May 04, 2026

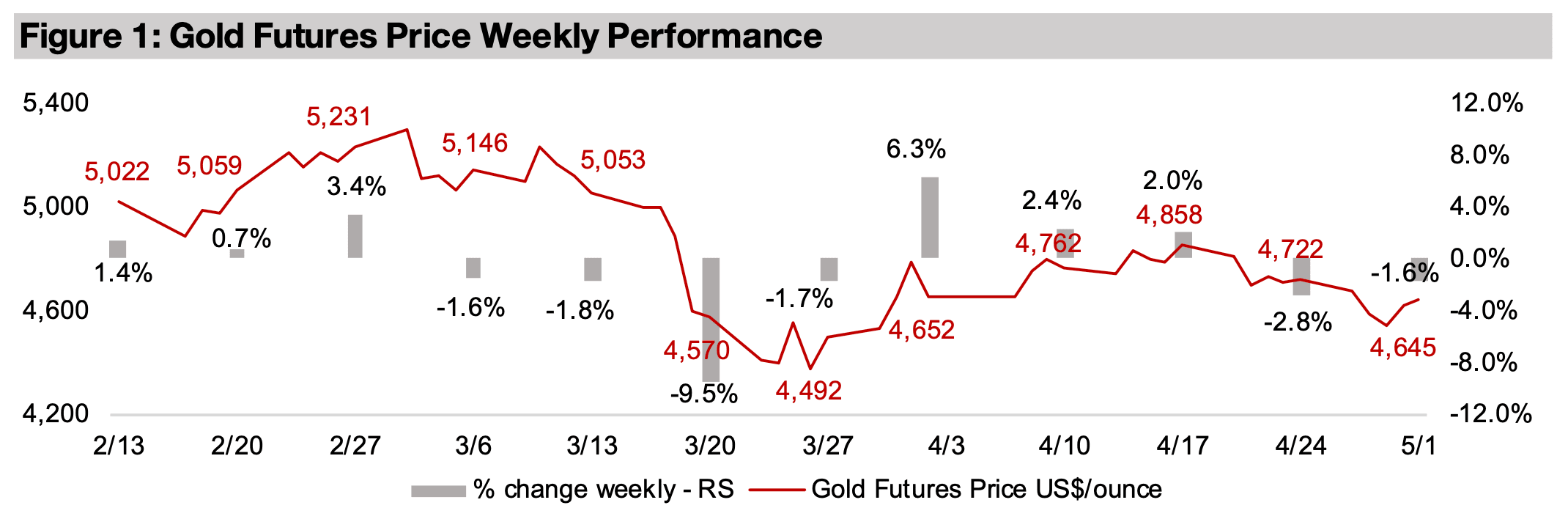

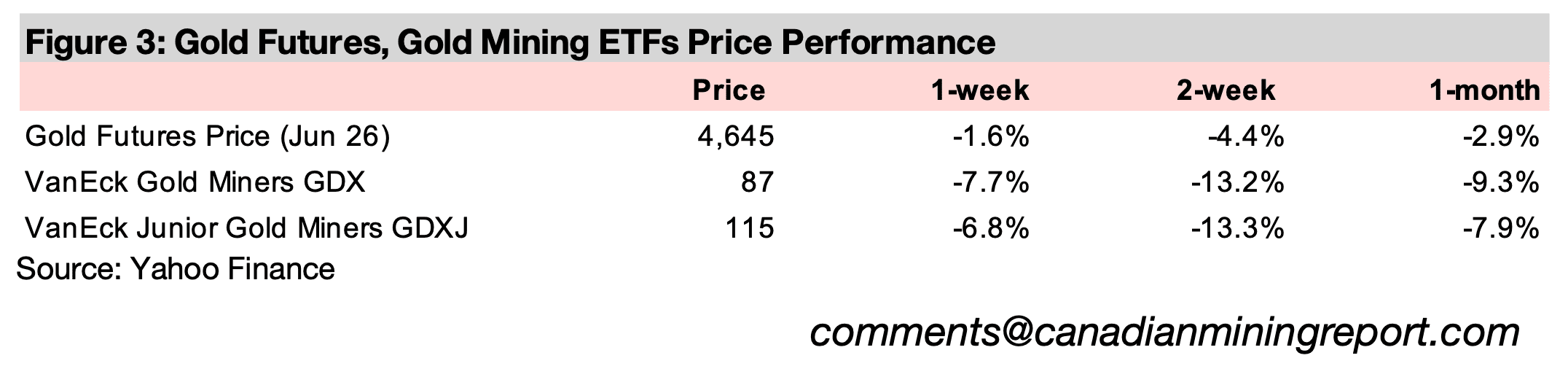

Gold declined -1.6% to US$4,645/oz, down for a second week, mainly on a continued major risk-on rally in markets which saw reduced flows into safe havens including the metal, even though risks have remained elevated on the Middle East conflict.

The strong Q1/26 results for the large gold companies continued with Agnico, Kinross and Alamos reporting and seeing revenue surge as the realized gold price offset a decline in production and rising costs, driving major gains in net income.

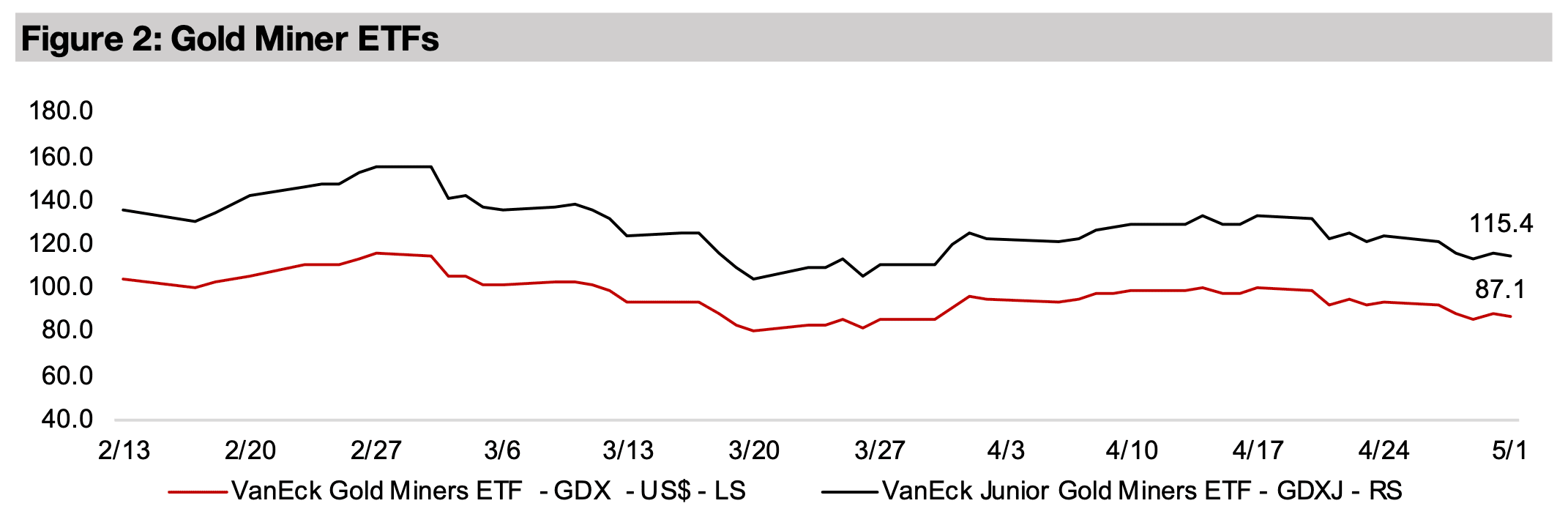

The gold stocks declined for the second week, with the GDX down -7.7% and GDXJ off -6.8% on the metal decline, underperforming global equities which continued to surge, with the S&P 500, Nasdaq and the Russell 2000 all reaching new all-time highs.

The gold price declined -1.6% to US$4,645/oz, down for the second week, which

appears mainly to have been driven by a major risk-on rally over the past two weeks,

as the effect of the US$ and bond yields were roughly balanced, with the latter rising

and the former declining. There has clearly been a shift into some of the potentially

most volatile sectors in April 2026, with US Tech, Bitcoin and China Tech up 19.8%,

15.1% and 10.3% for the month. Strong tech has once again supported the S&P 500,

which gained 10.0%, with European stocks also up, but by a more moderate 4.7%.

More defensive assets like gold and the gold stocks underperformed in April 2026,

with the metal off -3.0%, the GDX down -7.9% and GDXJ declining -9.3%, while

utilities were near flat, up 0.7%. While the oil price jumped 13% in April 2026, the

energy sector was also near flat, gaining just 0.4%, after the 9.0% rise in March 2026

on the gain in the oil price. This would seem to indicate some pressure on the

resources sector overall and yet another rotation by the markets back into tech.

However, there was still a 6.1% gain in the PICK MSCI Metals & Mining ETF, which

is driven mainly by copper, and was up 3%, and iron ore and aluminum, which were

flat, but also would have been supported by 13% and 2% gains in nickel and zinc.

This surge in the markets seems to go against clearly deteriorating global

macroeconomic fundamentals, with the geopolitical risk likely to remain high and

costs for all sectors very likely to rise as the effects of much higher oil prices move

through the supply chain. This seems to imply the markets are going through

somewhat of a mania now where prices have become increasingly disconnected from

underlying drivers. We can see evidence of this in market valuations which have

surged to near, or even above, all-time highs.

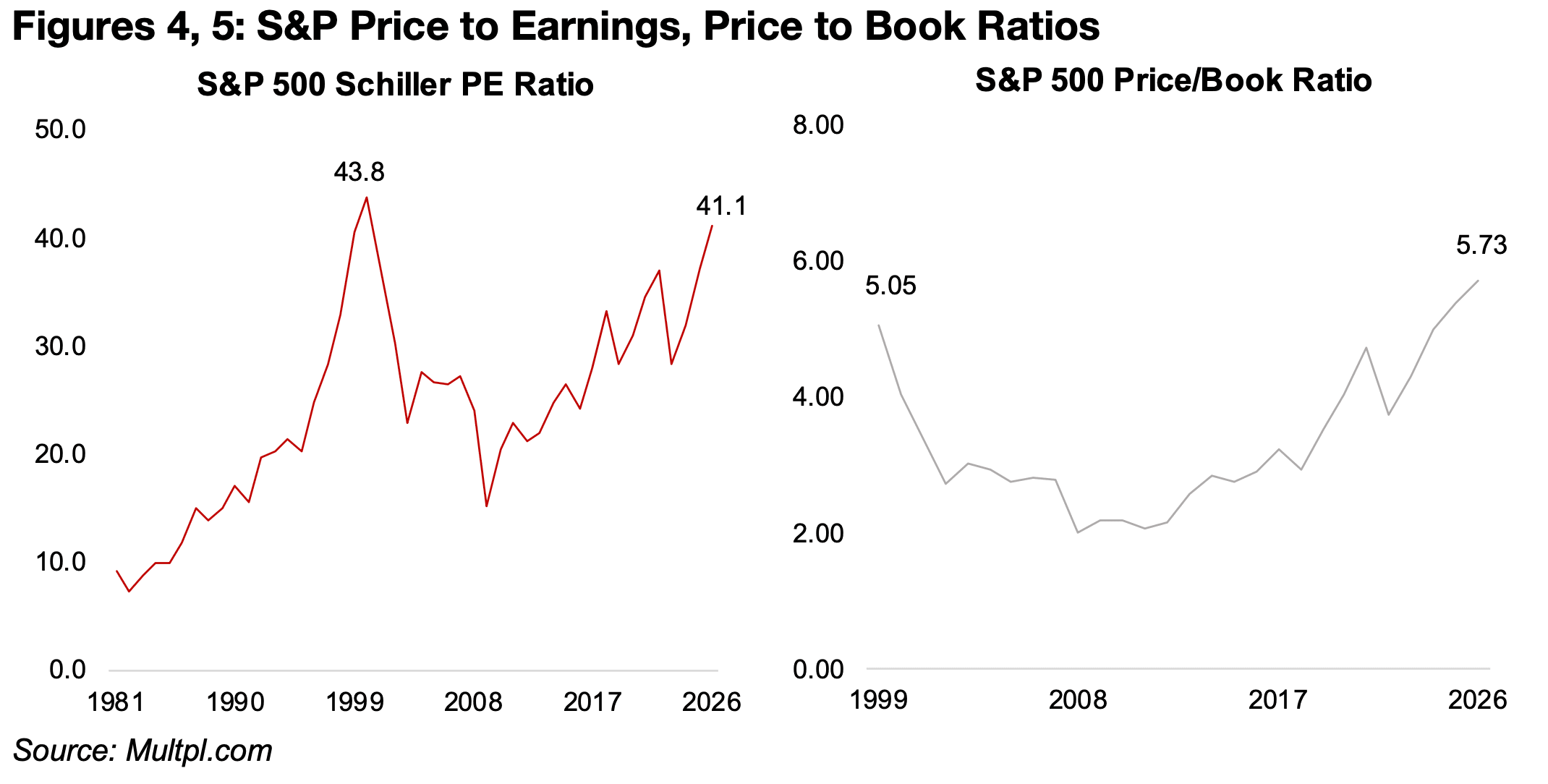

The S&P 500 Schiller PE Ratio, which takes the index price versus the 10-year

inflation adjusted earnings, has reached 41.1x, surpassed only in 2000 at 43.8x in the

dot-com boom (Figure 4). The S&P price to book ratio at 5.73x is at its highest level

ever, even above the 5.05x reached in the dot.com boom (Figure 5). While valuations

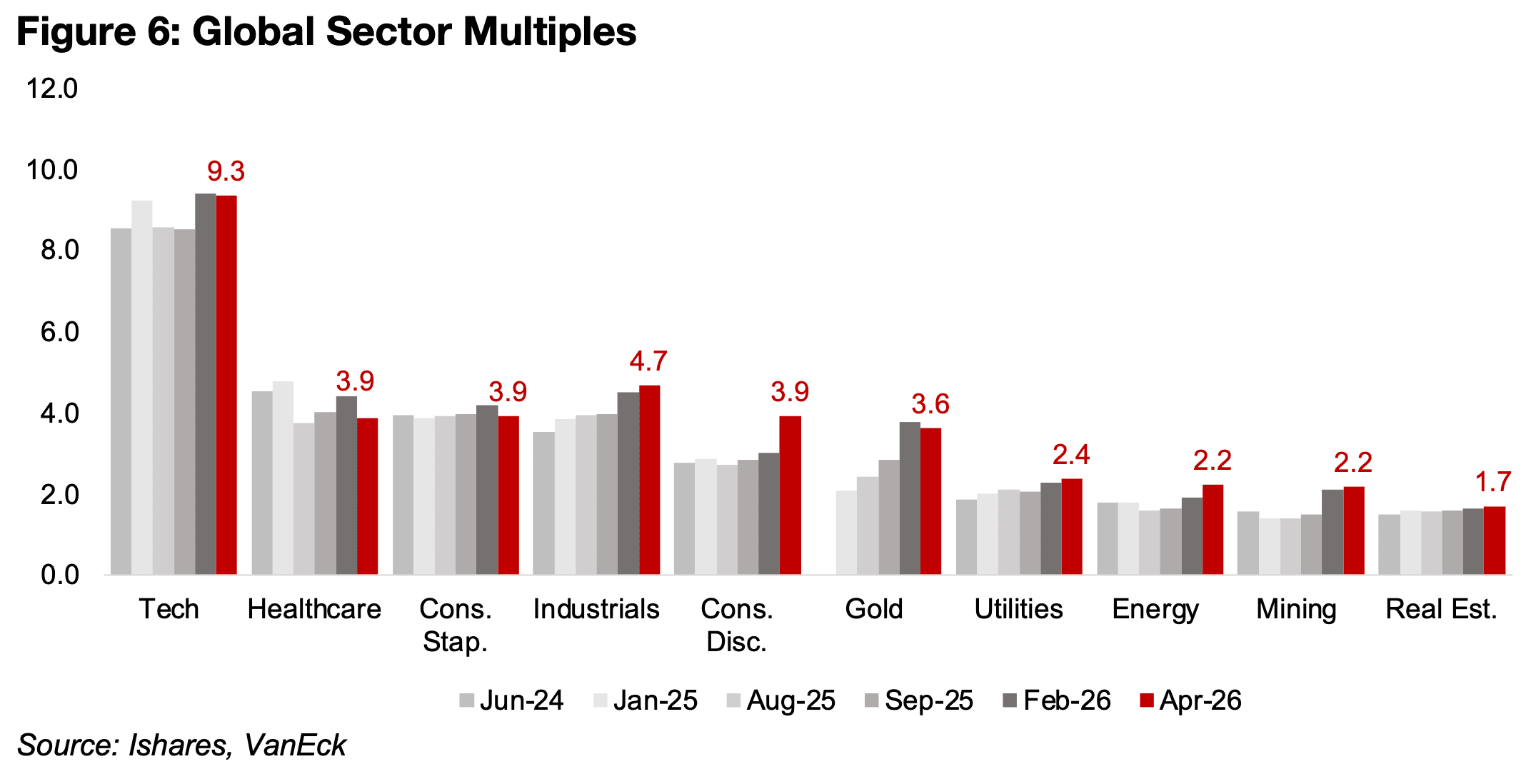

have been rising in other sectors, tech is still double the multiple of other sectors, and

the global market cap remains heavily concentrated in this sector (Figure 6). This

major reliance on tech to support markets has looked increasingly risky as it has been

driven by the AI boom, especially from huge investment in data centers. The

sustainability of AI-related spending as well the profitability of the sector, if it is not

backed by continued huge capital expenditure, has been increasingly questioned. If

this sector slumps, it could drag down the markets overall given its very high

weighting and valuations.

This could also hit some metals, especially copper, which has seen a significant lift

from the data center expansion. However, we expect that this type of decline in

markets would actually support the gold price, as it could drive down global demand,

and cause central banks to shift back into a monetary expansion. While there could

be a worst-case scenario for central banks of stagflation, where inflation remains high

even as growth declines, making it difficult from them to hike rates, gold has

historically tended to do well in this situation as a hedge against rising prices.

However, for now the markets seems to be pricing in a very low probability of almost

any major bearish outcomes from either an extended Middle East conflict and the

resulting high oil prices, or an AI sector bust. This type of extremely bullish outlook

coupled with extreme levels of valuations has tended historically to eventually lead to

major reversals, which can drive markets back into safe haven assets, including gold.

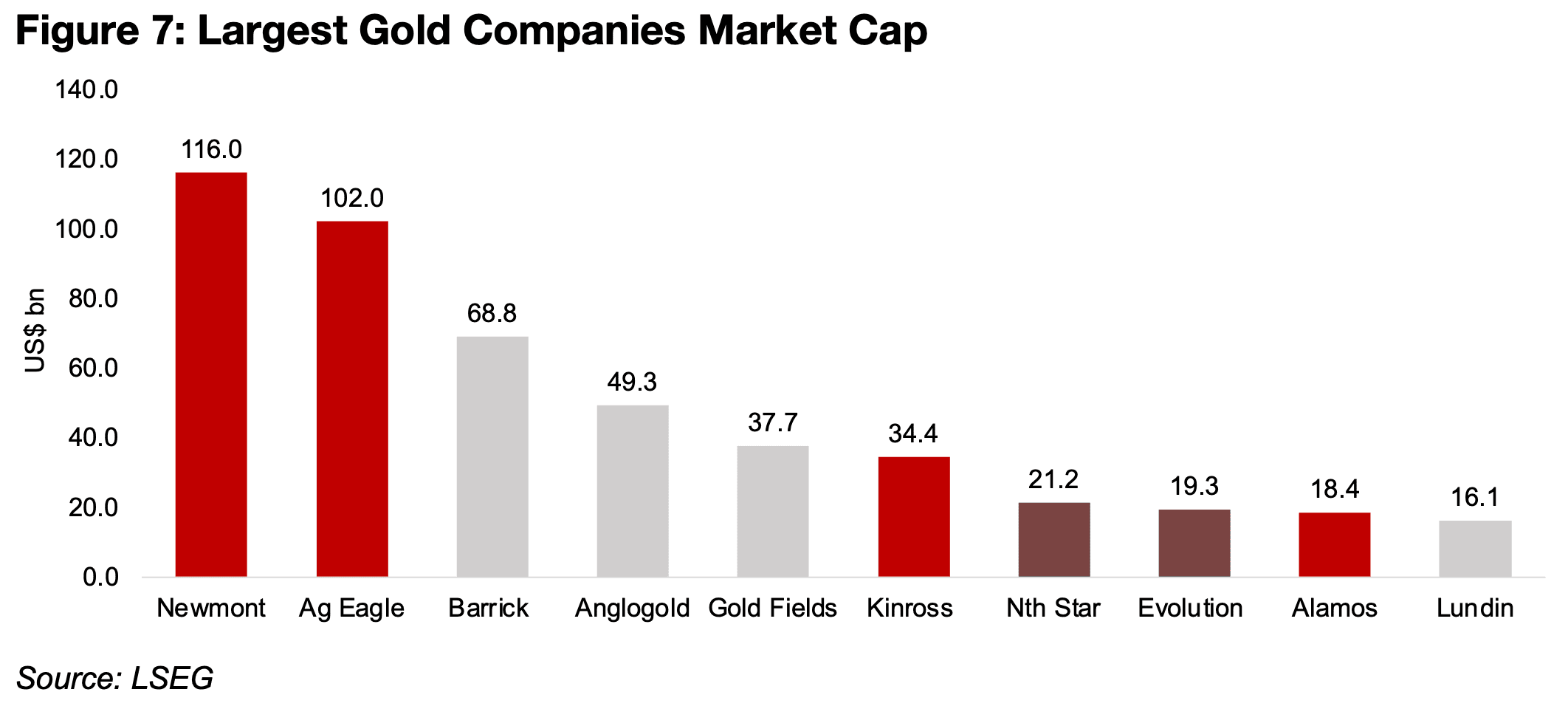

The large gold companies Q1/26 results have continued, with Agnico Eagle, Kinross and Alamos all reporting (Figure 7). This follows strong results from the largest gold company, Newmont, while Australia’s Northern Star and Evolution reported only Q1/26 operational results earlier in April 2026, as the country’s companies are only required to report for the half year. There are several majors still to release results over the next two weeks, including Barrick, Anglogold, Gold Fields and Lundin.

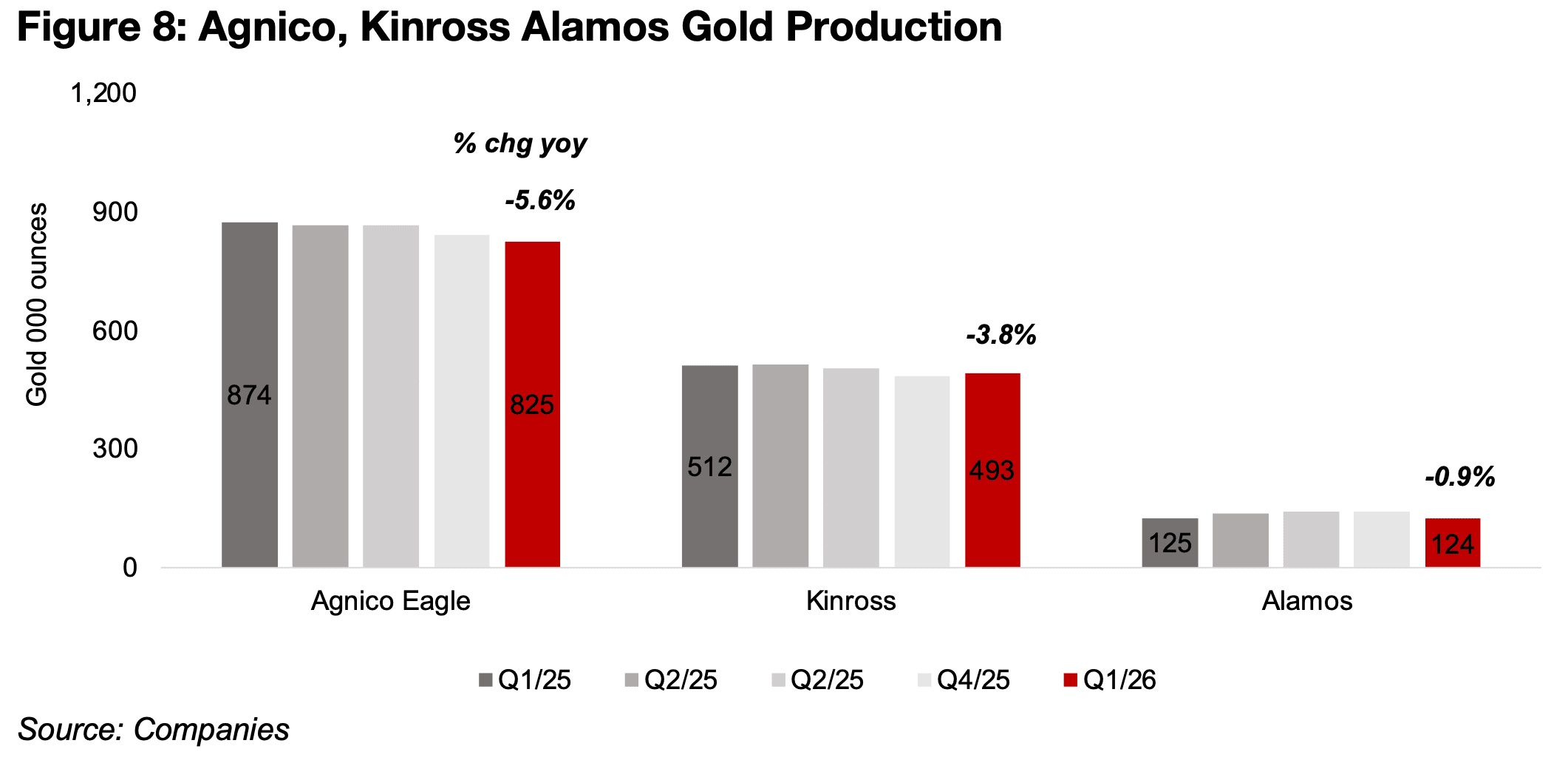

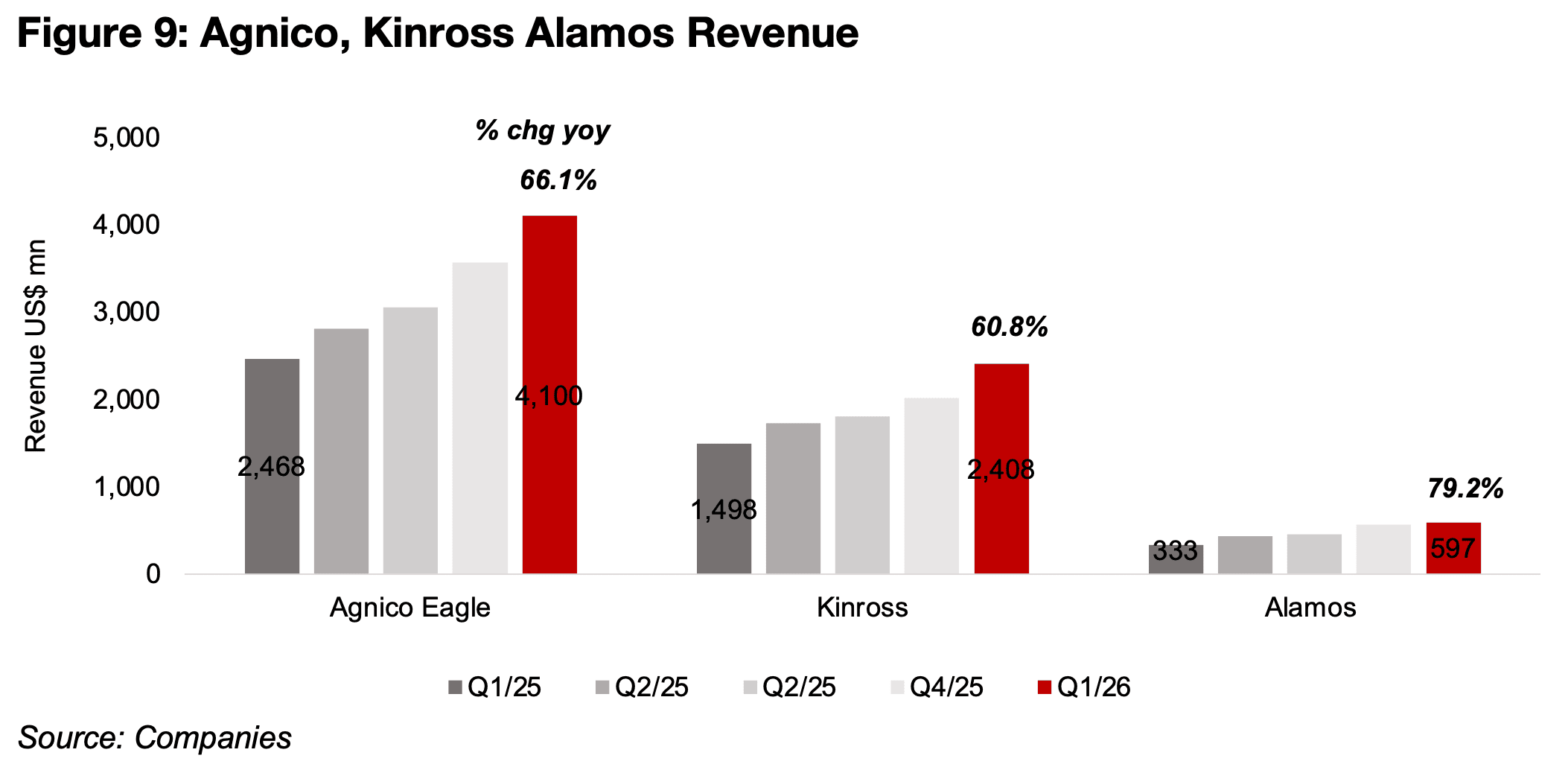

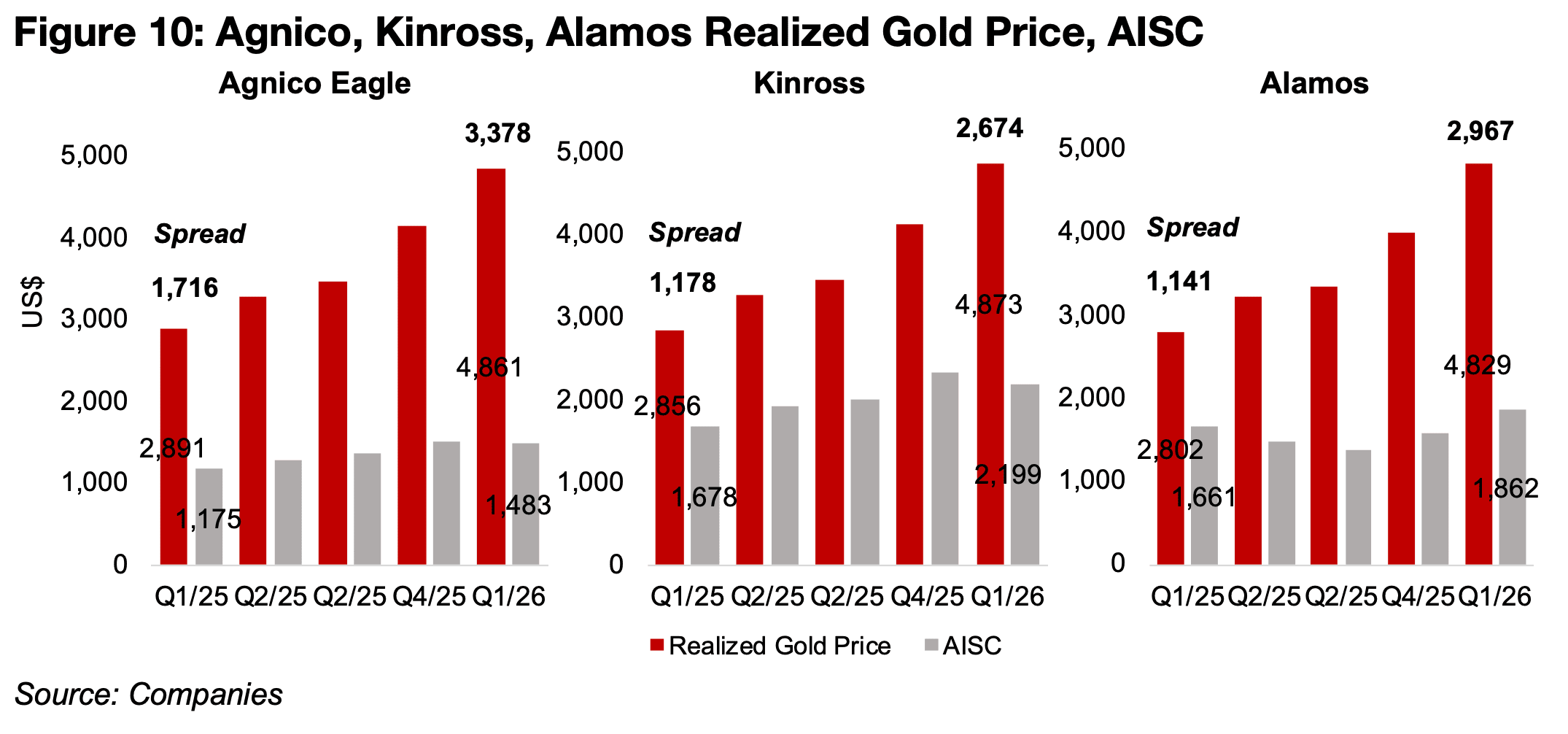

Production for all three companies declined for Q1/26 yoy, with Agnico Eagle down - 5.6% to 825k oz Au, Kinross down -3.8% to 493 oz Au and Alamos down -0.9% to 124k oz Au (Figure 8). However, revenue still jumped substantially on the rising gold price, with Agnico Eagle up 66.1% to US$4,100 mn, Kinross rising 60.8% to US$2,408mn mn, Alamos up 79.2% to US$592 mn (Figure 9).

This was driven by about a US$2,000/oz surge in the realized gold price for all three to well over US$4,800/oz in Q1/26, up from over US$2,800/oz in Q1/25 (Figure 10). While the costs of production have have actually increased substantially, they have been far outpaced by the jump in the gold price. The AISC for Agnico Eagle was up 26.2% to US$1,483/oz, for Kinross it increased 31.0% to US$2,199/oz, and there was a more muted 12.1% rise for Alamos to US$1,862/oz. This quarter saw the first effect from the higher oil price, but only in the last month of March 2026, and the full effect will start to come through in Q2/26. However, the operating spreads are so substantial for the companies at US$3,378/oz for Agnico Eagle, US$2,674/oz for Kinross, and for Alamos US$2,967/oz, that they would be able to absorb even a substantial jump in energy costs related to oil prices.

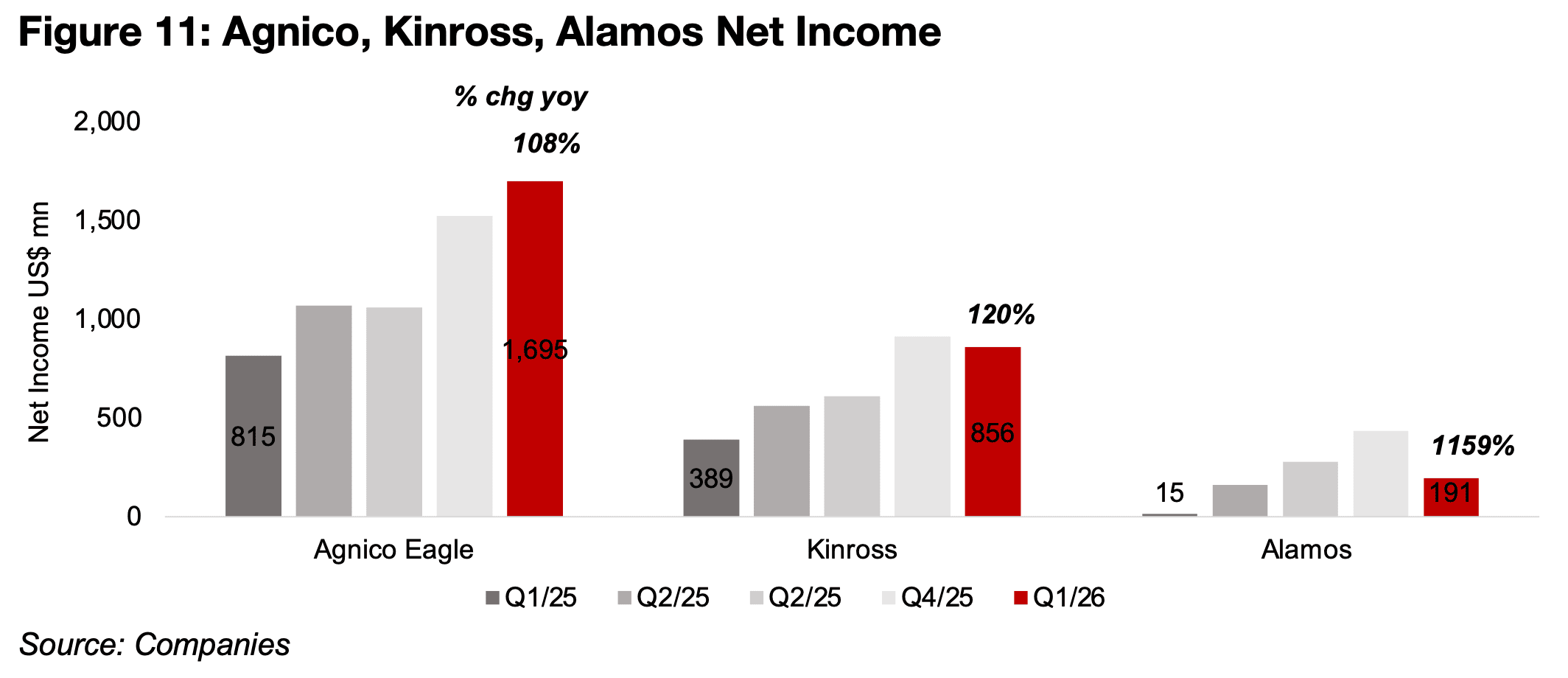

This rise in operating spread has translated to substantial net income gains for the companies, with both Agnico Eagle and Kinross up over 100% yoy in Q1/26 to US$1,695mn and US$856mn, respectively (Figure 11). Alamos had a massive percentage gain over 1,000% yoy to US$191mn in Q1/26, with Q1/25 net income low at US$15mn partly mainly on lower core operating earnings and but also from some higher extra items in the quarter.

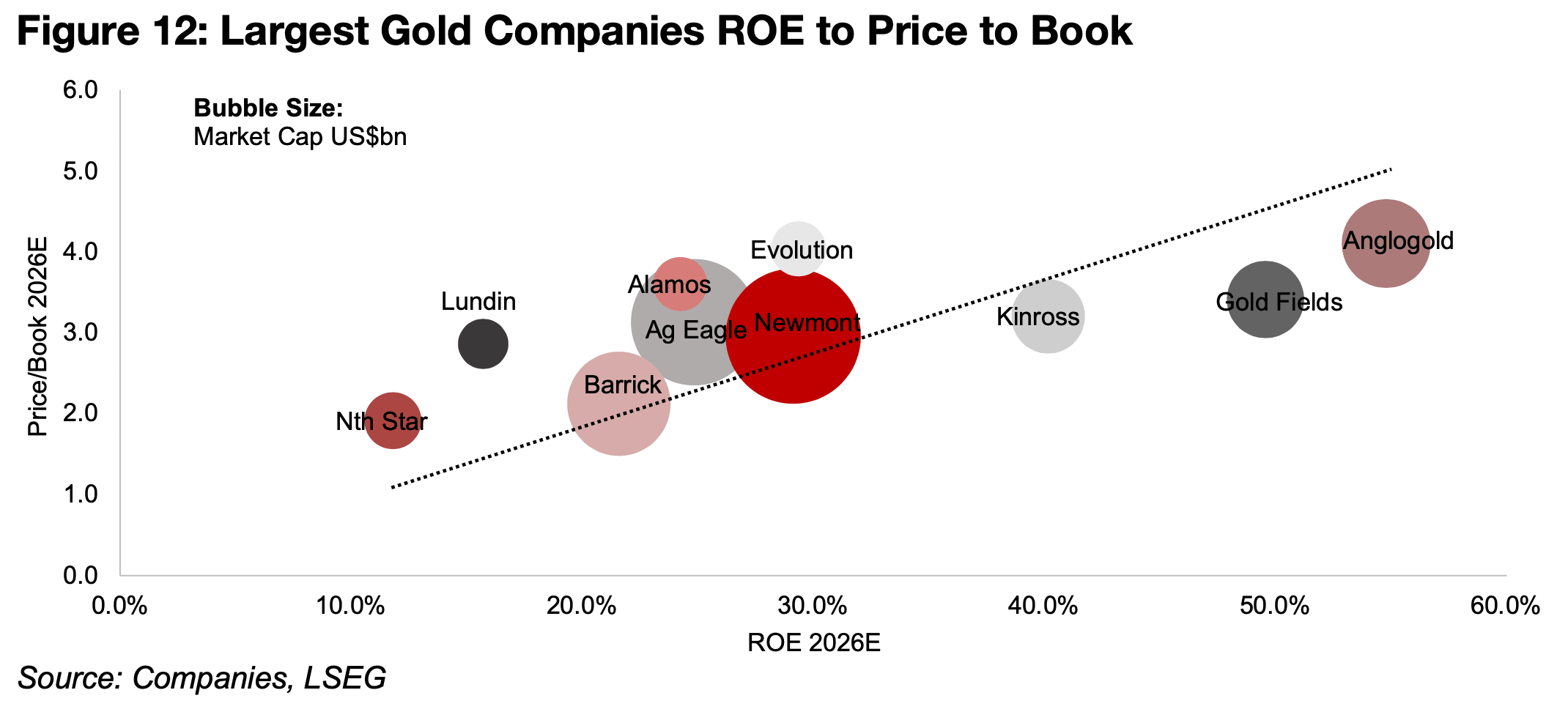

Large gold’s valuations have jumped significantly over the past year, with the price to book far above historical averages for most companies. However, this does also have strong fundamental support, as the companies have seen a major jump in returns on the surging gold price and relatively muted cost increases. Looking at price to book to ROE, the sector actually does not indicate major mispricing between the companies, with the valuation multiple generally rising with the returns (Figure 12).

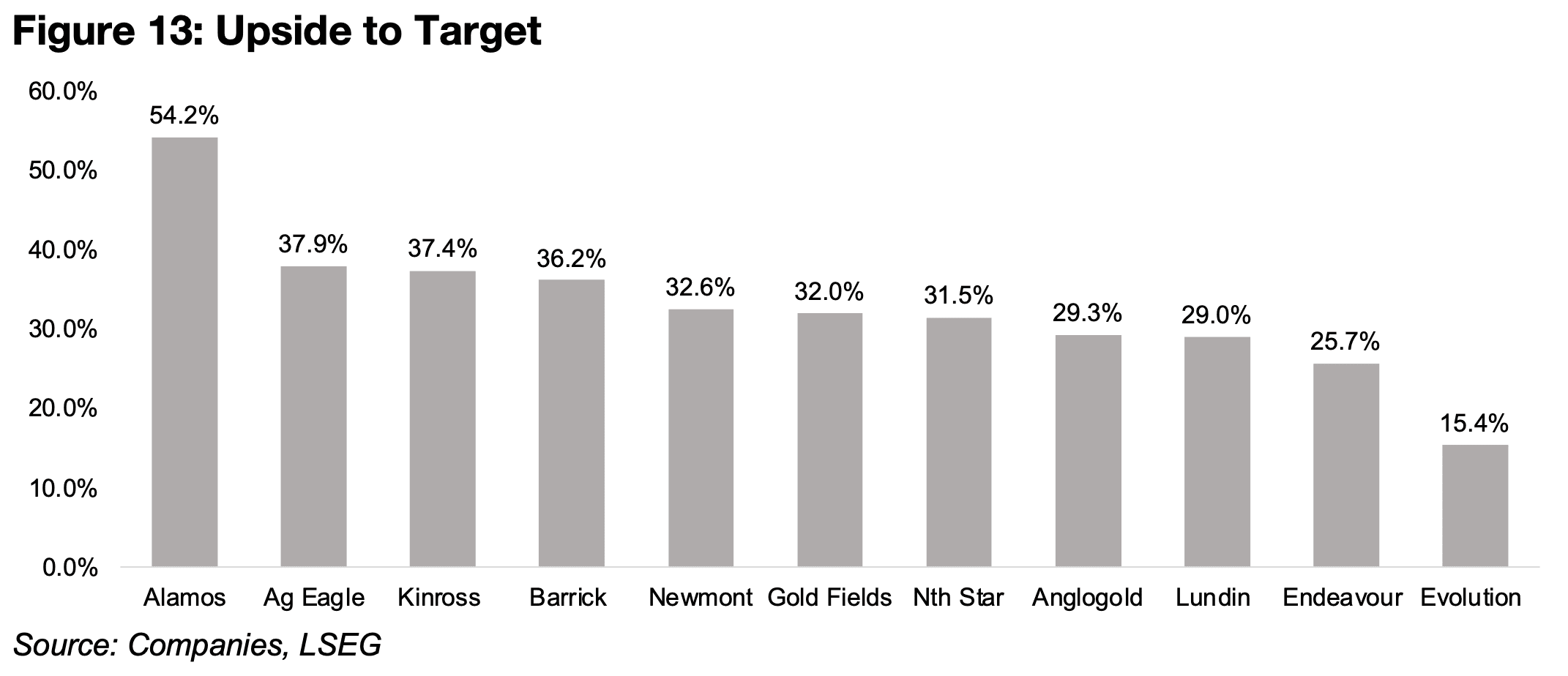

Lundin, Alamos and Evolution are somewhat above the line, and Gold Fields moderately below, but even these are not substantial outliers. The large gold companies overall have seen substantial upgrades to target prices especially starting around November 2025, which the market finally pricing assumptions for much higher gold prices for longer. This was partly driven by the surge in the sector from December 2025 to February 2026, with some analysts following the price gains with target upgrades. This had seen many of the companies actually near their target prices, but with the plunge in March 2026, they again dipped below the consensus targets. The market is now looking for around 25% to 40% upside for most of the sector, with two outliers, one high at over 50%, and one low at over 15% (Figure 13).

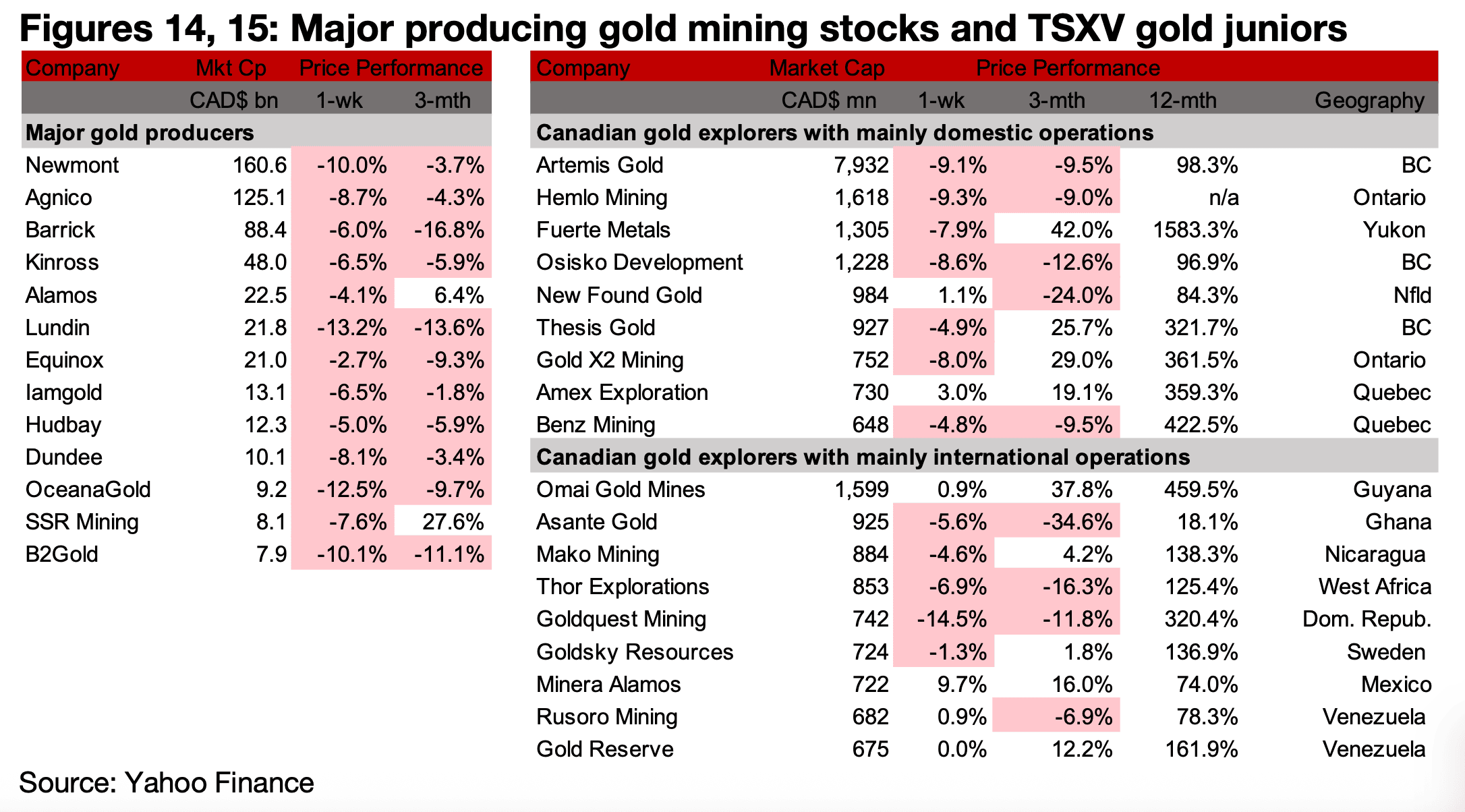

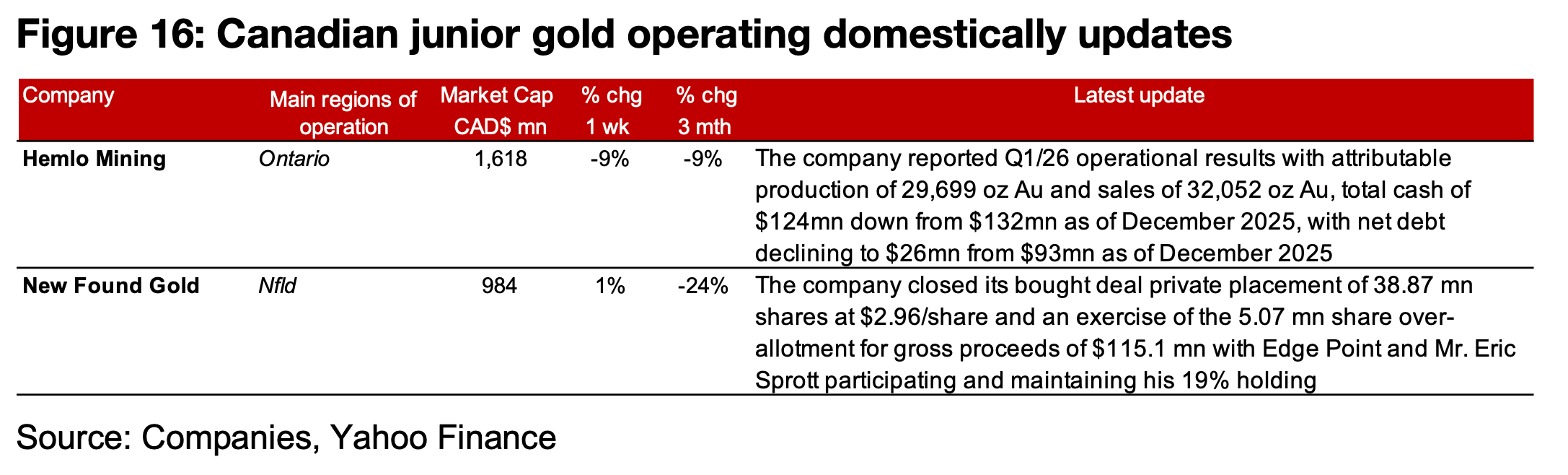

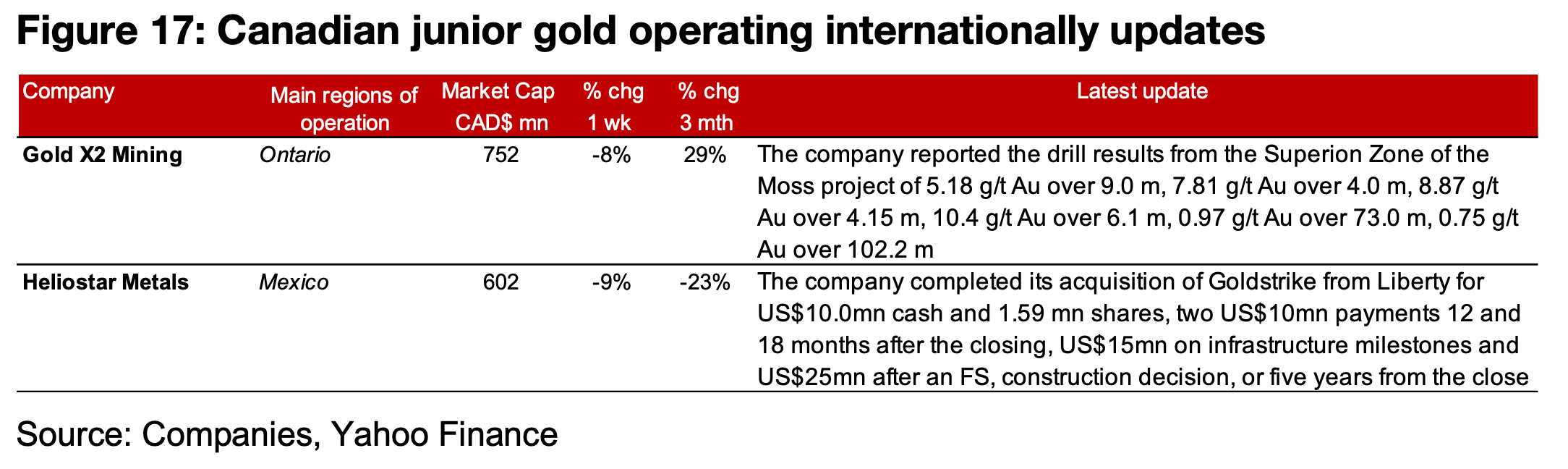

The major producers all declined substantially and most of TSXV gold were down (Figures 14, 15). For the TSXV gold companies operating mainly domestically, Hemlo reported Q1/26 operational results with 29.7k oz Au of production, 32.1k oz Au of sales and a moderate decline in cash but substantial fall in net debt from December 2025. New Found Gold closed its bought deal placement with 38.9 mn shares at $2.96/share plus an overallotment of 5.1 mn shares for gross proceeds of $115.1mn, with participation by Edgepoint and Mr. Eric Sprott, who maintained his 19% holding (Figure 16). For the TSXV gold companies operating mainly internationally, Gold X2 reported drill results from the Moss project and Heliostar completed its acquisition of Goldstrike from Liberty for US$10.0 mn in cash and 1.59 mn in shares and potentially four more payments of US$10mn, US$10mn, US$15mn and US$25mn on achieving certain operational milestones (Figure 17).

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.

Author

Ben McGregor authors the Weekly Roundup at CanadianMiningReport.com, providing sharp analysis of the metals and mining sector. With a talent for spotting trends, Ben distills complex market shifts into clear, engaging insights on TSXV junior miners. His weekly updates cover gold, copper, uranium, and more, blending data-driven perspectives with a knack for identifying opportunities. A vital resource for investors, Ben’s work navigates the dynamic junior mining landscape with precision.