May 25, 2026

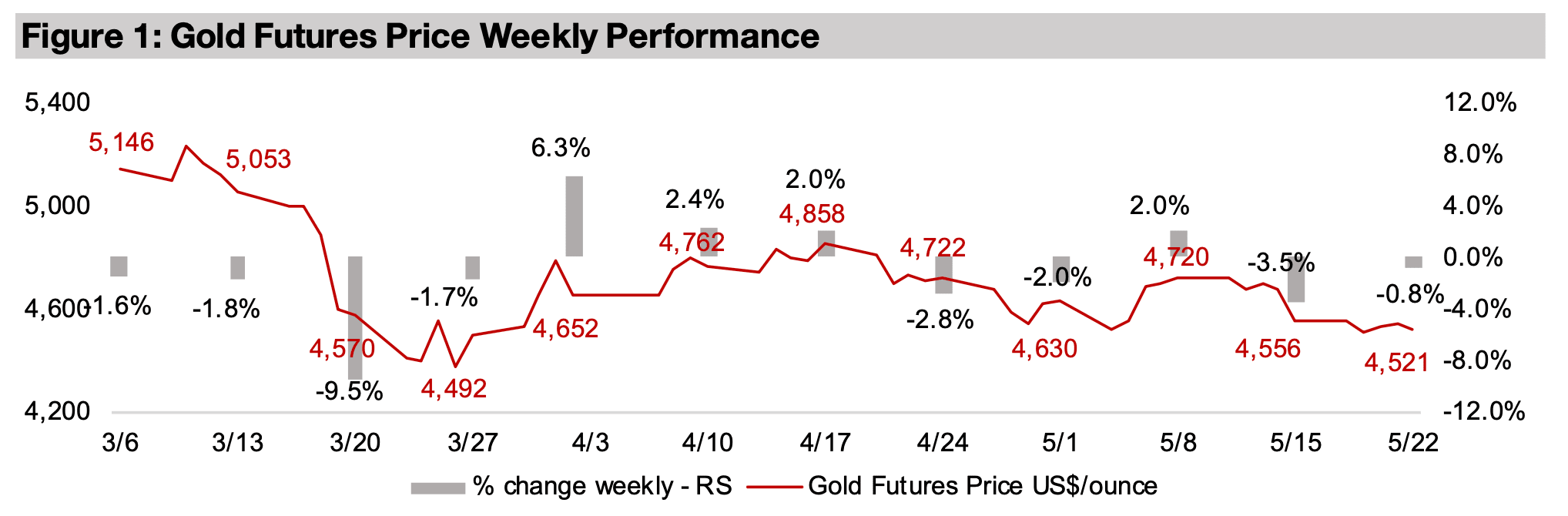

Gold edged down -0.8% to US$4,521/oz, heading back towards the lows for the year as major economic news was limited, especially versus last week’s inflation shock, and the appointment of the new Fed Chairman was already well known to the market.

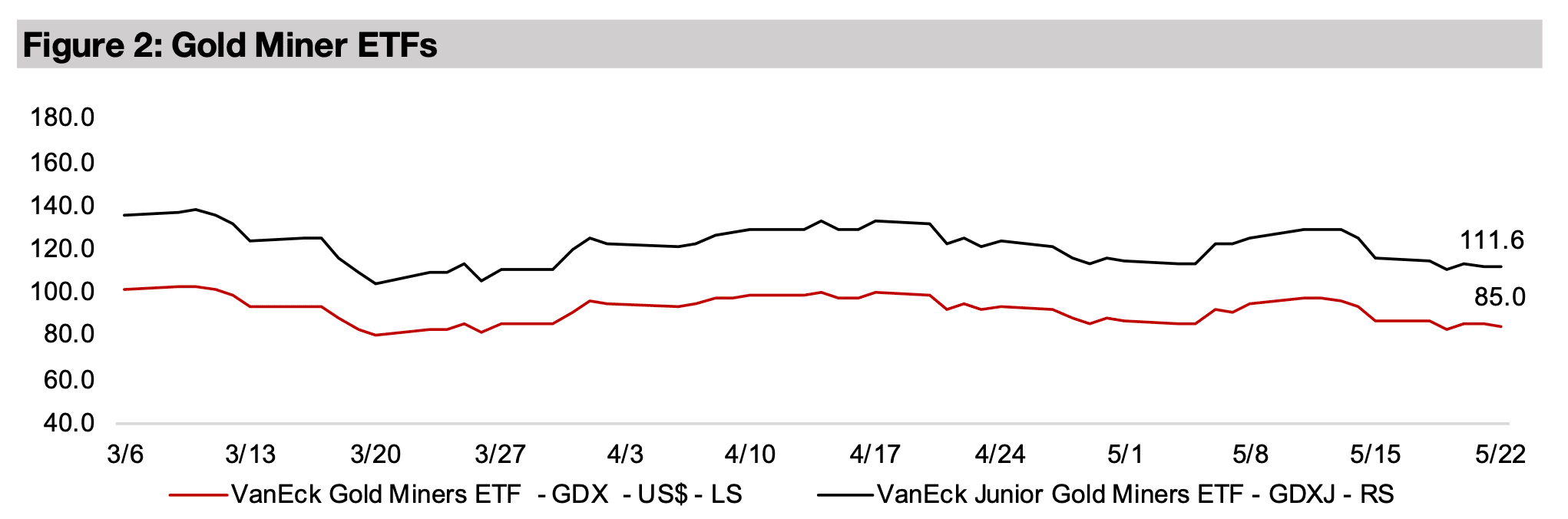

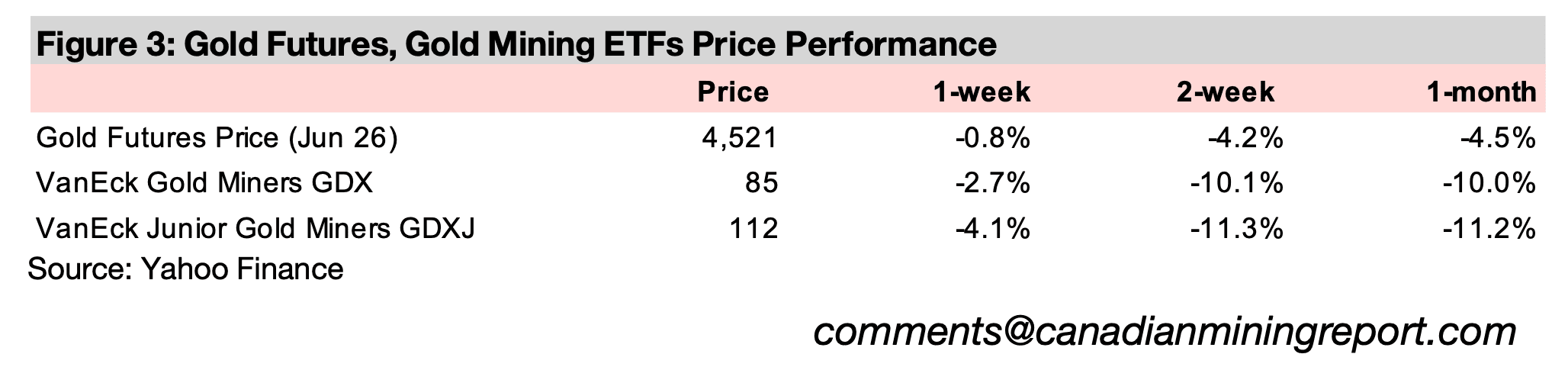

The gold stocks declined on the slide in the metal price, with the GDX down -2.7% and GDXJ off -4.1%, as equities were mixed, with the S&P 500 up 0.8% and the Nasdaq near flat, up 0.2%, outpaced by the Russell 2000 index, up 2.4%.

The gold price slid -0.8% to US$4,521/oz, heading back down towards its lows for

the year of US$4,492/oz, as the markets were mixed, with signs that the risk-on rally

may be losing steam and becoming more scattered, the large cap S&P 500 up 0.8%,

but the tech-driven Nasdaq near flat, up 0.2%, and the small caps still jumping, with

the Russell 2000 up 2.4%. The economic news was less explosive than the inflation

shock of last week, with some pull back in oil prices as there seems to have been

some progress on a US-Iran deal. While the new Fed Chairman Warsh started this

week, the appointment was already well-known to the market and unlikely had a

major effect on market movements.

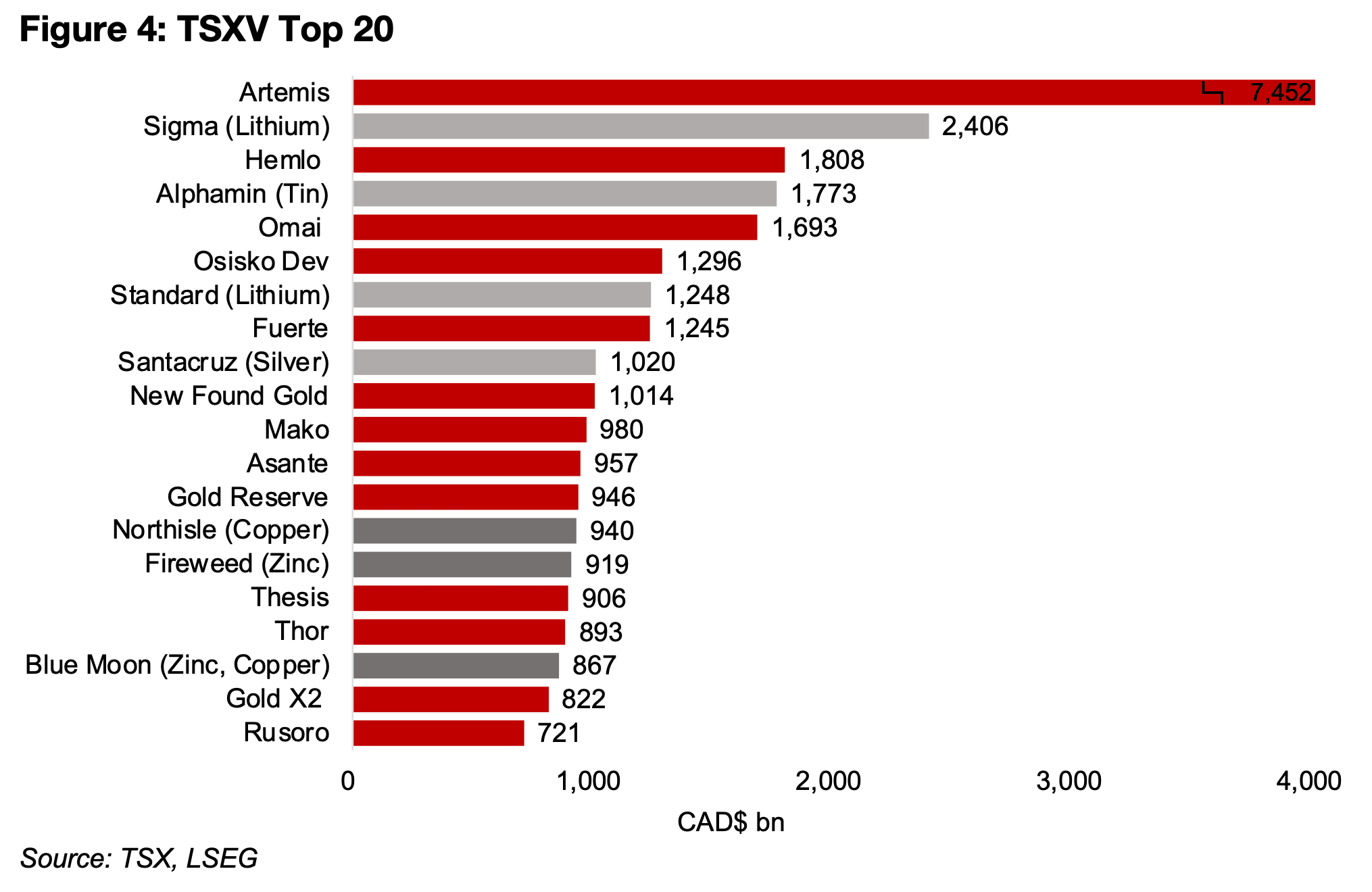

TSXV large copper, zinc and tungsten stocks on the rise

While the TSXV Mining Top 20 by market cap, excluding royalties companies, is

dominated by gold companies, with 13 in total, there are also three major base metals

players, Northisle Copper and Gold, zinc and tungsten developer Fireweed and

copper, zinc and tungsten developer Blue Moon (Figure 4). The others are two lithium

companies, Sigma and Standard and silver and tin producers Santacruz and

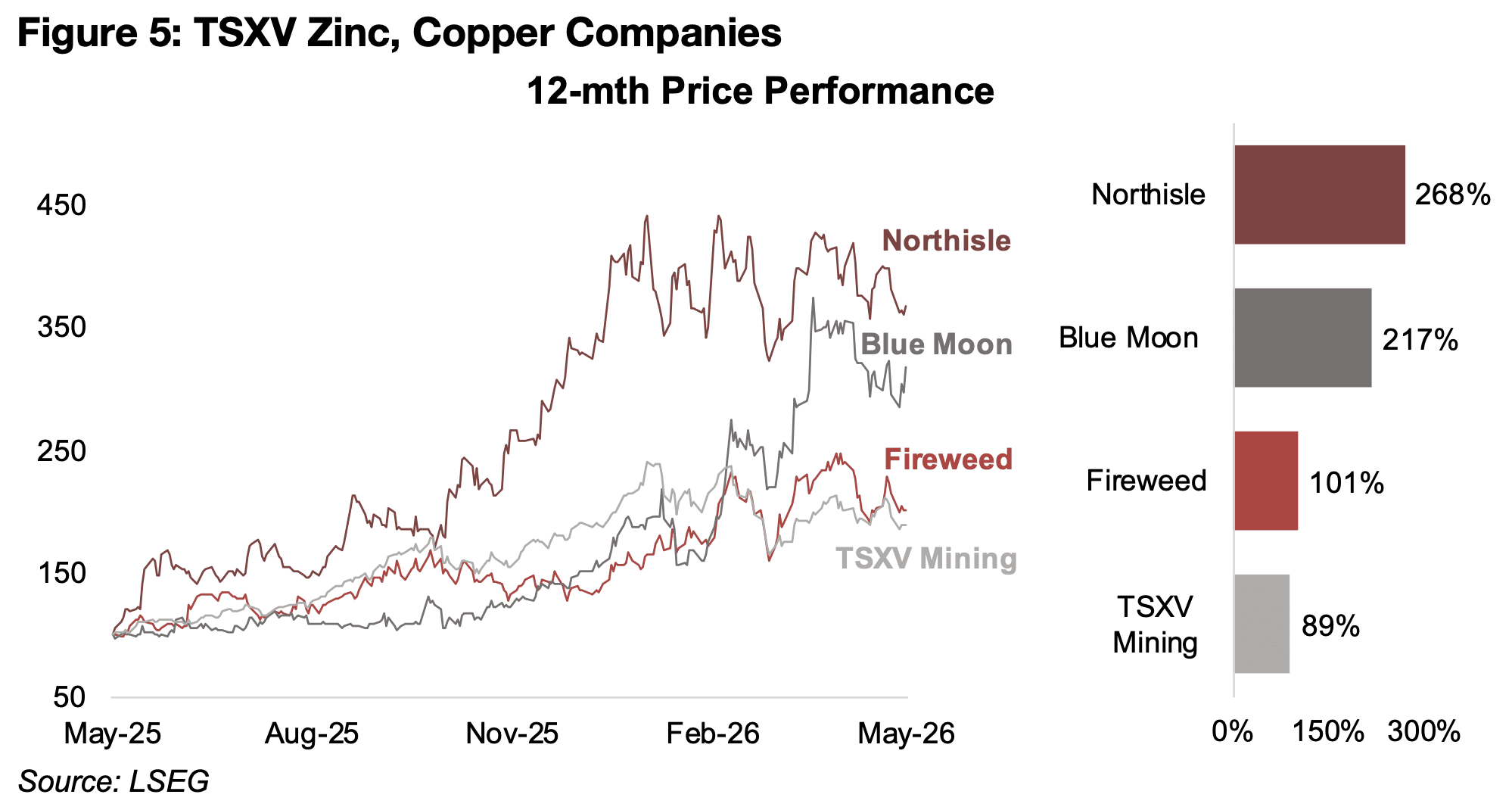

Alphamin. All three have seen strong price performances over the past year, with

Northisle the strongest, up 268%, Blue Moon increasing 217% and Fireweed up

101%, outperforming the 89% gain for the TSXV Mining Index (Figure 5)

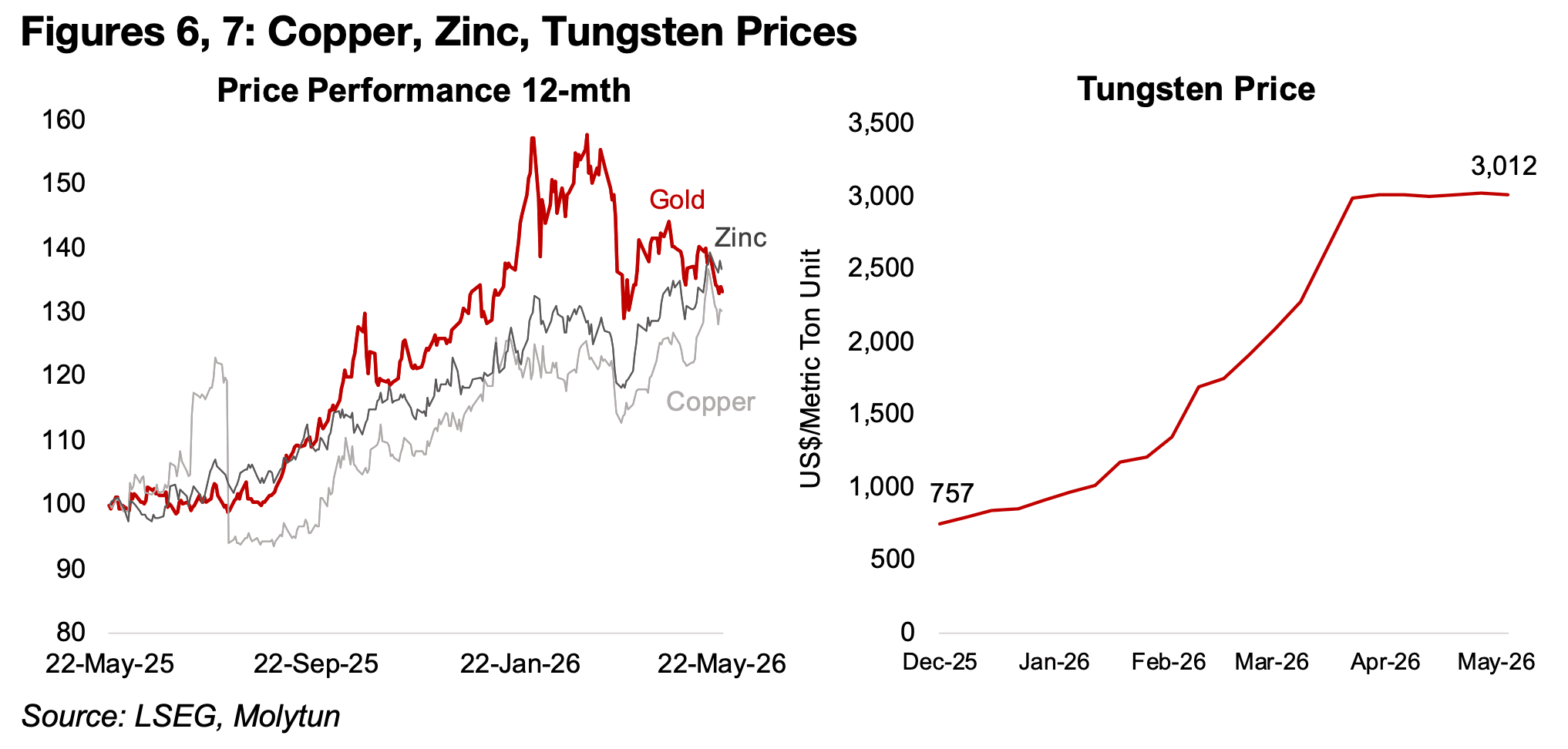

The share prices of these companies have been driven partly by strong gains for copper and zinc prices, with performances broadly inline with gold price over 12- mths, with latter slightly above and the former slightly below (Figure 6). However, the biggest outperformer of the key metals underlying these companies has been tungsten, which has risen more than four times since December 2025 (Figure 7).

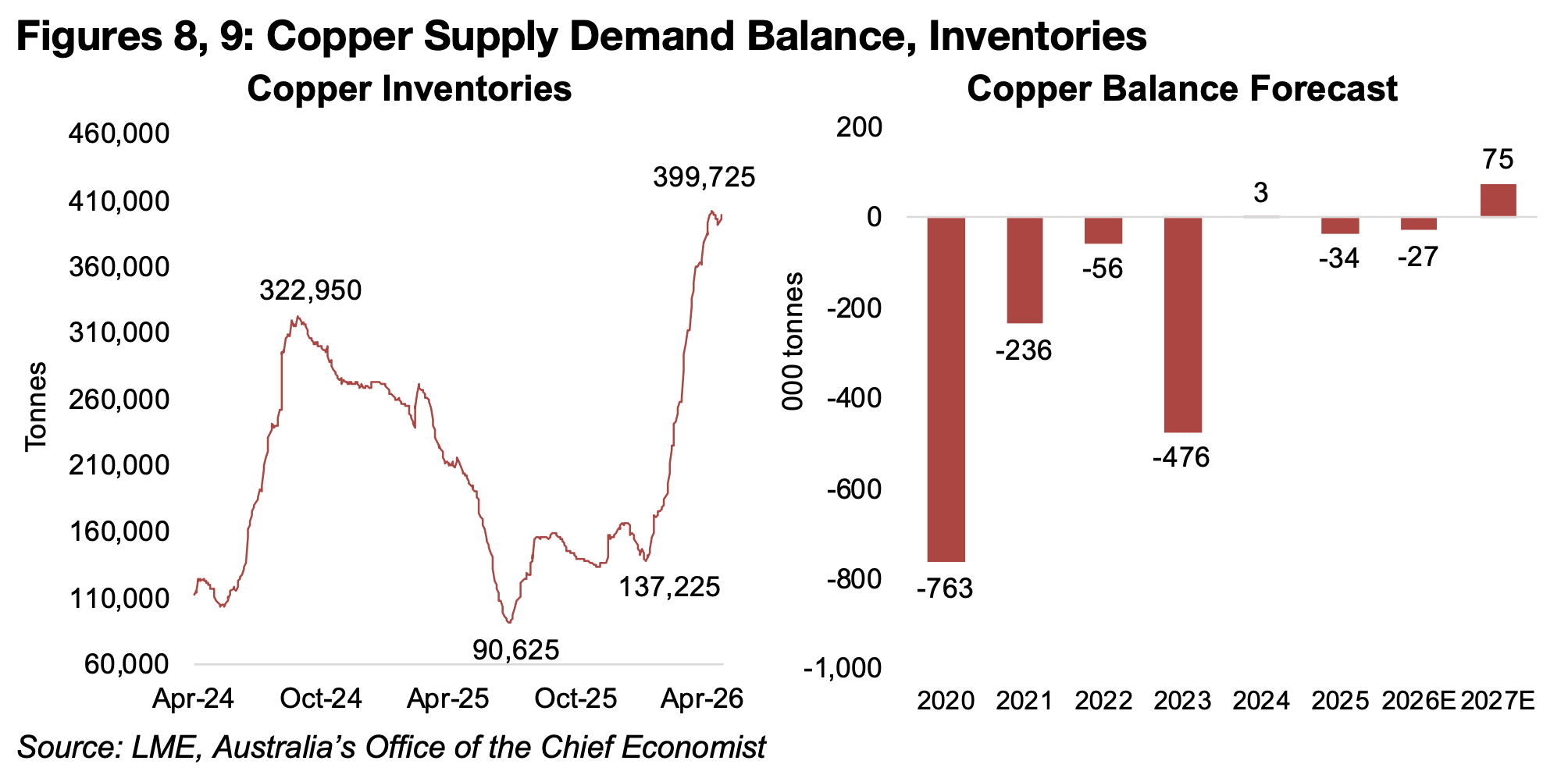

While the copper price has been driven especially by strong demand related from the

AI sector, there are concerns over the sustainability of this boom. Inventories of the

metal have also rebounded substantially from mid-2025 lows and the distortions of

last year related to tariffs in the US seem to be unwinding (Figure 8).

While the copper market is currently forecast to be in a slight deficit for 2026E

especially on continued low supply from Indonesia’s Grasberg, a surplus is forecast

for 2027E, which could put some pressure on the price (Figure 9). These estimates

from Australia’s Office of the Chief Economist (AOCE) are also from December 2025,

with the regular March 2026 update not released given the lack of clarity following

the start of the war. As since late 2025 copper demand has outpaced expectations

and there may been additional supply issues from the energy crisis in Peru, which is

the third largest global supplier of the metal, there are likely to be major adjustments

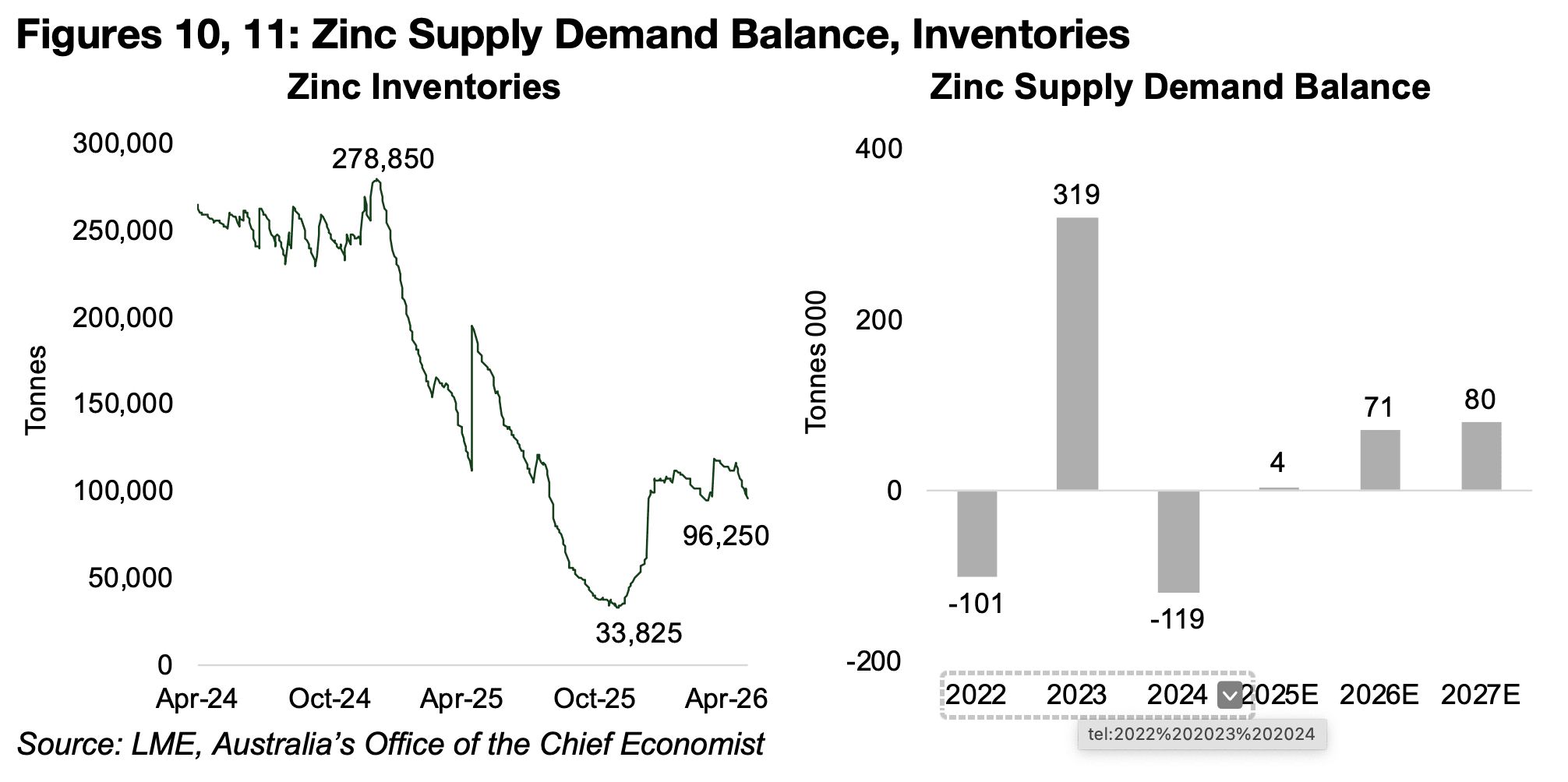

to these forecasts when the AOCE releases its June 2026 estimates. While zinc

inventories also rebounded from late 2025, they remain well below late 2024 highs,

and a considerable surplus is also expected for 2026E-2027E (Figures 10, 11).

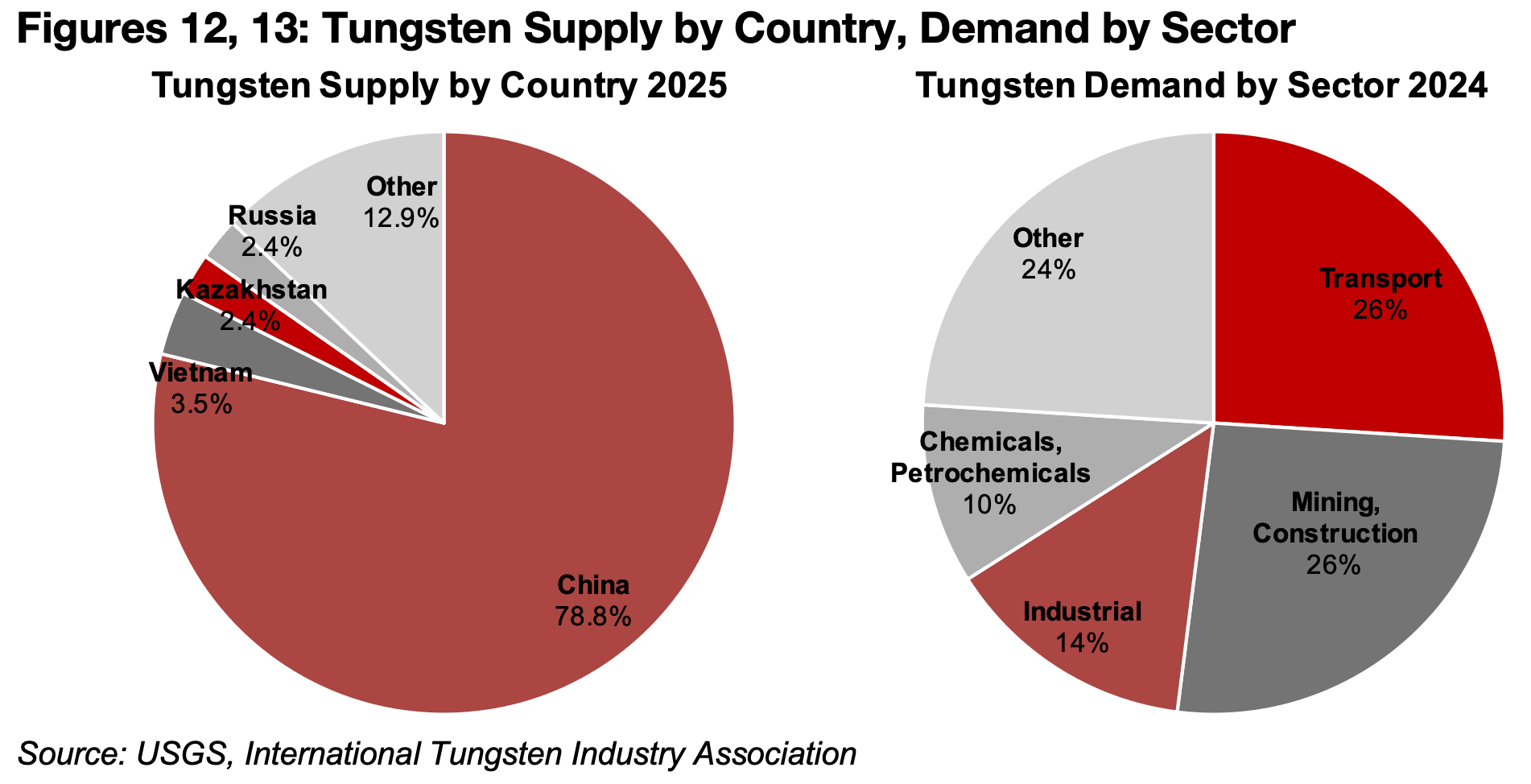

The main driver of the surge in the tungsten price has been export controls from China, which accounted for the majority of supply, at 78.8%, in 2025, inline with broader control of critical minerals in the country since late 2025 and given the metal’s significant military applications (Figure 12). Demand for the metal has been strong from the military sector on rising geopolitical risk but also from tech (Figure 13).

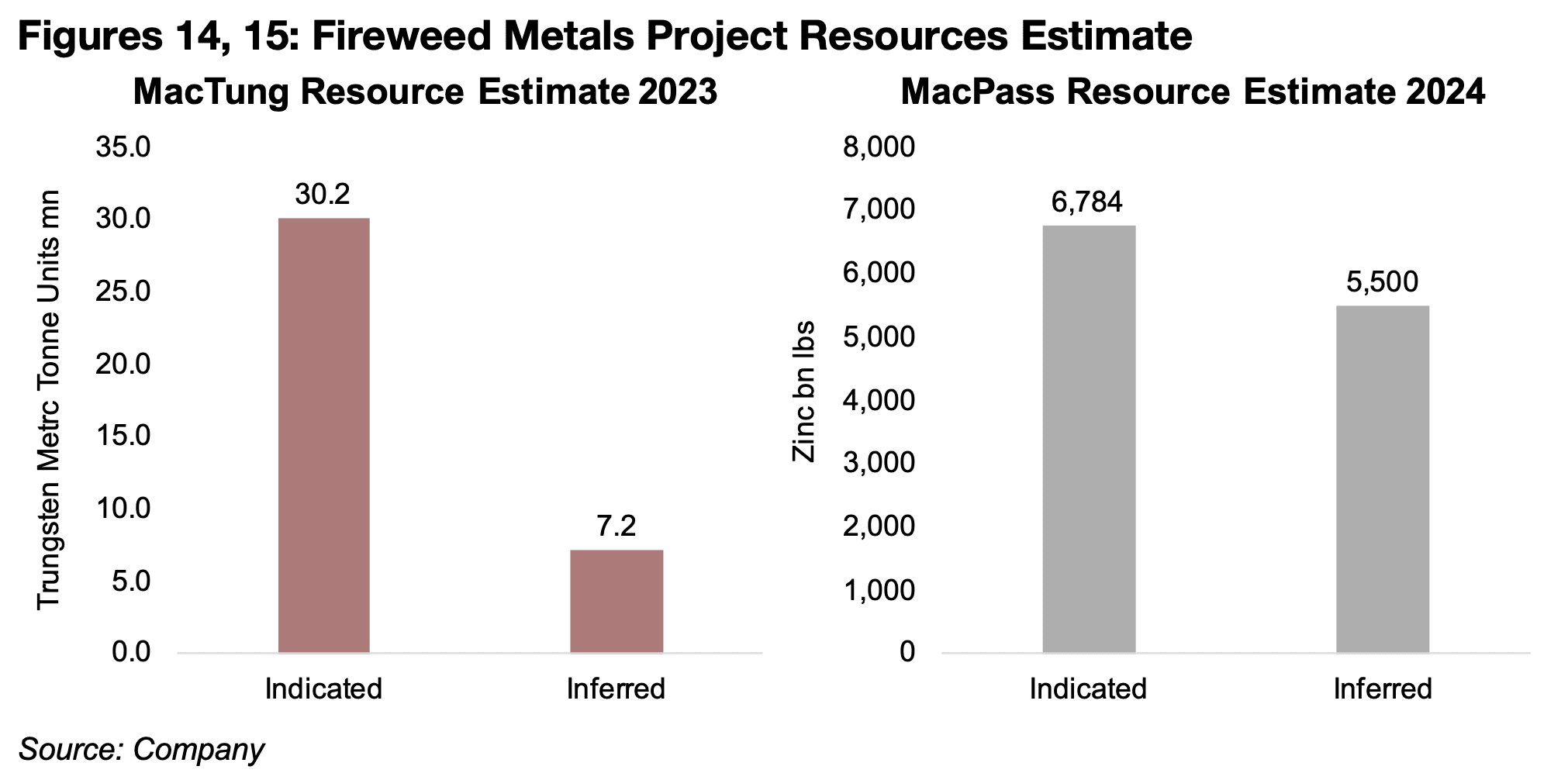

Fireweed Metals has two major projects, both in the Yukon, with MacTung’s

Resource Estimate from 2023 showing 30.2 mn Indicated and 7.2 mn Inferred Metric

Ton Units of tungsten and an FS was started in March 2026. The MacPass Resource

Estimate shows 6,784 bn Indicated and 5,500 bn Inferred tonnes of zinc, and also

substantial lead and silver, and drilling at the project continues (Figures 14, 15).

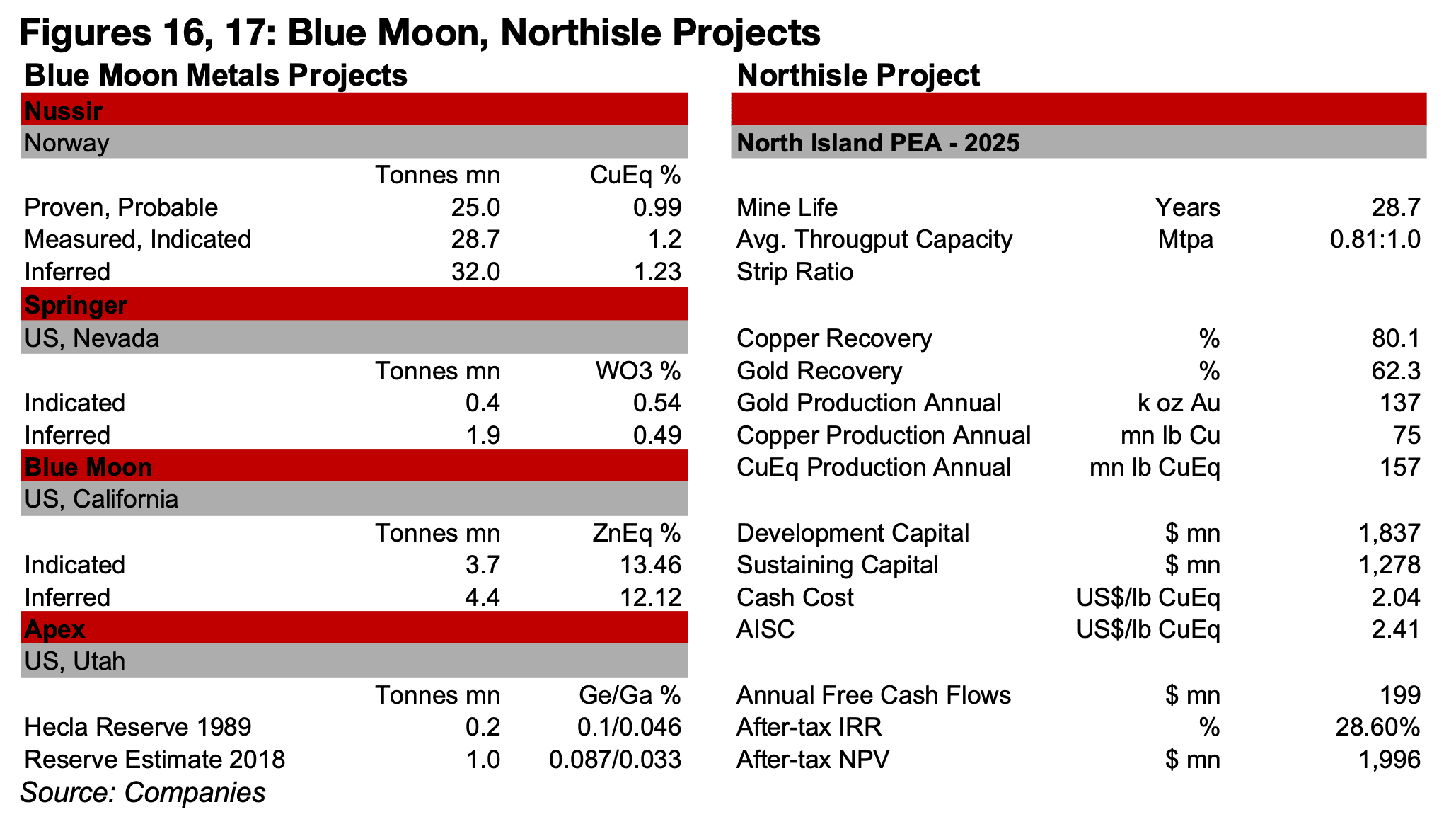

Blue Moon has four major projects, with the Nussir copper project in Norway the most

advanced, with a Feasibility Study completed, the start of construction announced in

April 2026 and production expected by Q3/27. The project has a resource of 25.0 mn

tonnes Proven and Probable Resources at 0.99% CuEq, 28.7 mn tonnes Measured

and Indicated at 1.2% CuEq and 32.0 mn tonnes Inferred at 1.23% CuEq (Figure 16).

The Springer tungsten project is expected to start production by the fourth quarter of

next year, and the Blue Moon zinc project by 2029, with the Apex Germanium and

Gallium project at an earlier stage with metallurgical work ongoing.

Northisle Copper and Gold is at the PEA stage for its North Island project in British

Columbia, with an estimated 157 mn lbs CuEq in production over 29 years,

development capex of $1,837 mn and sustaining capex of $1,278 mn (Figure 17). The

company continues drilling at the project with the most recent results released in

March 2026, and targets a PFS metallurgical testing program and resource update

for Q2/26 and completion of the PFS by Q4/26.

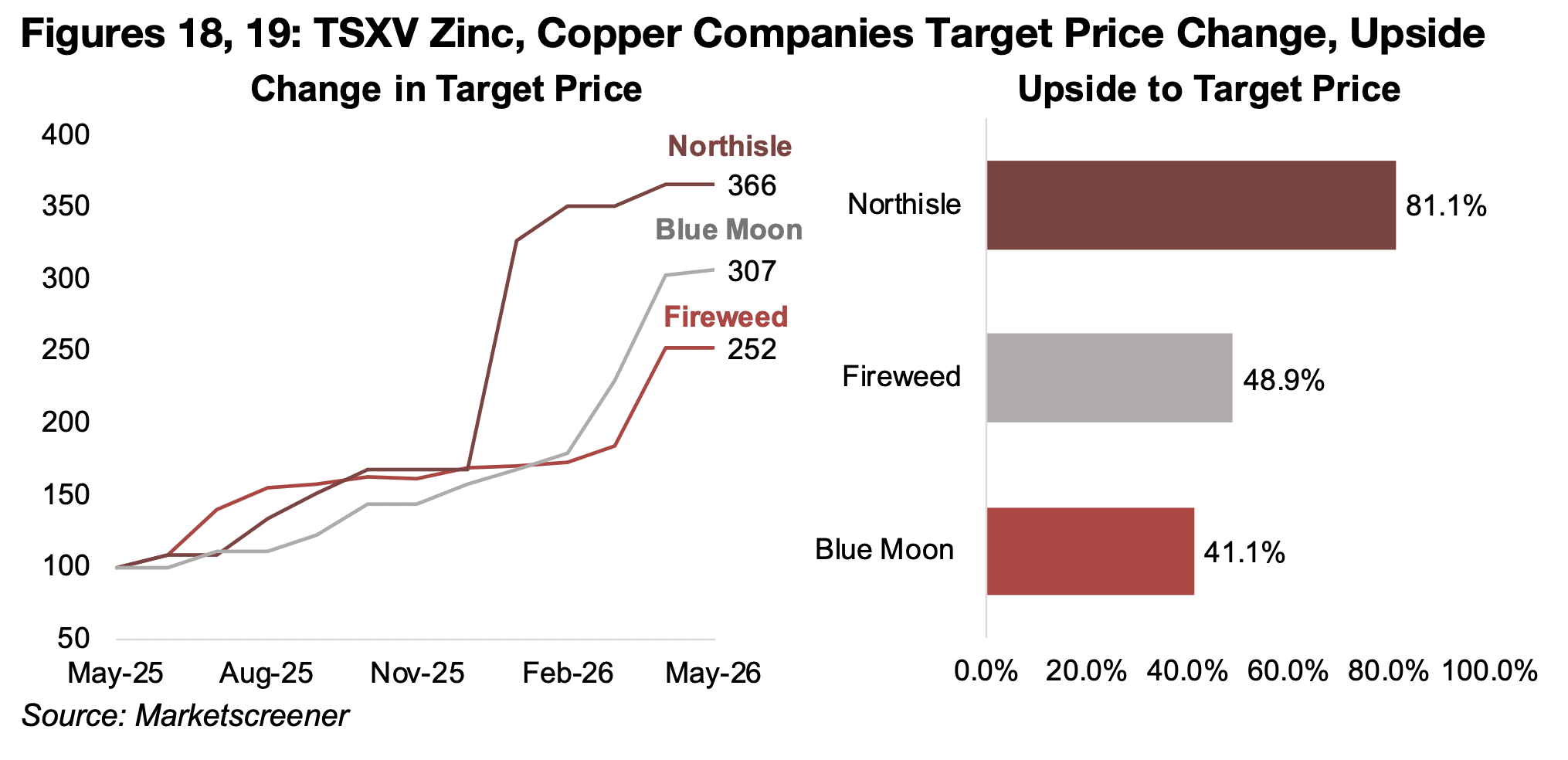

Even as the stock prices of the three companies has risen, this has still been

surpassed by the rise in the market’s consensus targets, with Northisle’s up over

250%, Blue Moon over 200% and Fireweed over 150% (Figure 18). This indicates

upside to the target price of 81.1% for Northisle, 48.9% for Fireweed and 41.1% for

Blue Moon (Figure 19).

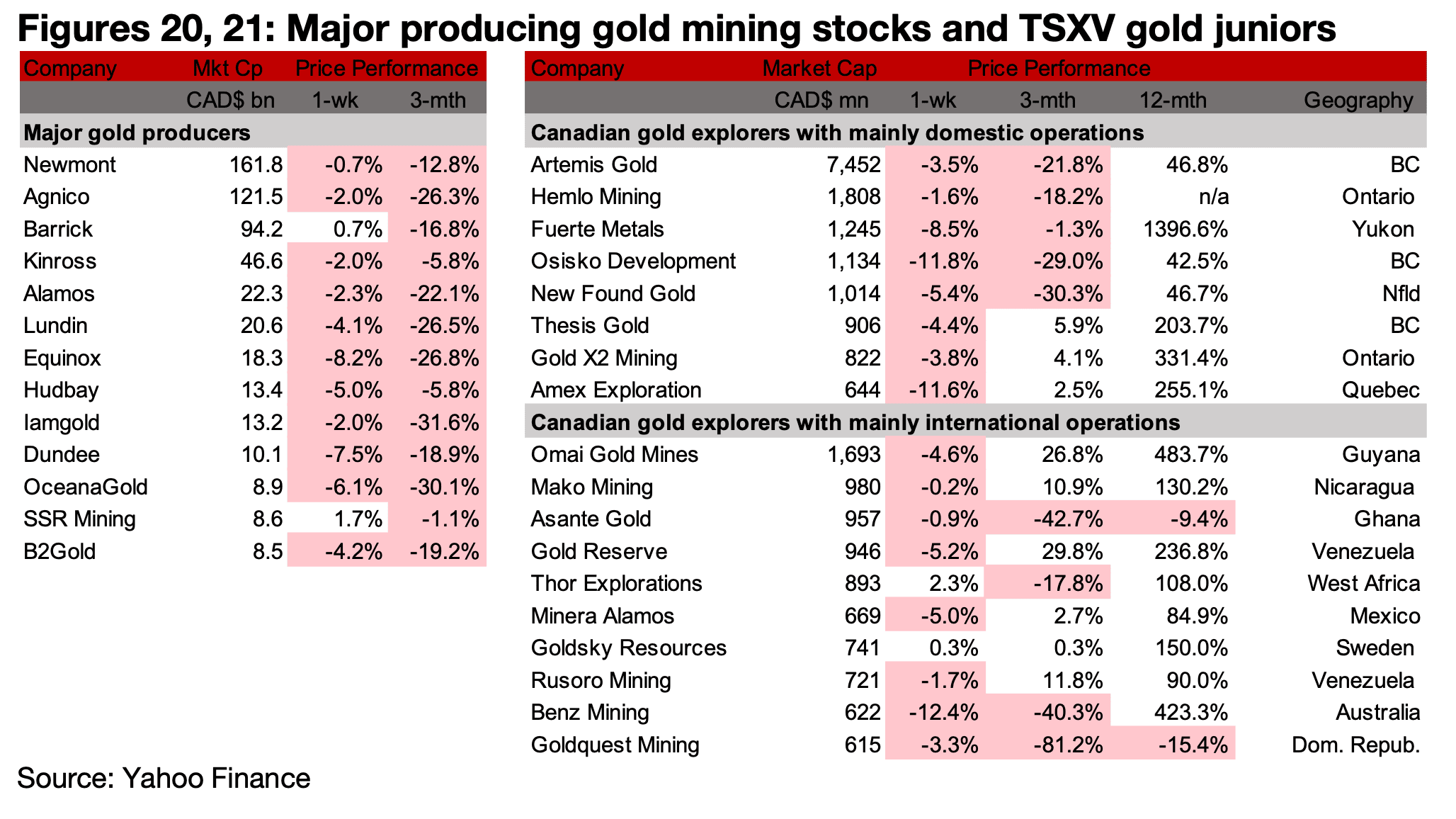

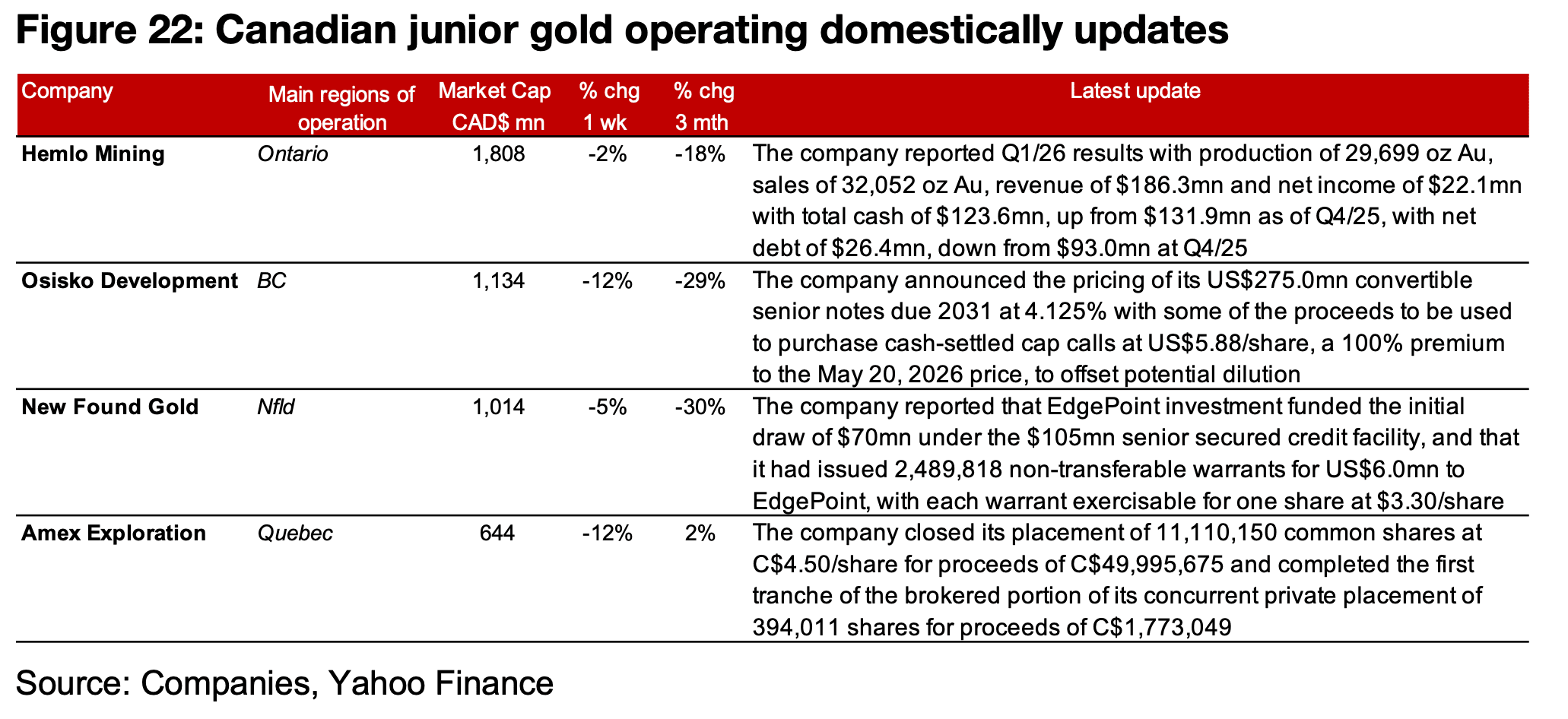

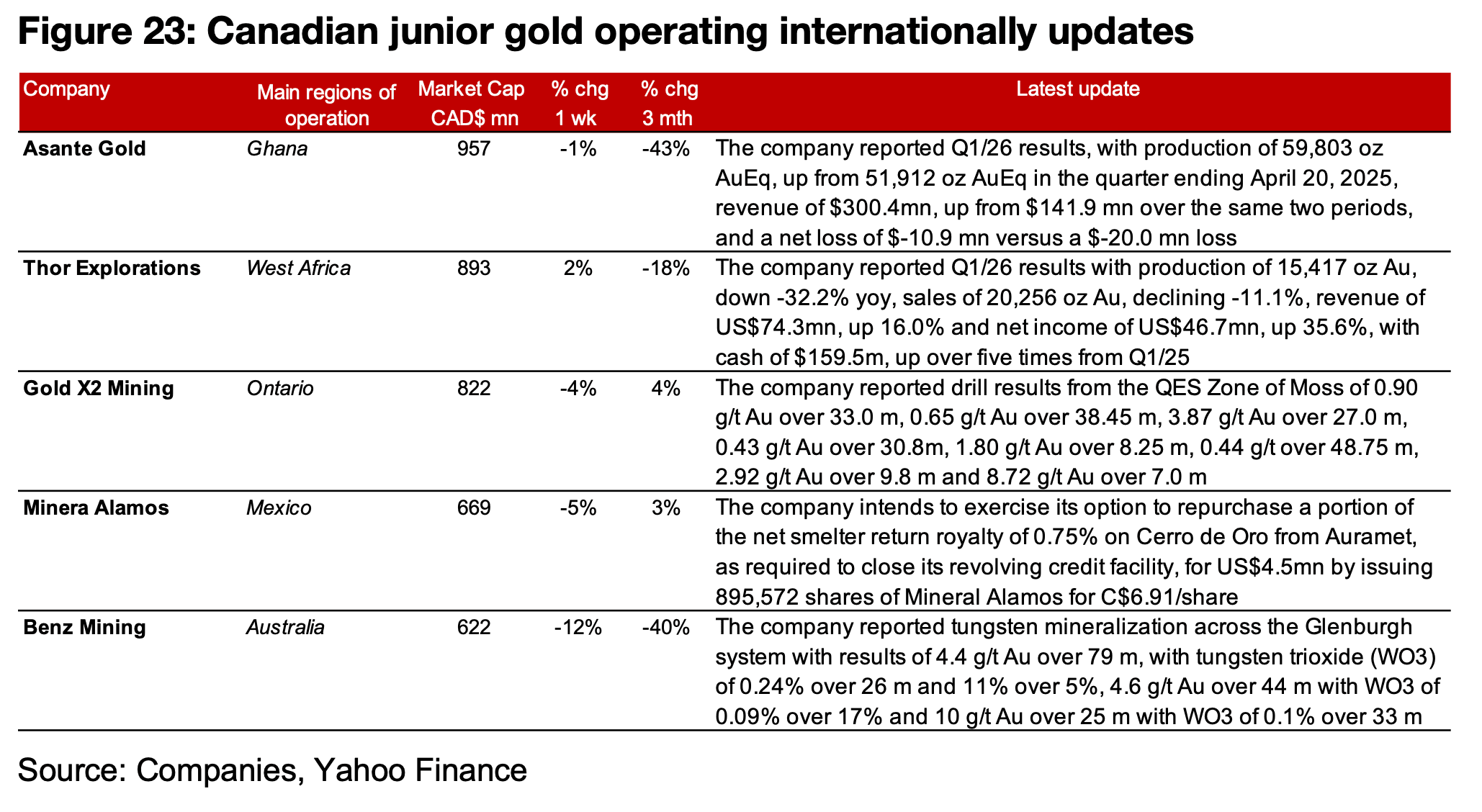

The major producers and TSXV gold were nearly all down on the drop in the gold price (Figures 20, 21). For the TSXV gold companies operating mainly domestically, Hemlo reported Q1/26 results, Osisko Development announced the pricing of its convertible senior notes, New Found Gold reported that EdgePoint funded the initial draw of its senior secured facility and Amex closed its private placements (Figure 22). For the TSXV gold companies operating mainly internationally, Asante Gold and Thor Explorations reported Q1/26 results, Gold X2 Mining announced drill results from the QES Zone of Moss, Minera Alamos announced the planned exercise of its option to purchase a net smelter return on Cerro de Oro from Auramet and Benz Mining reported tungsten mineralization as a part of gold results for Glenburgh (Figure 23).

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.

Author

Ben McGregor authors the Weekly Roundup at CanadianMiningReport.com, providing sharp analysis of the metals and mining sector. With a talent for spotting trends, Ben distills complex market shifts into clear, engaging insights on TSXV junior miners. His weekly updates cover gold, copper, uranium, and more, blending data-driven perspectives with a knack for identifying opportunities. A vital resource for investors, Ben’s work navigates the dynamic junior mining landscape with precision.