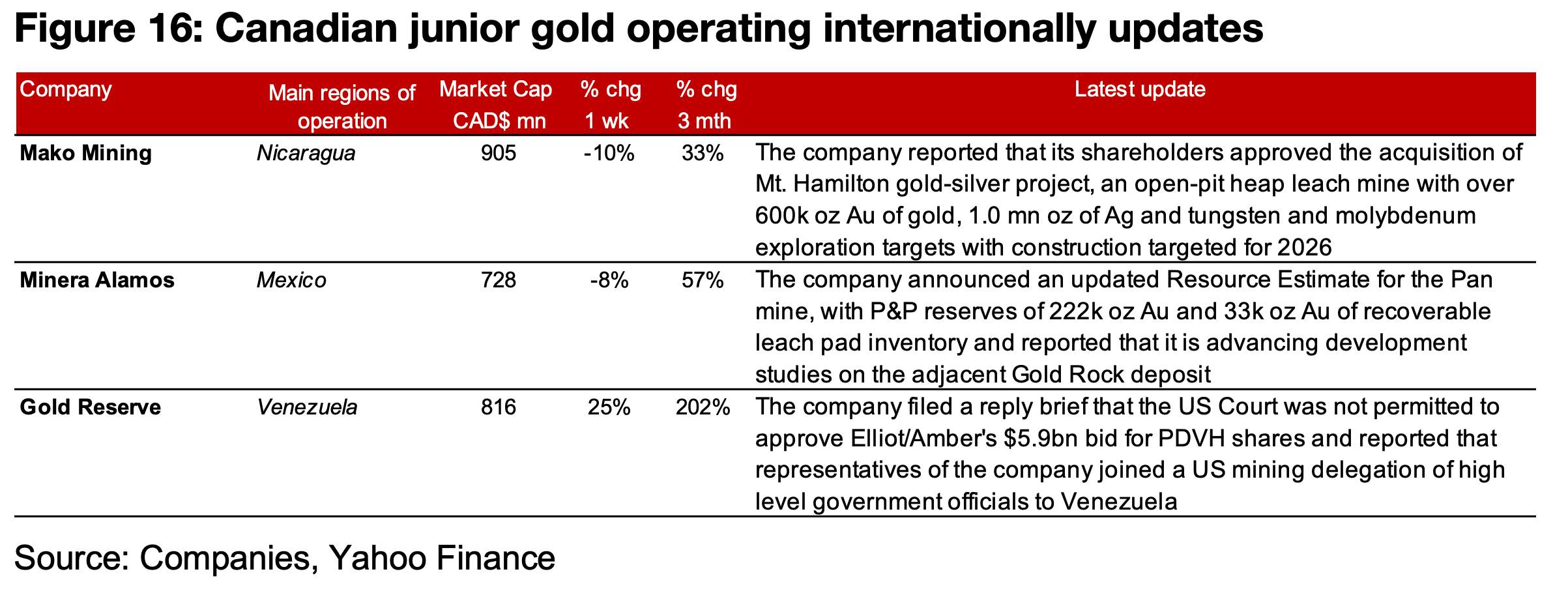

All of the major producers and most of TSXV gold saw major declines as the gold price edged down and oil prices jumped (Figures 13, 14). For the TSXV gold companies operating mainly domestically, New Found Gold entered into a term sheet for a US$75.0mn loan facility for Queensway and reported drill results from the Iceberg and Keats Zone of the project, and Amex reported an exploration agreement with the Apitipi Anicinapek Nation for the Perron West and Abbotsford and Hepburn projects (Figure 15). For the TSXV gold companies operating mainly internationally, Mako reported that shareholders approved the acquisition of the Mt. Hamilton project and Minera Alamos announced an updated Resource Estimate for the Pan mine. Gold Reserve filed a reply brief with the US Court that it was not permitted to approved Elliot/Amber’s bid for PDVH shares and reported that rep

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.

Author

Ben McGregor authors the Weekly Roundup at CanadianMiningReport.com, providing sharp analysis of the metals and mining sector. With a talent for spotting trends, Ben distills complex market shifts into clear, engaging insights on TSXV junior miners. His weekly updates cover gold, copper, uranium, and more, blending data-driven perspectives with a knack for identifying opportunities. A vital resource for investors, Ben’s work navigates the dynamic junior mining landscape with precision.