March 02, 2026

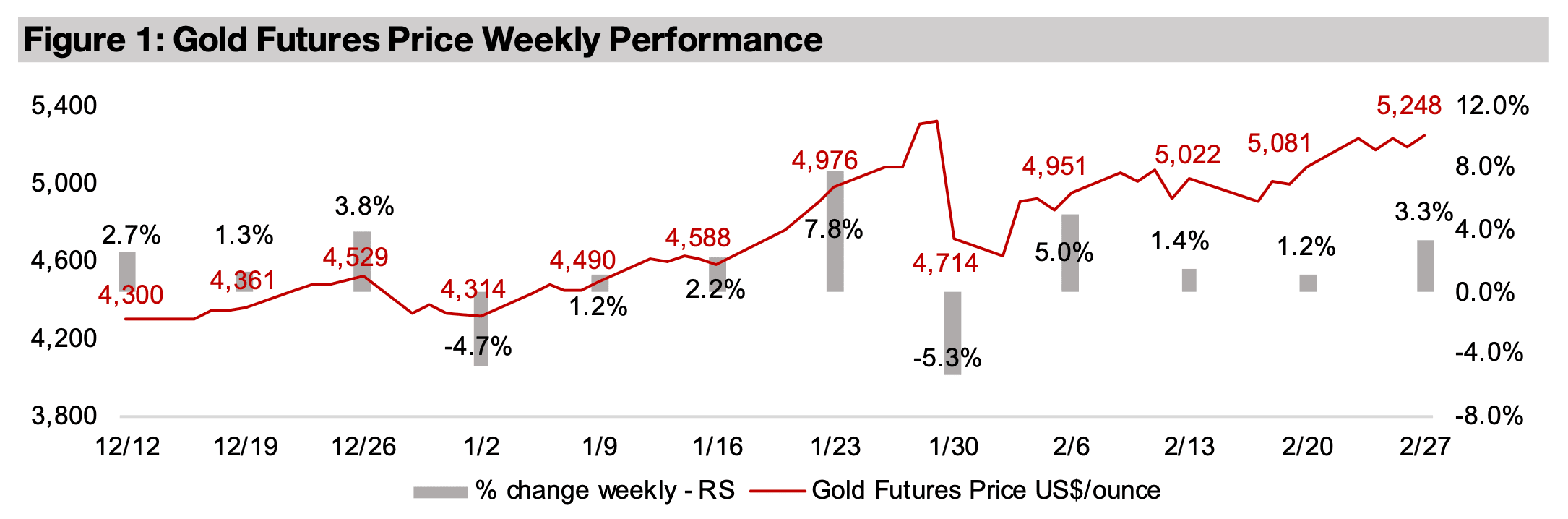

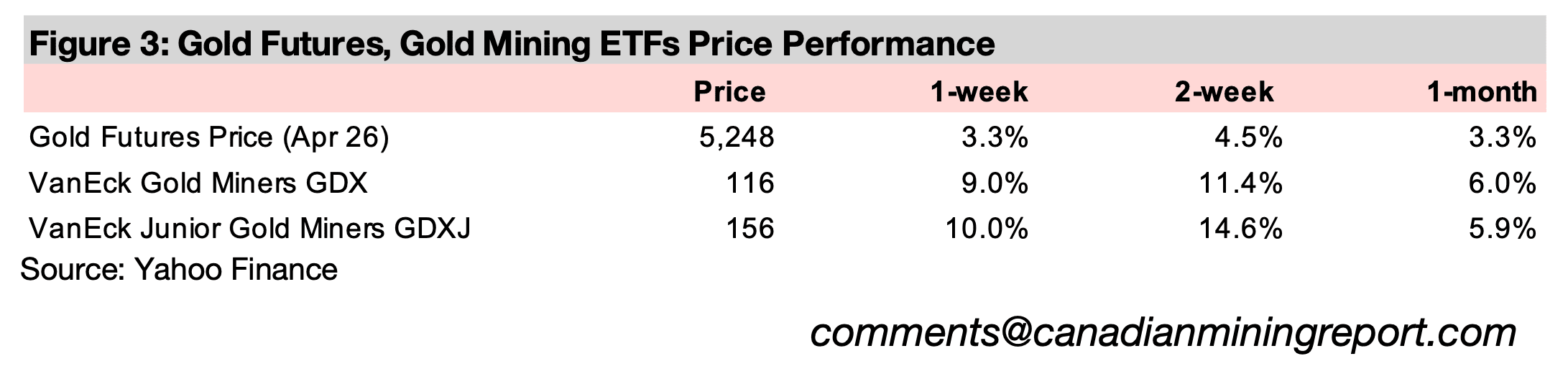

Gold rose 3.3% to US$5,248/oz, and after the huge jump in political risk over the weekend with the US attack on Iran and retaliatory strikes, its has now regained the previous highs of US$5,400/oz reached in late January 2026.

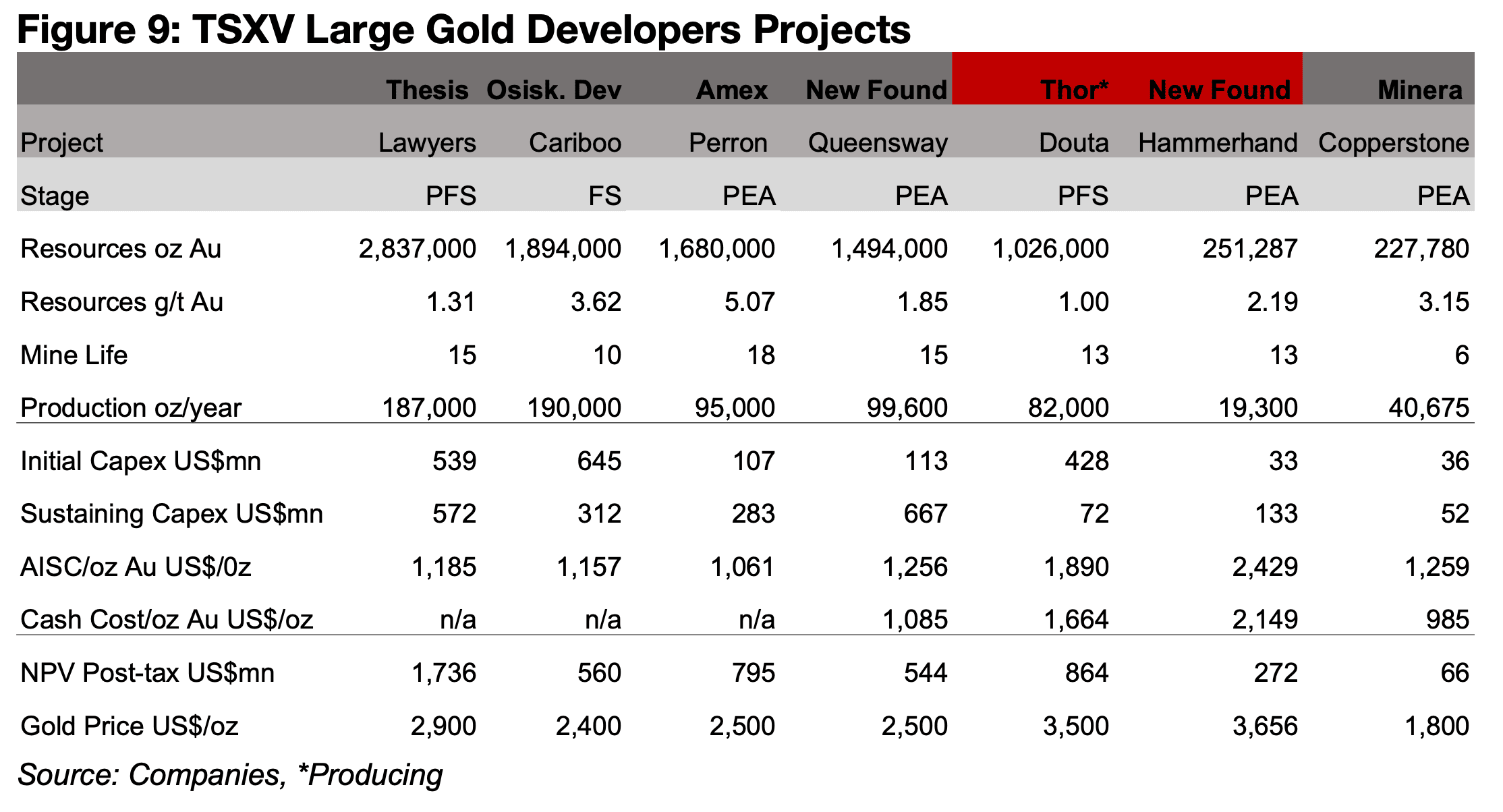

This week we look at the larger TSXV gold developers, which have overall seen major share price gains over the past year and made substantial advancements of their respective main projects, with the market expecting strong upside to target prices.

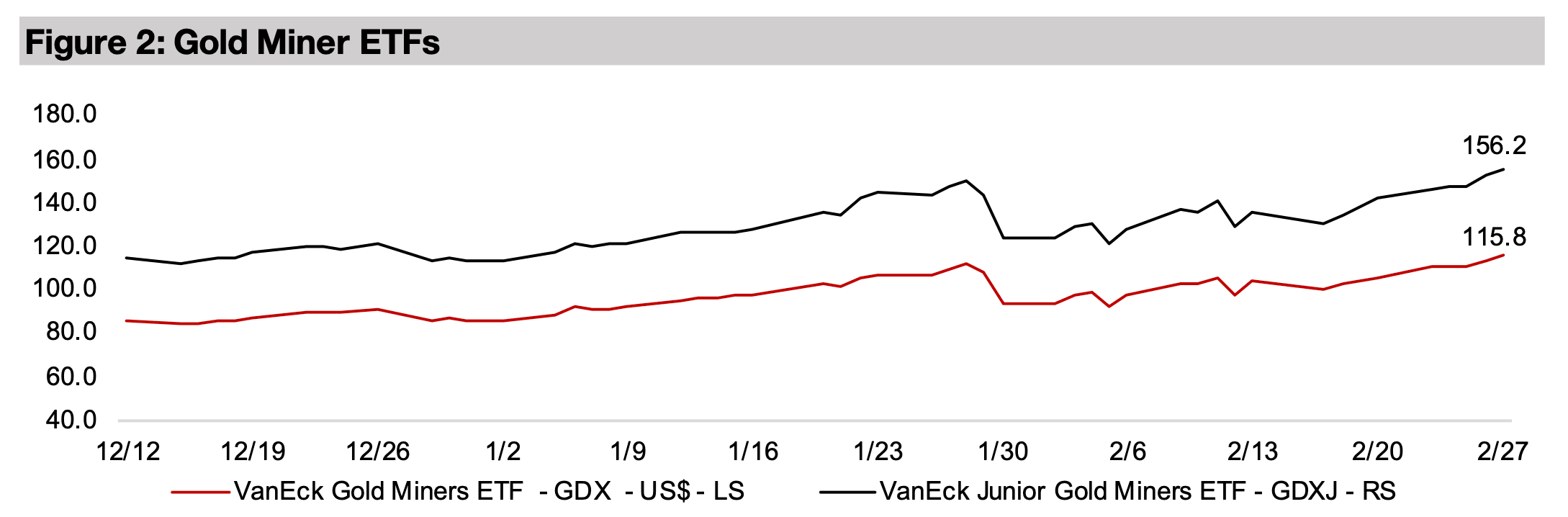

The gold stocks reached new highs, with the GDX up 9.0% and the GDXJ gaining 10%, outperforming flat broader equity markets, with the S&P 500 down -0.3%, although tech and small caps were weak with the Nasdaq and Russell down -0.8%.

The gold price rose 3.3% to US$5,248/oz, with key economic news including US

wholesale price inflation coming in above expectations. This did not move the

broader equity markets much, with the S&P 500 down -0.3%, although the Nasdaq

dropped off -0.8% on a continued sell off in tech and the Russell 2000 was also down

-0.8% on moderate risk off sentiment. The gold stocks jumped on the gain in the gold

price, with the GDX up 9.0% and GDXJ rising 10.0%.

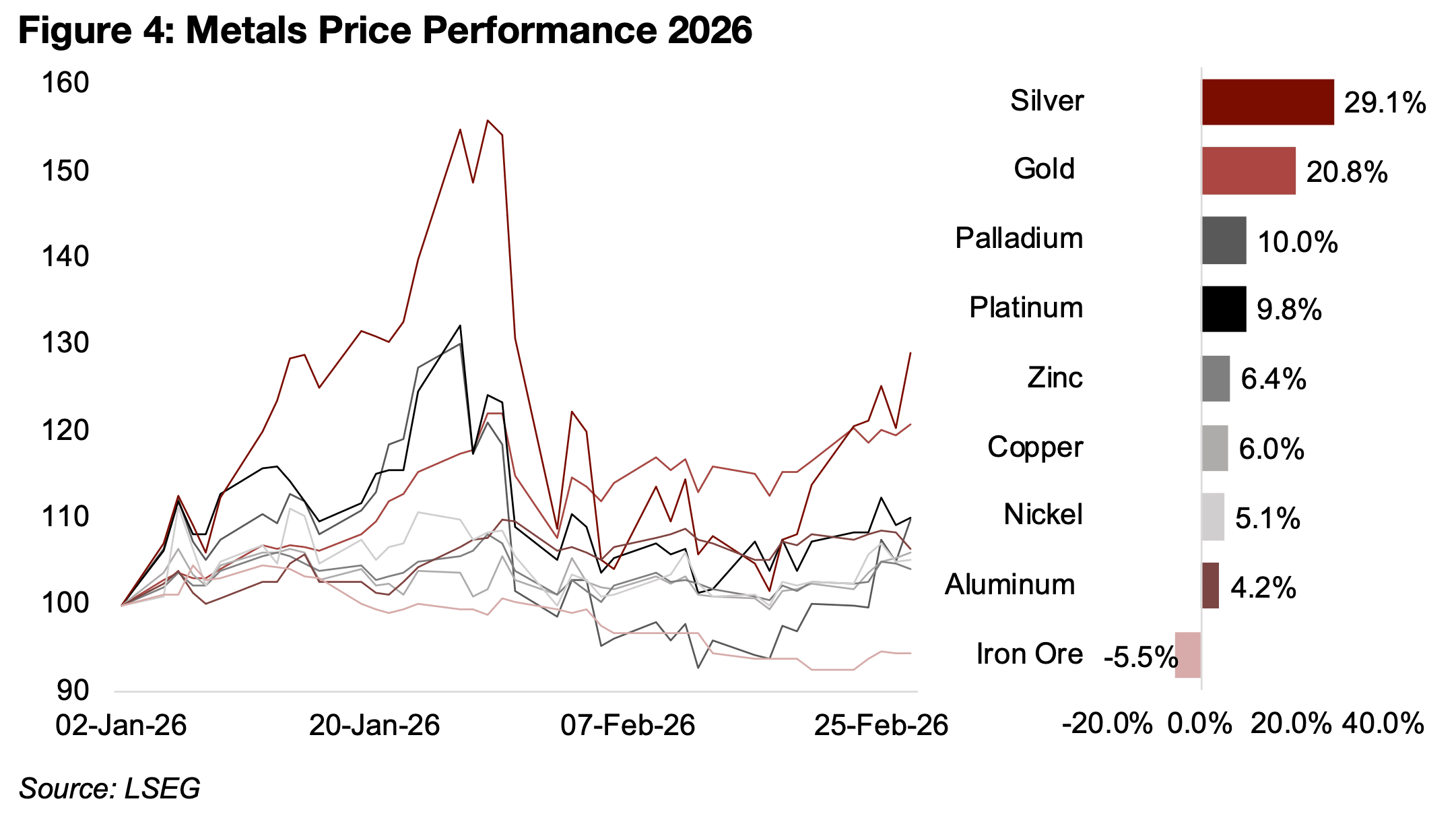

For 2026 so far, the precious metals have continued to lead the market, with silver

still seeing the biggest gains of 29.1%. However, this is far off its peak in late January,

2026, and silver is now only moderately above gold, which is up 20.8%, around

doubling the gains of palladium, at 10.0%, and platinum, at 9.8% (Figure 4). The base

metals have continued to underperform the precious metals, with most up by similar

amounts, with zinc, copper, nickel and aluminum rising 6.4%, 6.0%, 5.1% and 4.2%,

respectively, with only iron ore down, by -5.5%.

However, there was much more major news than over the weekend, with a huge

eruption in geopolitical risk as the US and Israel bombed of Iran and the latter made

retaliatory attacks in the Middle East and other countries. The gold price has since

jumped back to its previous highs of around US$5,400/oz. It seems likely that

heightened geopolitical risk will continue for an extended period and could cause

significantly volatility in many commodities prices, including the metals. The conflict

is expected to especially drive up oil prices given the closure of key shipping routes.

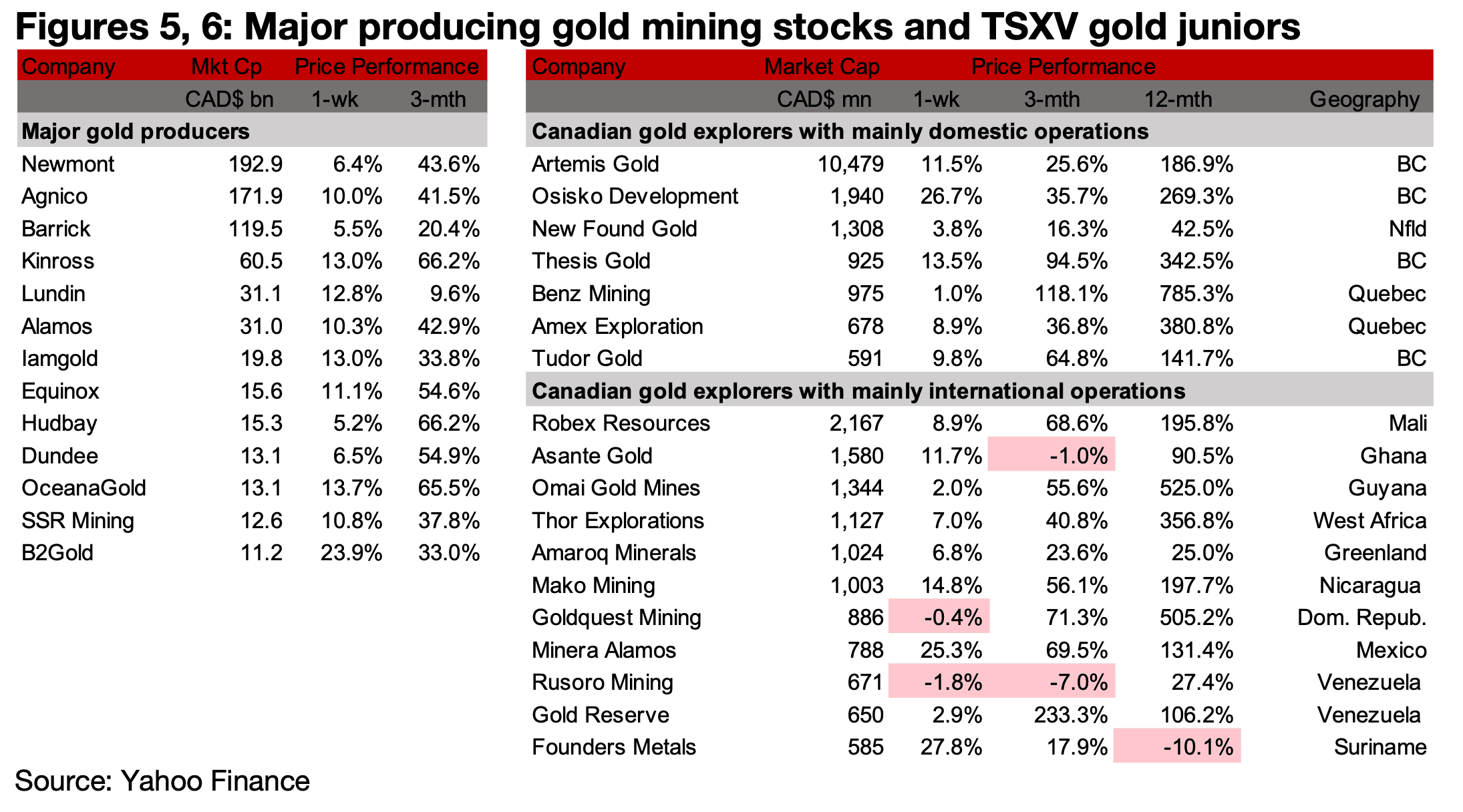

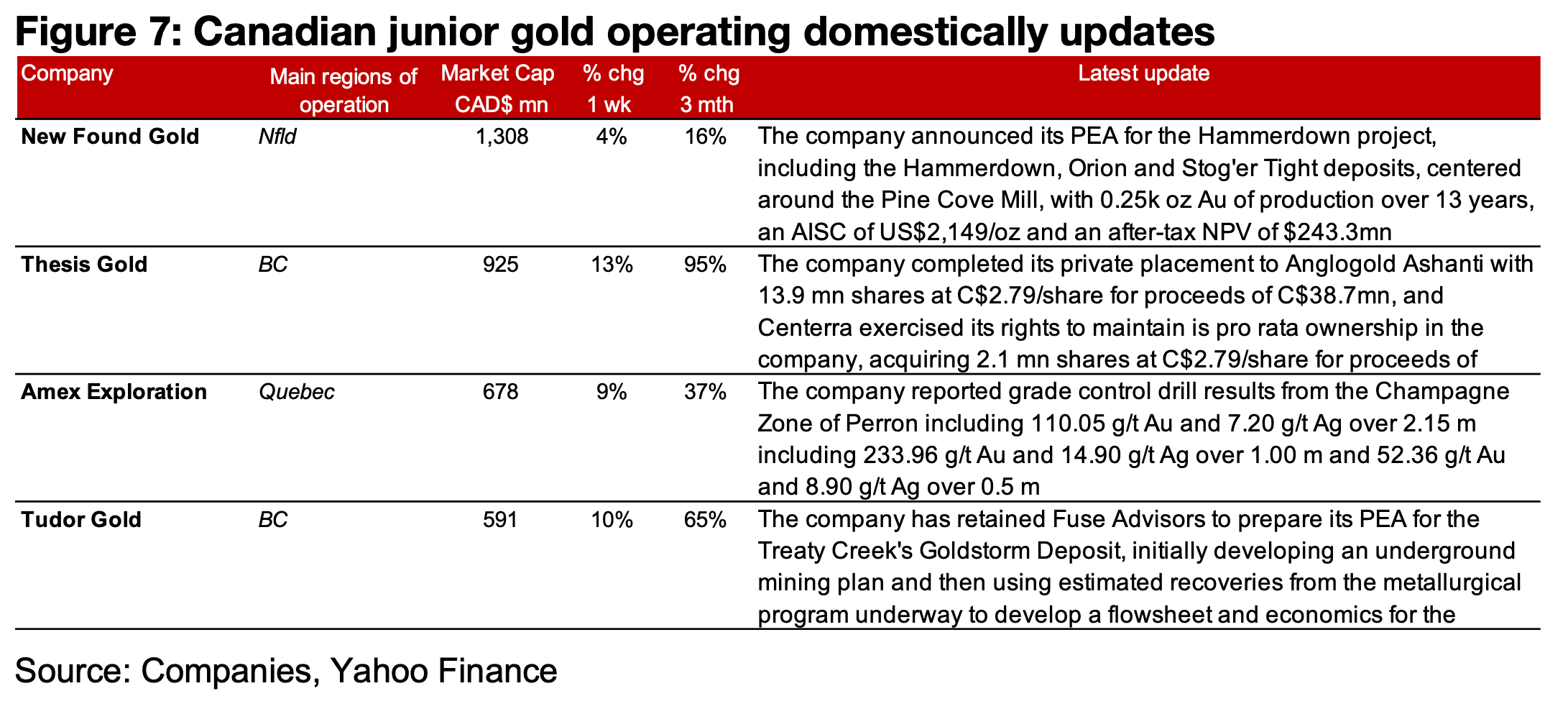

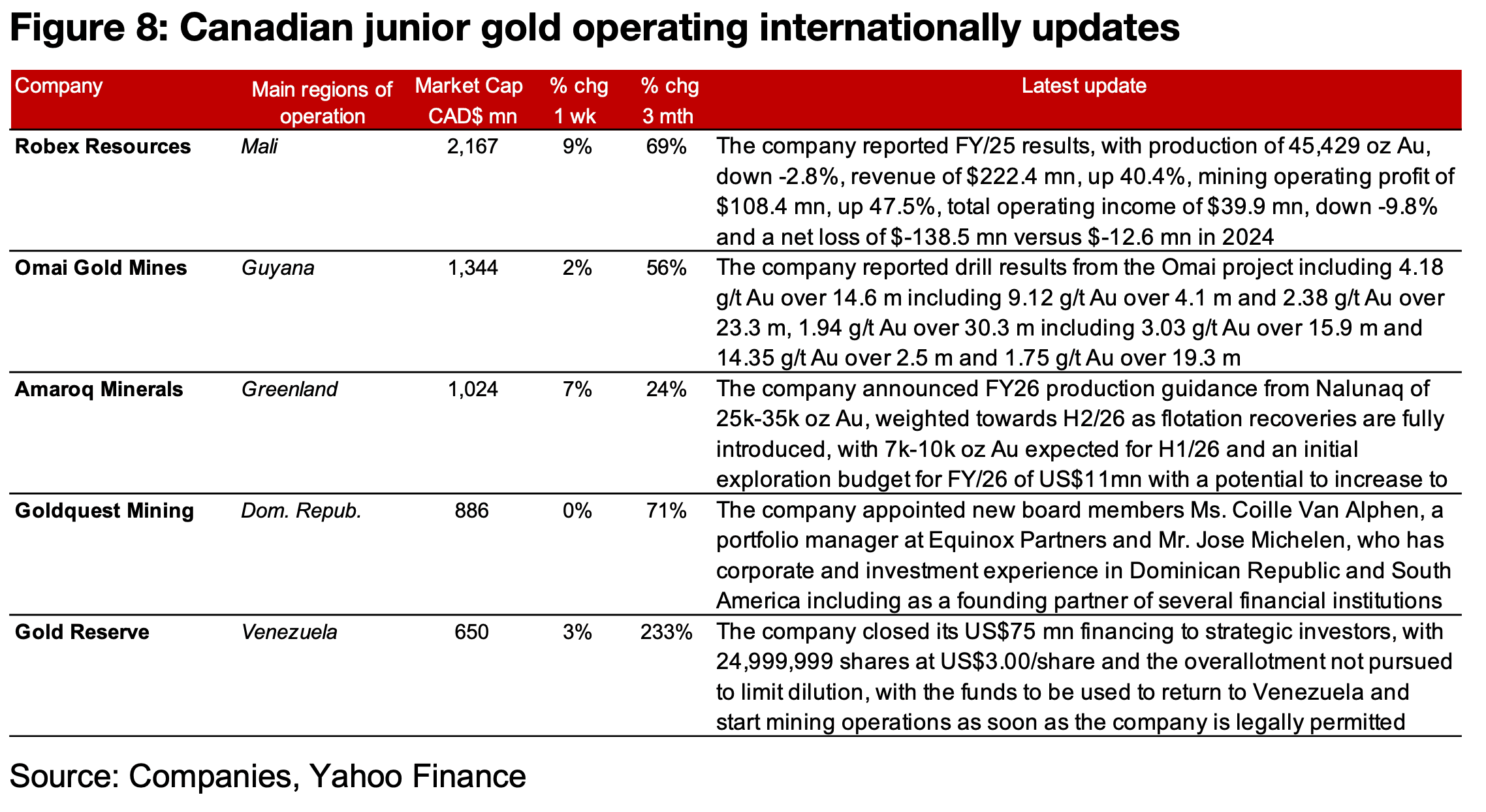

All of the major producers and most of TSXV gold saw strong gains on the rebound in the gold price (Figures 5, 6). For the TSXV gold companies operating mainly domestically, New Found Gold announced a PEA for Hammerdown, Thesis completed its placement to Anglogold Ashanti and Centerra purchased shares to maintain its holding, Amex reported drill results from Champagne at Perron and Tudor Gold announced that Fuse Advisors had been retained to prepare the PEA for Treaty Creek (Figure 7). For the TSXV gold companies operating mainly internationally, Robex reported FY/25 results, Omai reported drill results from Omai, Amaroq announced its FY/26 production guidance and exploration budget, Goldquest made appointments to its Board and Gold Reserve closed its financing (Figure 8).

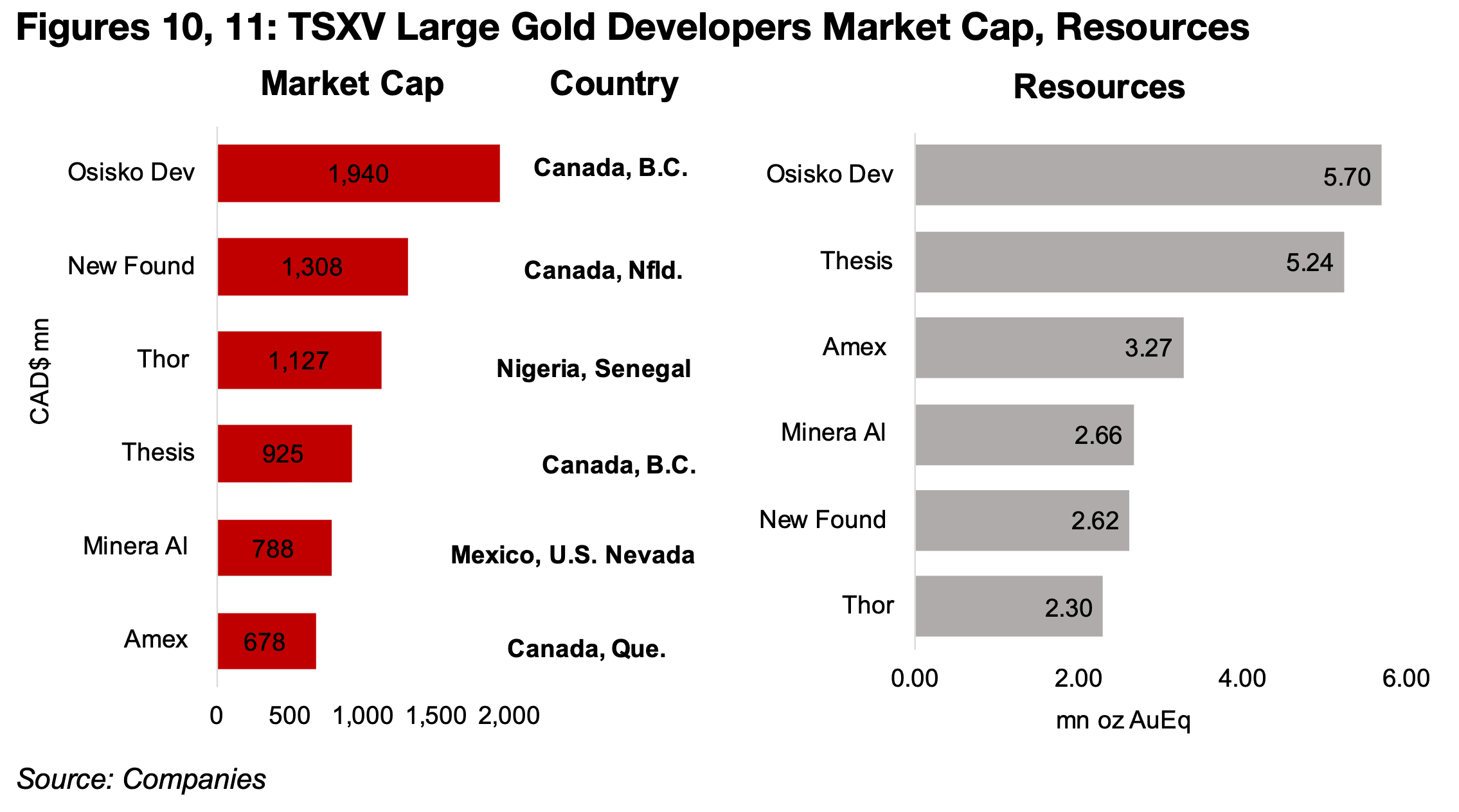

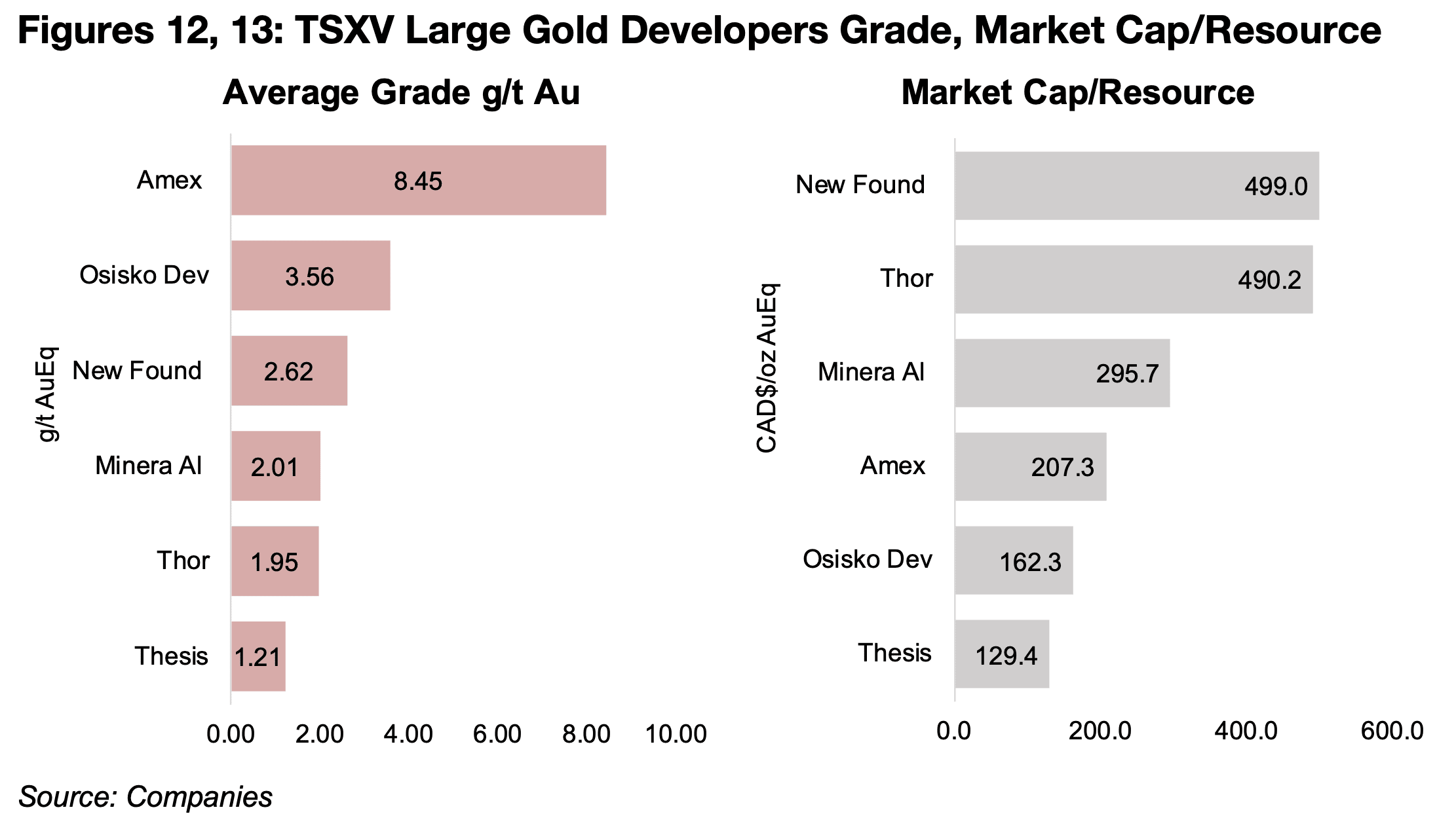

New Found Gold’s Hammerdown at only 0.25 mn oz Au is considerably smaller than its Queensway project, at 1.49 mn oz Au, and its average cost per ounce is about double, with an AISC of US$2,429/oz versus US$1,256/oz for Queensway (Figure 9). The after-tax NPVs of US$543mn for Queensway and US$272mn are also not entirely comparable, given far different gold price assumptions, with US$2,500/oz for the former, and US$3,656/oz for the latter. The company has the second highest market cap of the large TSXV developers, at US$1.3bn, with total resources at 2.62 mn oz Au, at a reasonably high grade of 2.62 g/t Au (Figures 10, 11, 12).

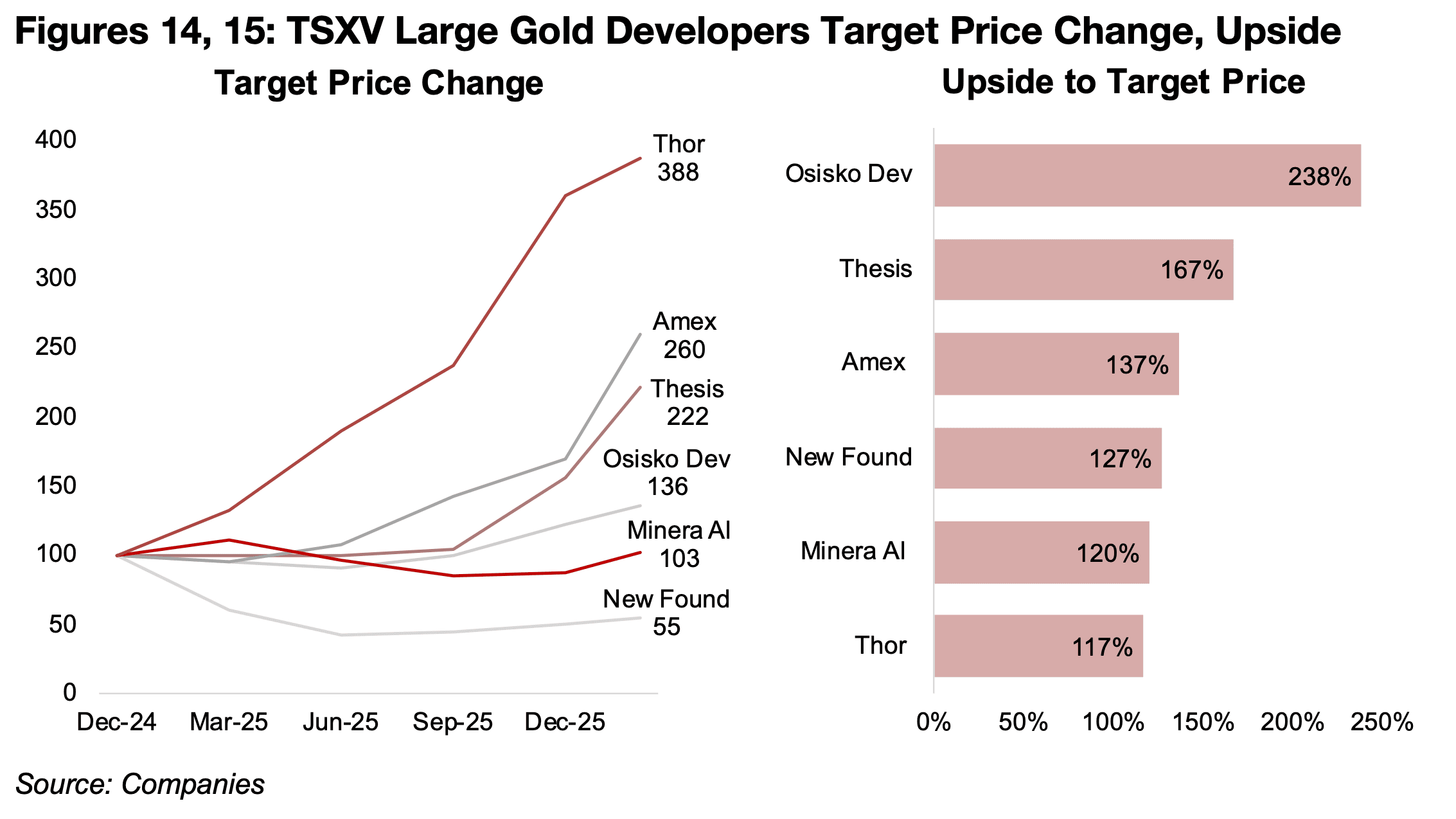

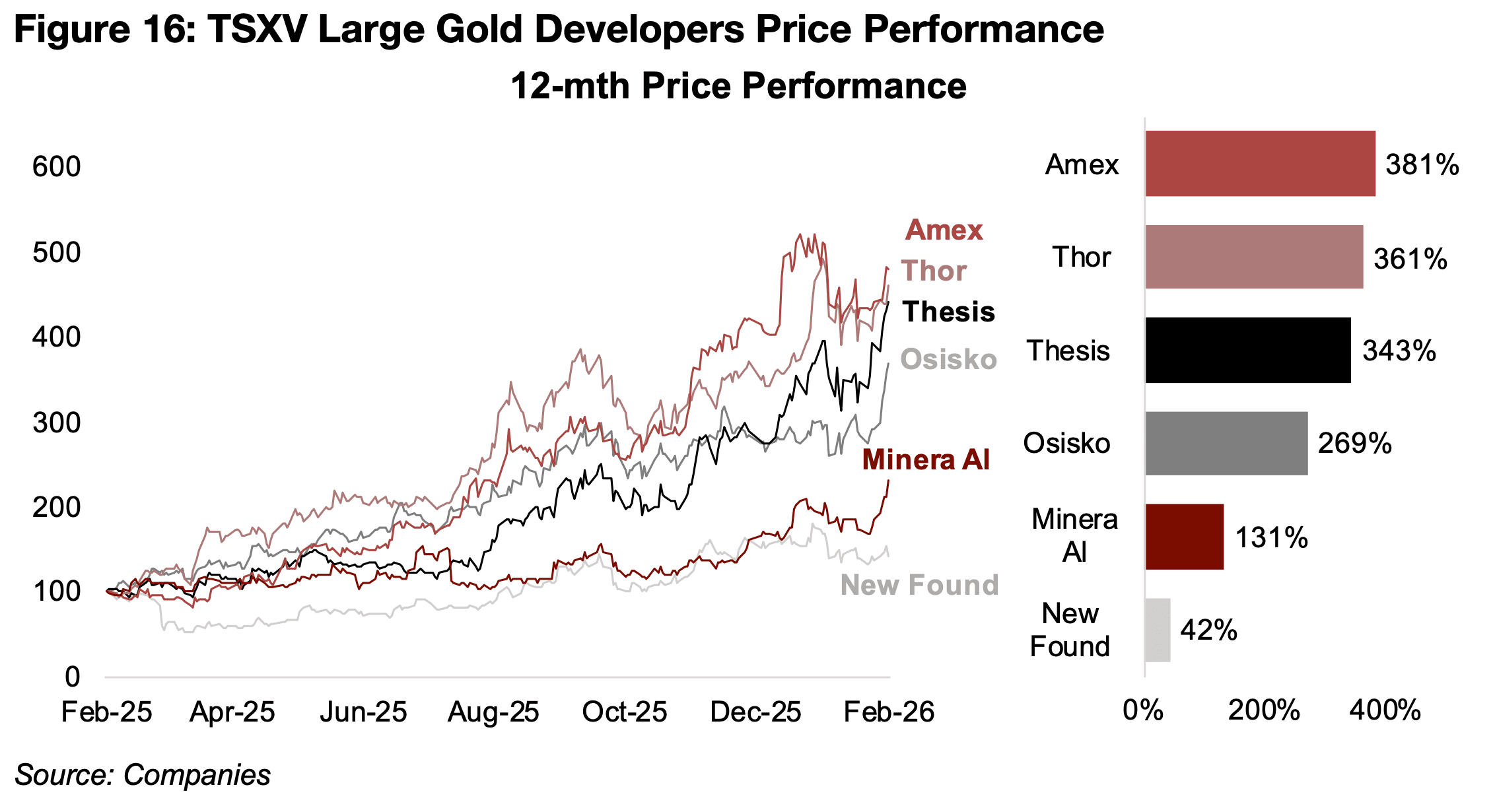

The market is paying the highest of the group for New Found Gold on a Market Cap/Resource at CAD$499.0/oz, which comes after a significant decline in the company’s price after the March 2025 announcement of its resource estimate for Queensway, which appeared to have significantly disappointed the market (Figure 13). This saw the company’s target price downgraded over the past year, with it at about half of its level at the end of 2024 (Figure 14). However, the market still sees substantial upside to the target price of 127%, around the middle of the TSXV larger gold developers (Figure 15). The company has rebounded from the slide earlier in 2025, and is still up 42% over the past month, also this lags the rest of the group significantly, with the rest all up well over 100%.

While Thor Explorations is producing at its Segilola mine in Nigeria, we have included it in Figure 8 as Douta in Senegal is one of the major development projects of the larger TSXV gold companies, and its PFS was released relatively recently, at the end of January 2026. With 1.0mn oz Au of expected total production, or 82k oz over 13 years, it is expected to replace Segilola, which had production of 92k oz Au in 2025 and is forecast to be depleted by early 2027, and maintaining or expanding its US$1.1bn market cap will rely on Douta being inline with forecasts. Thor’s total resources are relatively small versus the large TSXV developers, with 2.30 mn oz Au, and its overall grade is 1.95 g/t Au, with Douta having a much lower average grade at 1.3 g/t Au than Segilola at 4.2 g/t Au. The market is paying a relatively high Market Cap/Resource for the company, at CAD$490.2/oz, and it has seen by far the largest target price upgrade over the past year given the advancement of Douta. It has had one of the highest share price increases of the TSXV larger gold companies, up 361% over the past twelve months, and has 117% upside to its consensus target price.

Osisko Development has become the largest market cap TSXV gold developer, at

CAD$1.9bn, as it advances both its flagship Cariboo project in British Columbia and

the Tintic Project, which holds the Trixie Mine, in Utah. The Cariboo project will be the

main driver for Osisko Development long-term, with 1.9mn oz Au of production

forecast over 10 years, expected to start by 2027, although the total resources of the

project are expected to be over twice this level, at 5.5mn oz Au. While Trixie, which is

currently being operated at a test mine, has relatively low resources, at just 0.15 mn

oz, they are extremely high grade, with M&I resources of 0.10mn at 19.11 g/t Au and

Inferred Resources of 0.04mn at 7.8 g/t Au.

Cariboo also has a relatively high grade with its Probable Resources of 2.0 mn oz Au

at 3.62 g/t Au, M&I Resources of 1.6 mn oz Au at 2.9 g/t Au and Inferred Resource of

1.9 mn oz At 3.09 g/t Au, for an average grade across the two projects of 3.56 g/t Au.

Although Osisko Development’s Market Cap to Resource is relatively low versus the

TSXV large developers, at CAD$162.3/oz, it has the highest upside to its target price

at 238% after only moderate upgrades to the target over the past year, and a 269%

gain in the share price over the past twelve months.

Amex is developing the reasonably large Perron project, with 1.7 mn oz Au of total

production, or 95k oz Au over 18 years, with a relatively low initial capex of US$107mn

and AISC of US$1,061/oz. The company has an ongoing grade control drill program

for its planned bulk sample of the Champagne Zone of the project, and in early

February 2026 started permitting for a power line for Perron.

The company’s market cap is the lowest of the large TSXV developers at CAD$678mn,

with a Market Cap/Resource of CAD$207.3/oz, although it has a relatively large

resource of 3.27 mn oz Au and very high grade of 8.45 g/t Au oz. The Perron project’s

grade was already relatively high at 5.07 g/t Au, and boosted by the extremely high

grade of Champagne with 0.83mn oz Au in M&I Resources at 16.2 g/t Au and 0.13

mn oz Au in Inferred Resources at 9.83 g/t Au. The company has seen the second

highest upgrade to its target price over the past year, and has 137% upside to its

target price, after the highest share price gains over the past twelve months of the

TSXV large gold developers, up 381%.

Thesis Gold & Silver, which was renamed from Thesis Gold in February 2027, has

had several major developments in advancing its Lawyers-Ranch project in British

Columbia this year, including a Pre-Feasibility Study reported in January 2026. The

project is the largest of the TSXV large gold developers, with a 2.84mn oz Au of

production, or 187k oz Au over 15 years, although the grade is relatively low at 1.31

g/t Au. The company started the environment assessment for the project near the

end of last year, and has continued to report drill results this year.

It also closed a strategic investment by Anglogold Ashanti over the past week for 5%

of the company, with Centerra also participating in a placement, exercising its rights

to maintain its 9.9% holding in the company, showing support from major gold

producers. The company’s market cap is toward the middle of the TSXV developers

at US$925 mn, and its resources the second highest, at 5.24 mn oz.

Its overall grade it the lowest of the group, at 1.21 g/t Au, which is likely partly driving

its low Market Cap/Resource versus the group at CAD$129.4/oz. Thesis has seen

substantial upgrades to its target price over the past year, has 167% upside to the

target, and its share price has risen 343% over the past twelve months.

Minera Alamos has four main projects, the Pan Mine, in Nevada, U.S., which it

acquired from Equinox Gold in October 2025, and it had its first gold pour in the same

month, Copperstone, in Arizona, at the pre-construction phase, and Gold Rock in

Nevada and Cerro de Oro in Mexico, which are both in both in development. The PEA

for the Copperstone shows the smallest project of the large TSXV gold developers,

with production of just 0.22mn oz Au, or 40.7k oz Au over six years, with a reasonably

high grade of 3.15 g/t AuEq.

Minera has the second lowest market cap of the group, at CAD$788mn, with 2.66 mn

oz Au in total resources at a moderate 2.01 g/t Au grade, with the Market

Cap/Resource reasonably high at CAD$295.7/oz. The company’s target price has

been near flat over the past year, and the market sees 120% upside to the target.

While the company has had strong gains over the past twelve months of 131%, this

is relatively low compared to the 250% or more gains for most of the TSXV large gold

developers.

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.

Author

Ben McGregor authors the Weekly Roundup at CanadianMiningReport.com, providing sharp analysis of the metals and mining sector. With a talent for spotting trends, Ben distills complex market shifts into clear, engaging insights on TSXV junior miners. His weekly updates cover gold, copper, uranium, and more, blending data-driven perspectives with a knack for identifying opportunities. A vital resource for investors, Ben’s work navigates the dynamic junior mining landscape with precision.