May 18, 2026

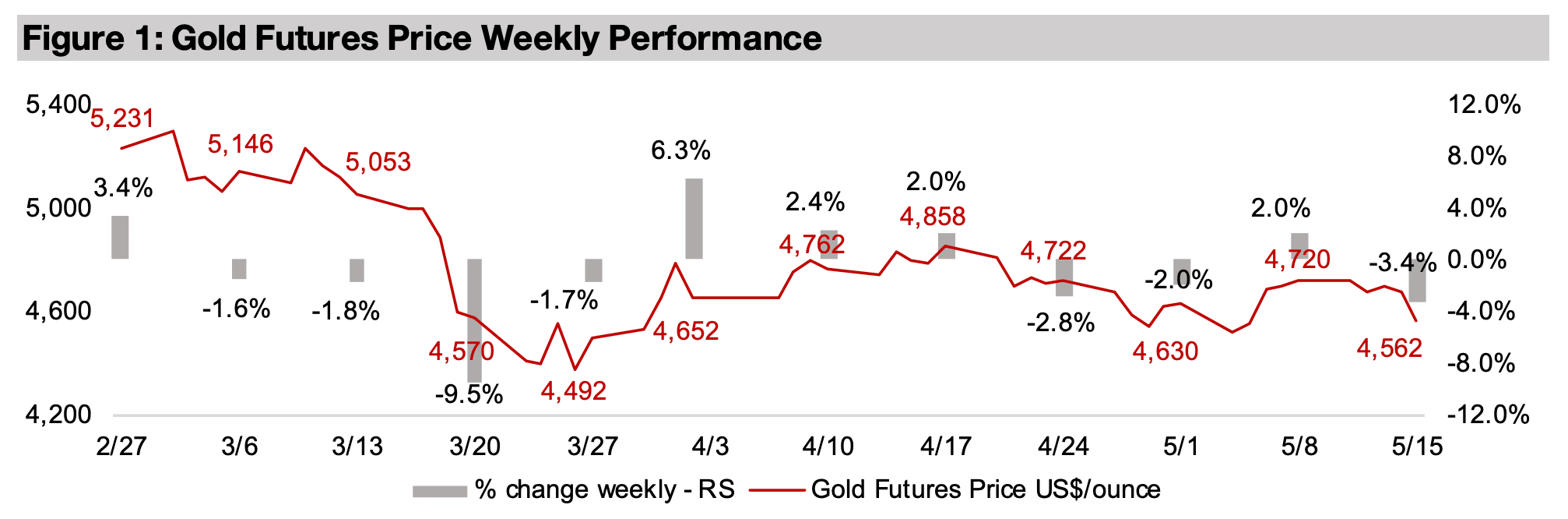

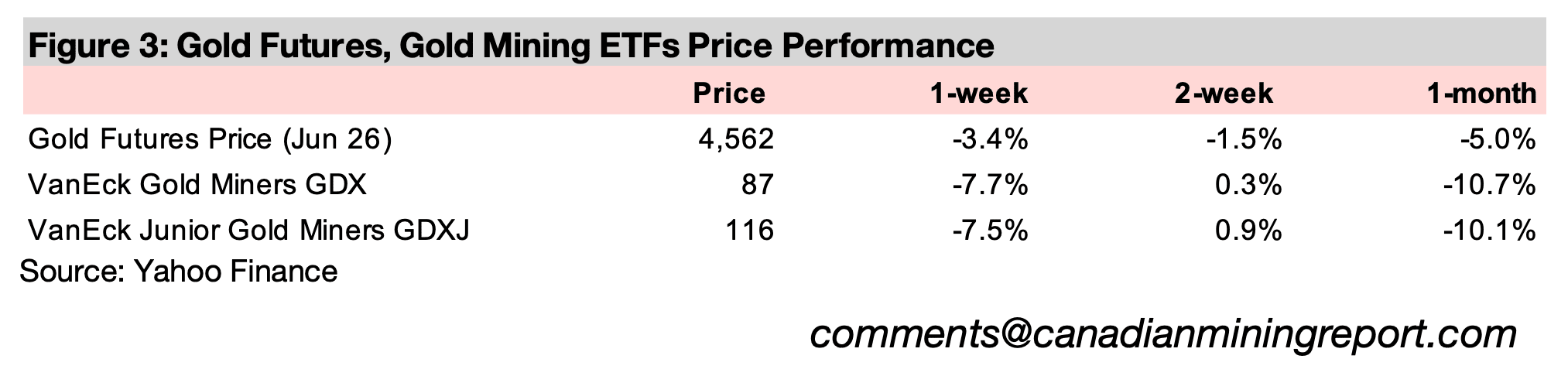

Gold declined -3.4% to US$4,562/oz, as the US$ and yields jumped on an unexpected rise in US inflation, and most other major metals declined even as energy issues in Peru were expected to affect global copper, silver and zinc supply.

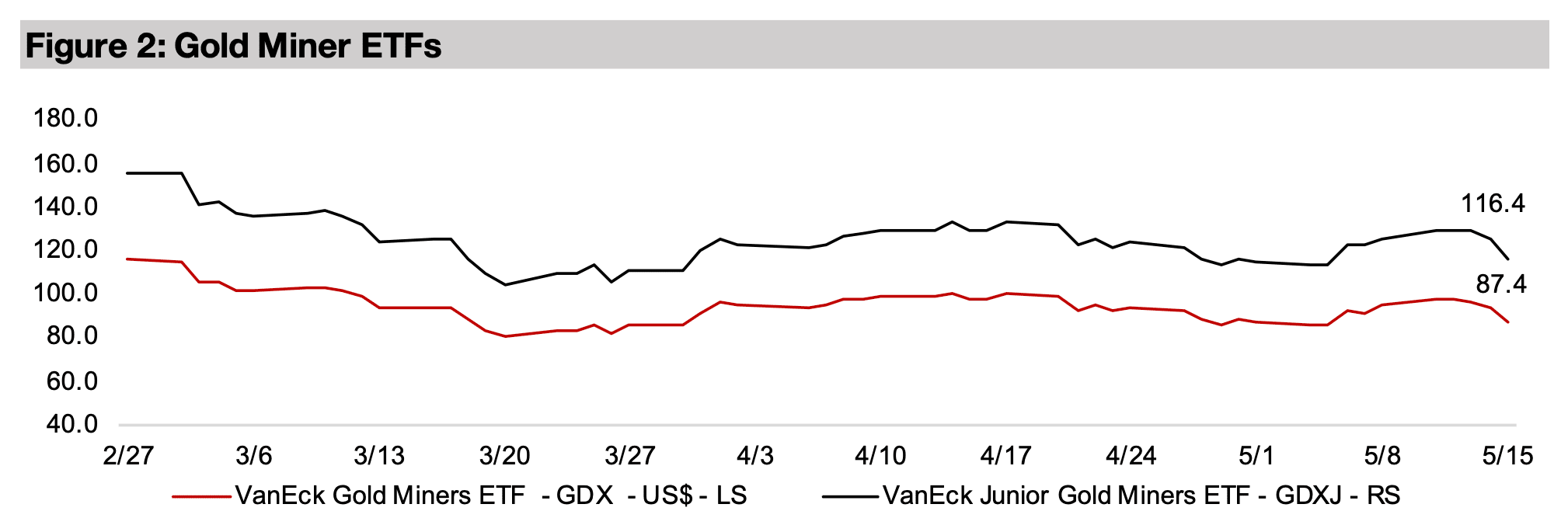

The gold stocks declined on the drop in the metal price, with the GDX down -7.7% and GDXJ off -7.5%, and a cooling of the equity market rally, with the S&P 500 and Nasdaq still up 0.3% but the Russell 2000 small cap index down -2.5%.

The gold price declined -3.4% to US$4,562/oz, driven by a jump in the US$ and yields

on shock inflation data, which increased expectations for a Fed rate hike. While this

caused a cooling of a near two-month risk-on rally, with the S&P 500 and Nasdaq

pulling back from gains earlier in the week, both still were up 0.3%. However, the

Russell 2000 declined -2.5%, showing more underlying risk aversion by markets than

indicated by the large caps. The gold stocks were hit by the decline in the metal price,

significantly underperforming even the losses for small caps, with the GDX down -

7.7% and GDX losing -7.5%.

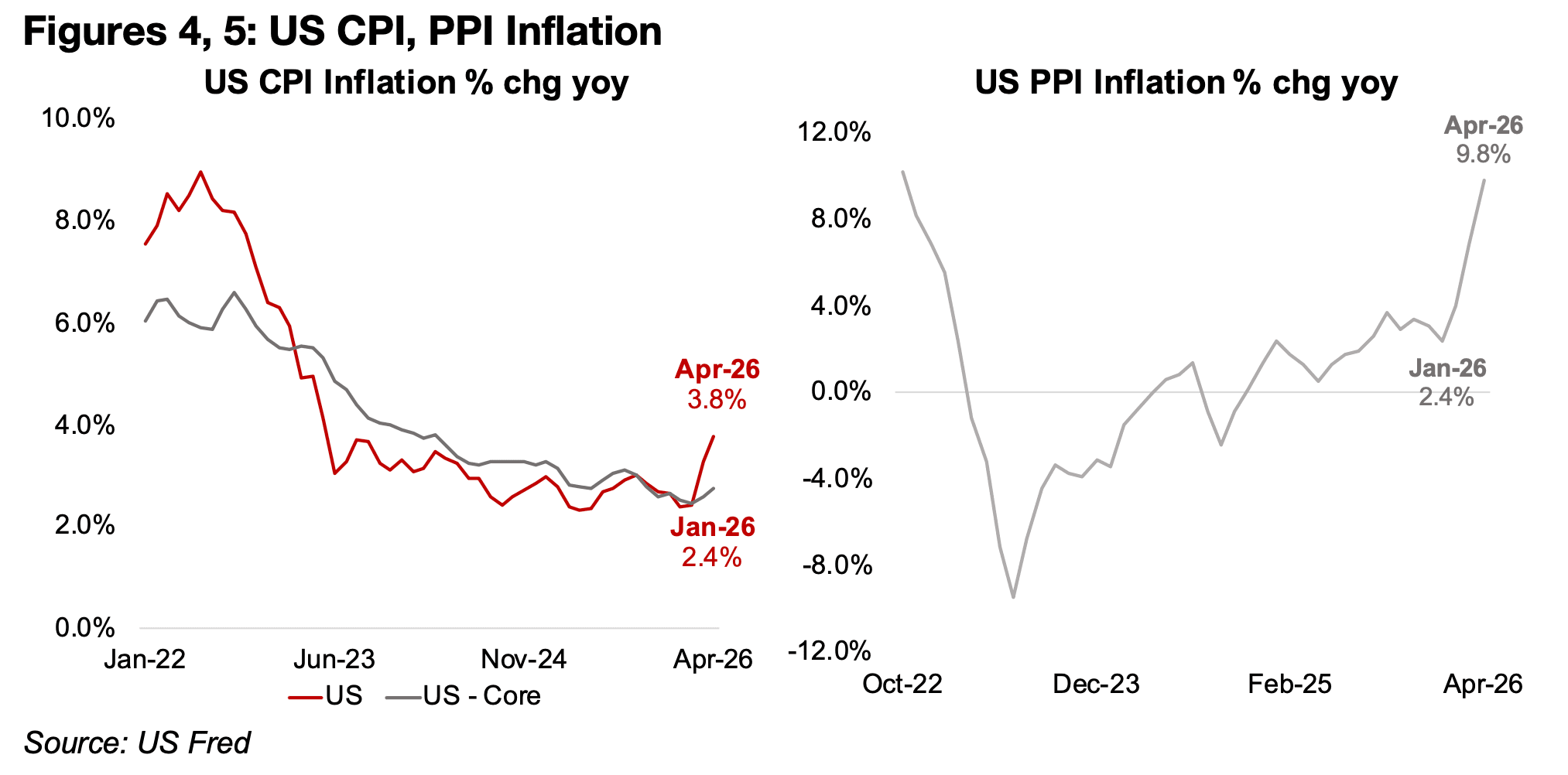

US headline inflation spiked to 3.8% yoy in April 2026, up from just 3.3% in March

2026 and well above the 2.4% lows for the year in January 2026 (Figure 4). While this

was mainly driven by the oil shock, core inflation excluding the more volatile energy

and food prices also rose, to 2.7% from 2.6% in March 2026 and up from lows of

2.5% in February 2025. There was an even greater jump in the Producer Price Index

inflation to 9.8% yoy in April 2026 from 6.9% in March 2026 and up from just 2.4%

in January 2026 (Figure 5). The PPI is also a negative indicator for potential increases

in consumer prices later in the year, as producers are likely to pass along some of the

increase down the supply chain, and this can take several months before it starts to

show up also in the CPI Index.

This will put the Fed in a more difficult position, with inflation spiking at the same time

as the employment situation has been weakening, with the former generating

pressure to hike rates and the latter to cut. The probability of a rate hike this year rose

substantially after this inflation data was released, indicating that the market expects

that sudden jump in prices could take precedence over the relatively low jobs data.

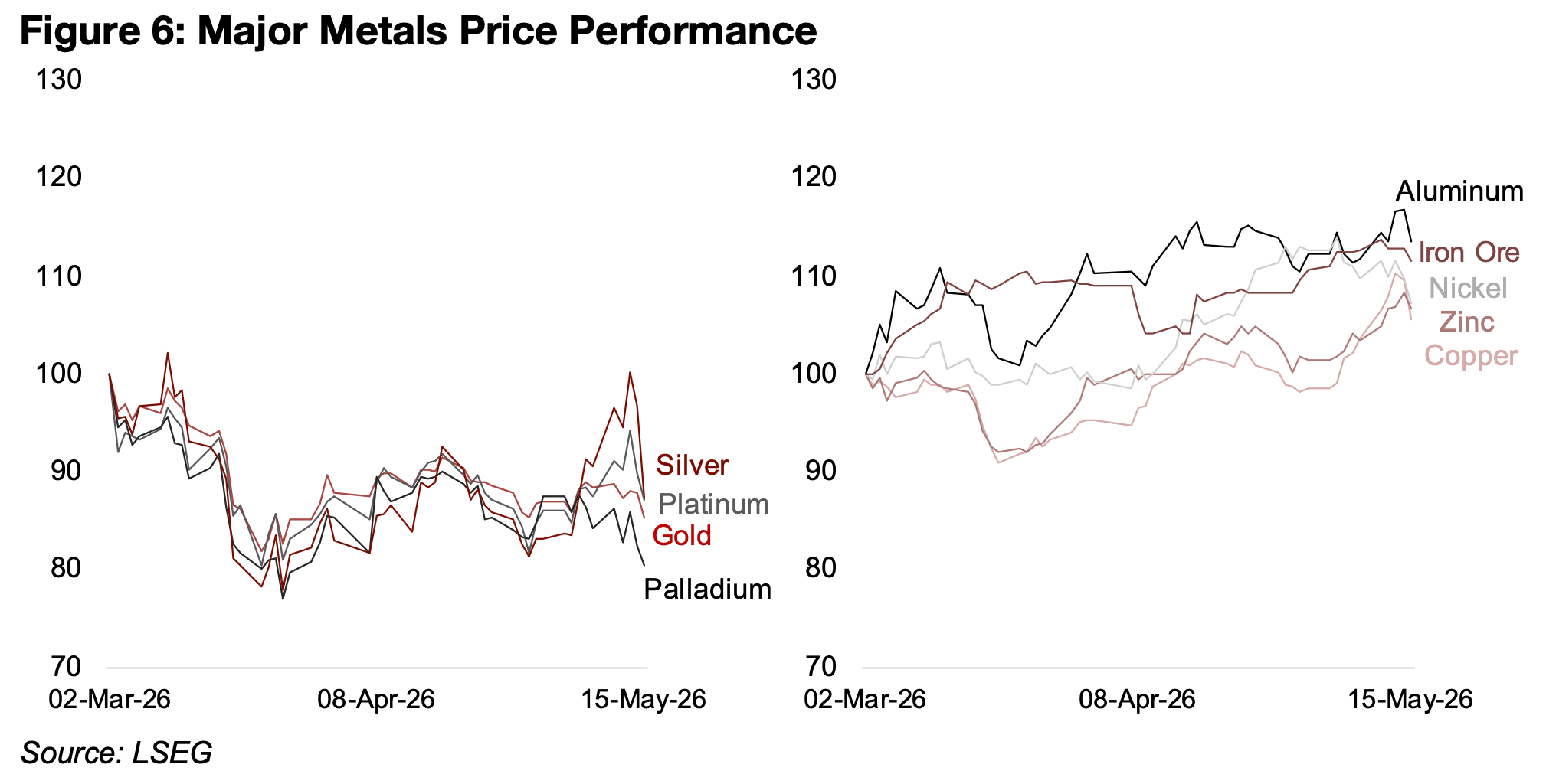

The major metals were mixed with copper down -3.7% and nickel losing -3.4%, but

aluminum near flat, with a decline of just -0.2%, while iron ore gained 3.7% and zinc

3.2% (Figure 6). The precious metals were hit particularly hard, with silver smashed -

11.2%, platinum down -6.0% and palladium up -5.9%. However, for silver this

followed a major spike in the previous week and once again pointed to large

speculative positions in the metal which were reversed immediately on the higher

inflation.

Since the start of the Middle East conflict at the end of the February 2026, the

precious metals have been the clear underperformers, with silver, platinum, gold and

palladium still all down by well over -10%. The base metals have been the major

gainers, with aluminum, iron ore, nickel, zinc, copper and iron ore all up by 5% or

more. The major driver behind the precious metals slump has been especially from a

shift in the monetary outlook from an expected expansion for the rest of 2026 to a

potential tightening, although for now, financial conditions remain very liquid.

The rise in the base metals does not appear to have been driven by any major

improvement in the global outlook for economic growth, especially given much higher

oil prices, but rather sector specific issues. The strongest gains, from aluminum, have

been driven by fundamental issues with supply, with capacity in the Middle East, one

of the leading global suppliers, directly attacked and expected to reduce output for

over a year. Iron ore, nickel and zinc are especially driven by growth in the global steel

industry, which while still sluggish, has seen a less severe contraction in recent

months. Copper seems to have been heavily driven by the AI story, with demand

especially for data centers, although the sustainability the market has become much

skeptical this year on the sustainability of the boom.

One issue that could hit supply for several of the major metals is an energy crisis in Peru, after damage to a natural gas pipeline that was a key supplier of the fuel for the country. This exacerbated an already difficult energy situation in the country with the state-owned oil company having been in a financial crisis since 2022. This could mean a substantial hit to global supply especially of copper, silver, and zinc, with it the third largest producer for the two former and second largest for the latter. The country has issued an emergency decree and measures including telework for state employees, intended to reduce energy consumption in the country and guarantee the supply of fuel.

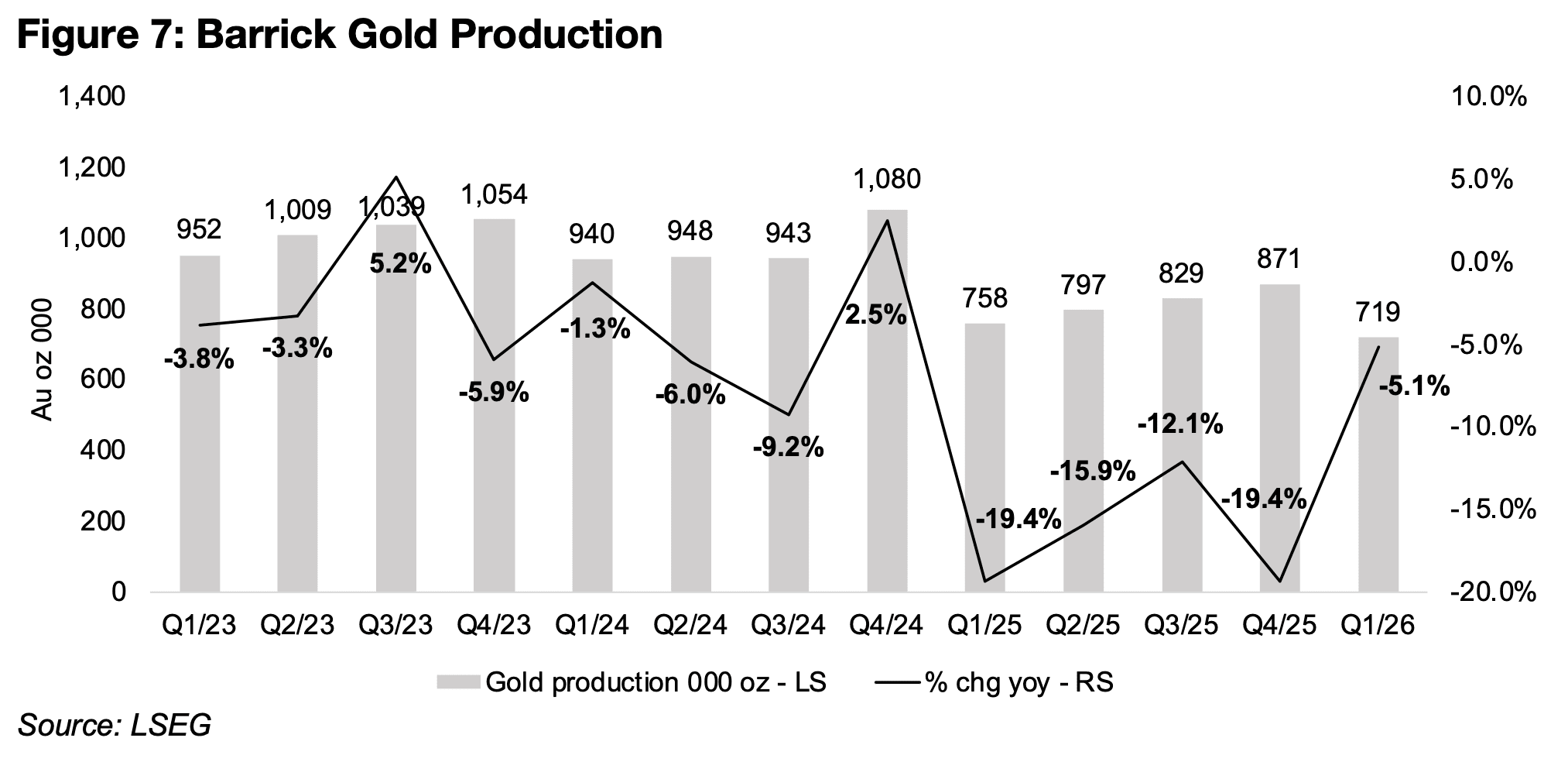

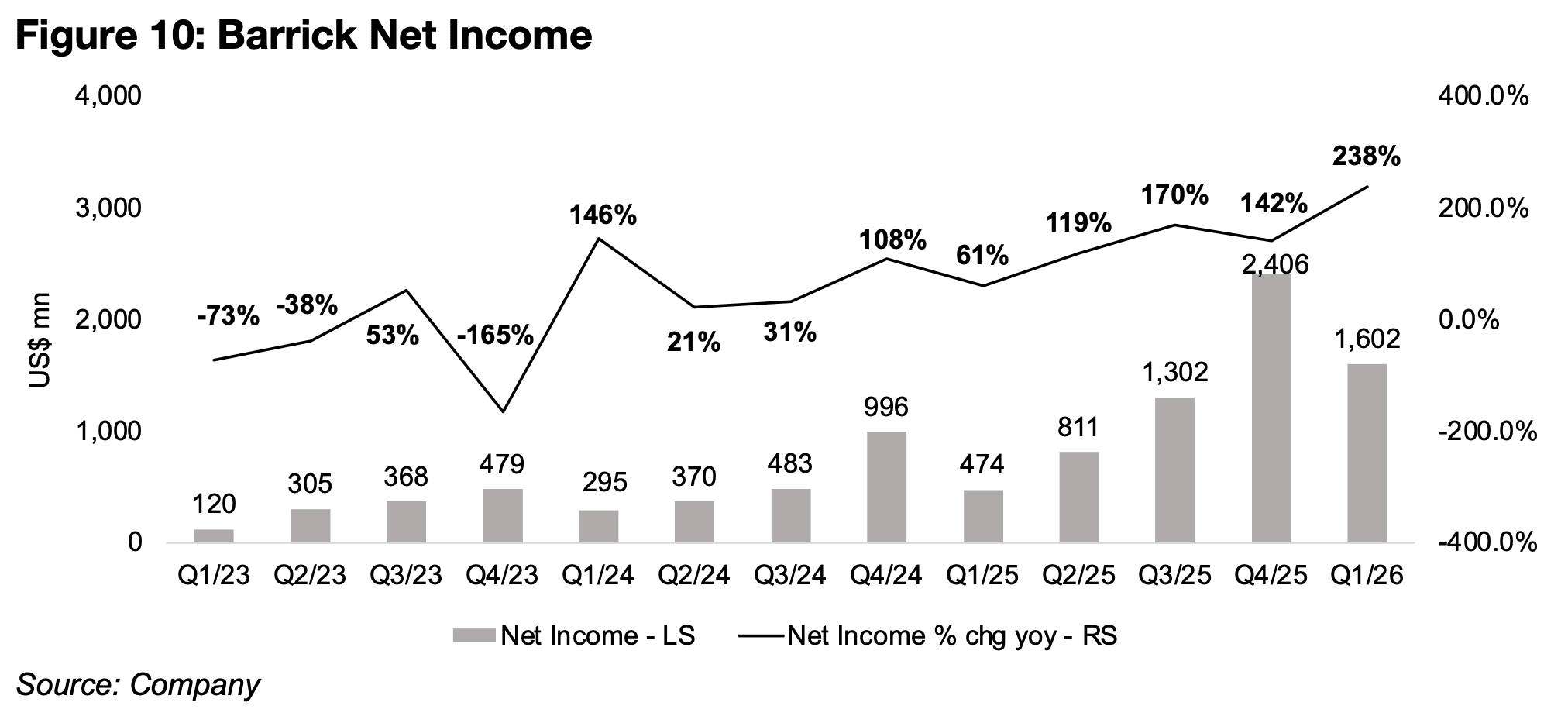

The Q1/26 results of Big Gold were completed with Barrick the last major to report.

Production contracted yoy, similar to the trend for Newmont and Agnico Eagle, down

-5.1%, although this was an improvement from four quarters of growth below -10%,

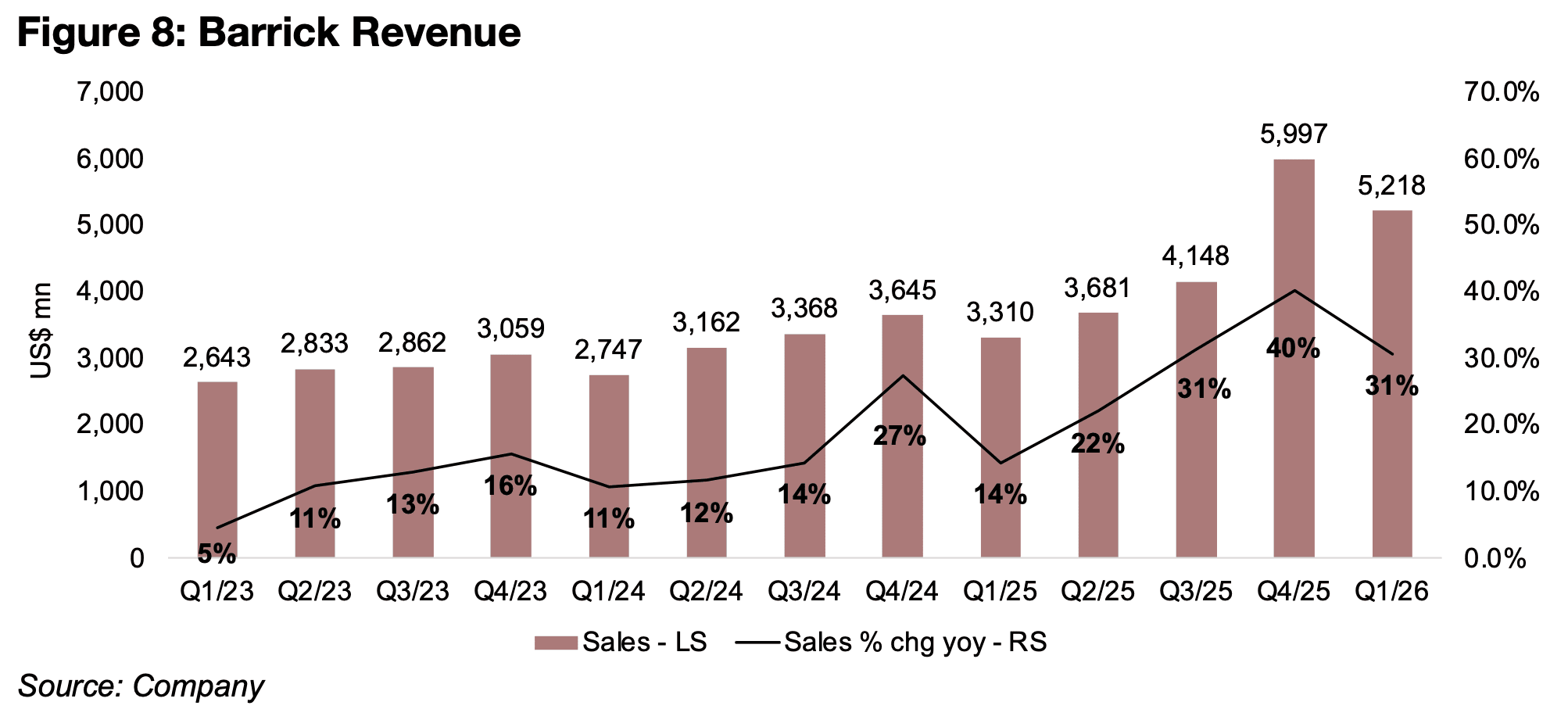

including two with -20% declines from Q1/25 to Q4/25 (Figure 7). Revenue growth

actually declined to 31% yoy from a peak of 40% in Q4/25, in contrast with many

other gold majors which saw their Q1/26 growth rates at by far the highest levels in

years (Figure 8).

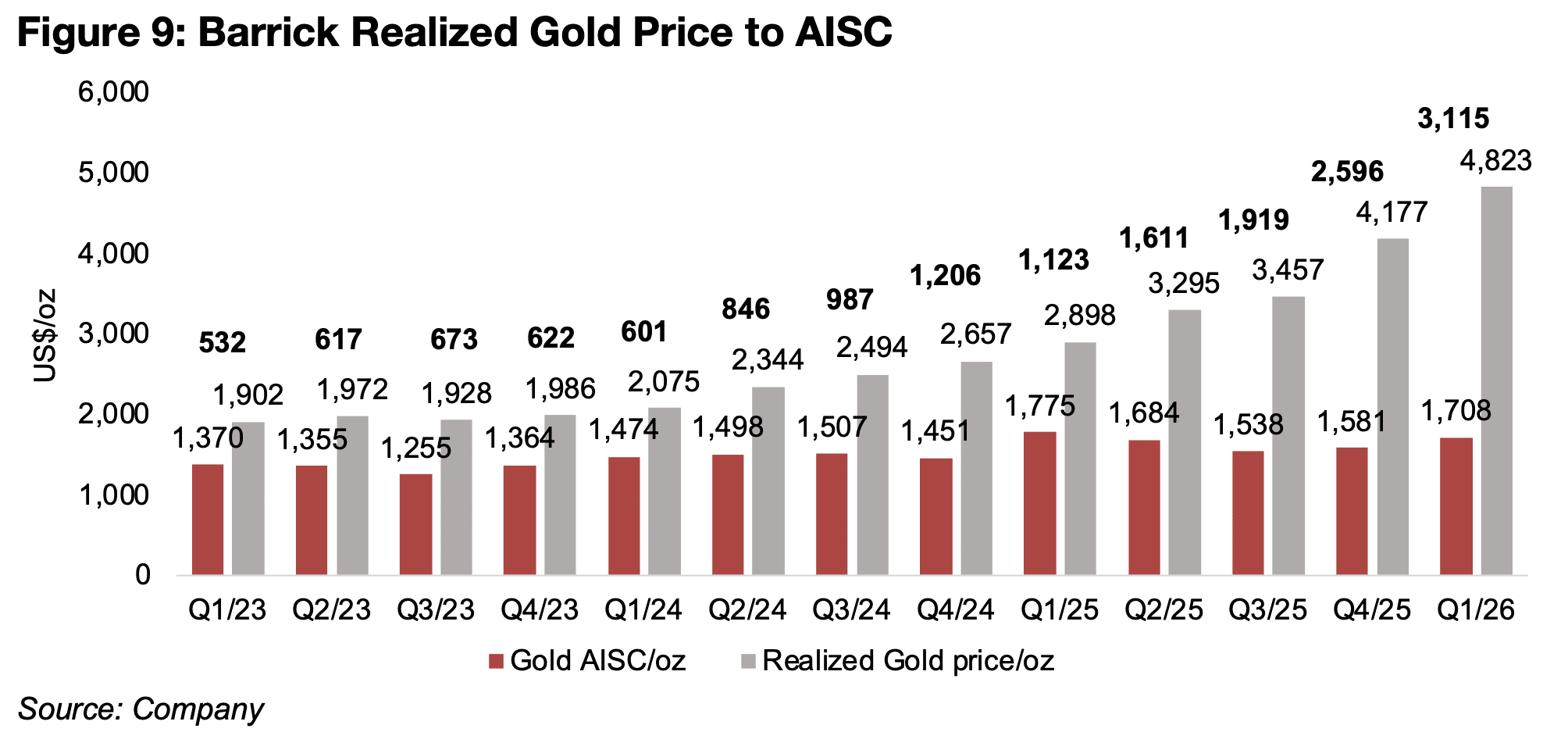

This came from a relatively low increase in the average realized gold price by 8.0%

qoq, versus 16.2% and 16.8% for Newmont and Agnico Eagle, and a much higher

rise in AISC, by 15.5%, versus just 5.5% for Newmont and a -2.2% decline for Agnico

Eagle. However, there was still a huge gain the average realized gold price yoy, by

nearly US$2,000/oz to US$4,823/oz, while the AISC declined slightly to US$1,708/oz,

seeing the company’s operating spread widen to US$3,115/oz from US$1,123/oz

(Figure 9).

While this drove up net income 238% yoy to US$1,602mn, there was a US$1,200mn drop quarter on quarter, as the average realized gold price increase was muted and costs surged (Figure 10). This made Barrick one of the only major companies in the gold sector where cost inflation was starting to show some signs of really offsetting the strong gold price. For the past several quarters there had been an interrupted surge in the gold price while costs increases had remained subdued and for some companies actually declined year on year. This could be a warning signal for Q2/26 results, as the rising costs for Q1/25 would have been mainly driven by the surge in oil prices, which only started in March 2026 and therefore were only realized for a month of this quarter. Overall, while year on year growth is still likely to be strong in Q2/26 there may be some quarter on quarter growth issues for the sector, especially as the gold price has been relatively weak.

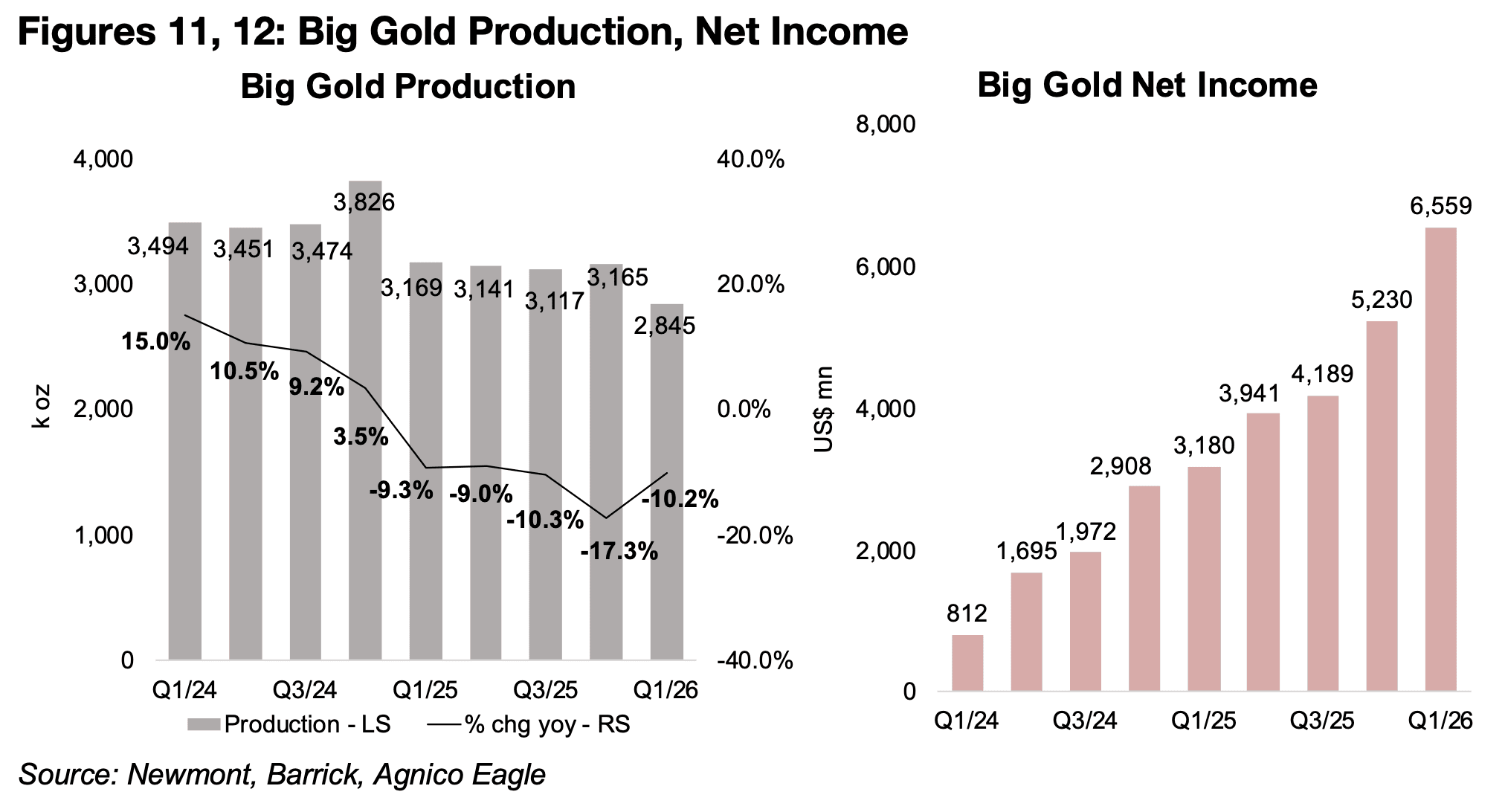

Nonetheless, Big Gold still had a massive Q1/26 overall year on year, even with some issues at Barrick quarter on quarter, which were not in evidence at Newmont or Agnico Eagle, which saw extremely strong qoq as well as yoy increases. The main issue for the sector remains the significant decline in gold production year on year, which did improve moderately to -10.2% in Q1/26 off lows of -17.3% in Q4/25, but is still in a substantial downtrend overall for the past few years (Figure 11). Obviously the rise in the gold price has completely offset set this at the net income line, but as Barrick showed, costs are starting to rise, and there may be issues with further gains in gold if central banks do start to increase interest rates (Figure 12).

While this can cause bond yields to rise, with inflation also spiking, it is unclear whether real yields, which subtract inflation from nominal yields, will actually expand or contract. Rising real yields can drive funds flows towards bonds and out of yieldless gold, as the opportunity cost of the holding the metal rises. For the junior gold miners, however, interest rate movements remain far beyond their scope of control, but there is clearly a major opportunity to develop new projects which could eventually be targets of the majors to offset their declining production.

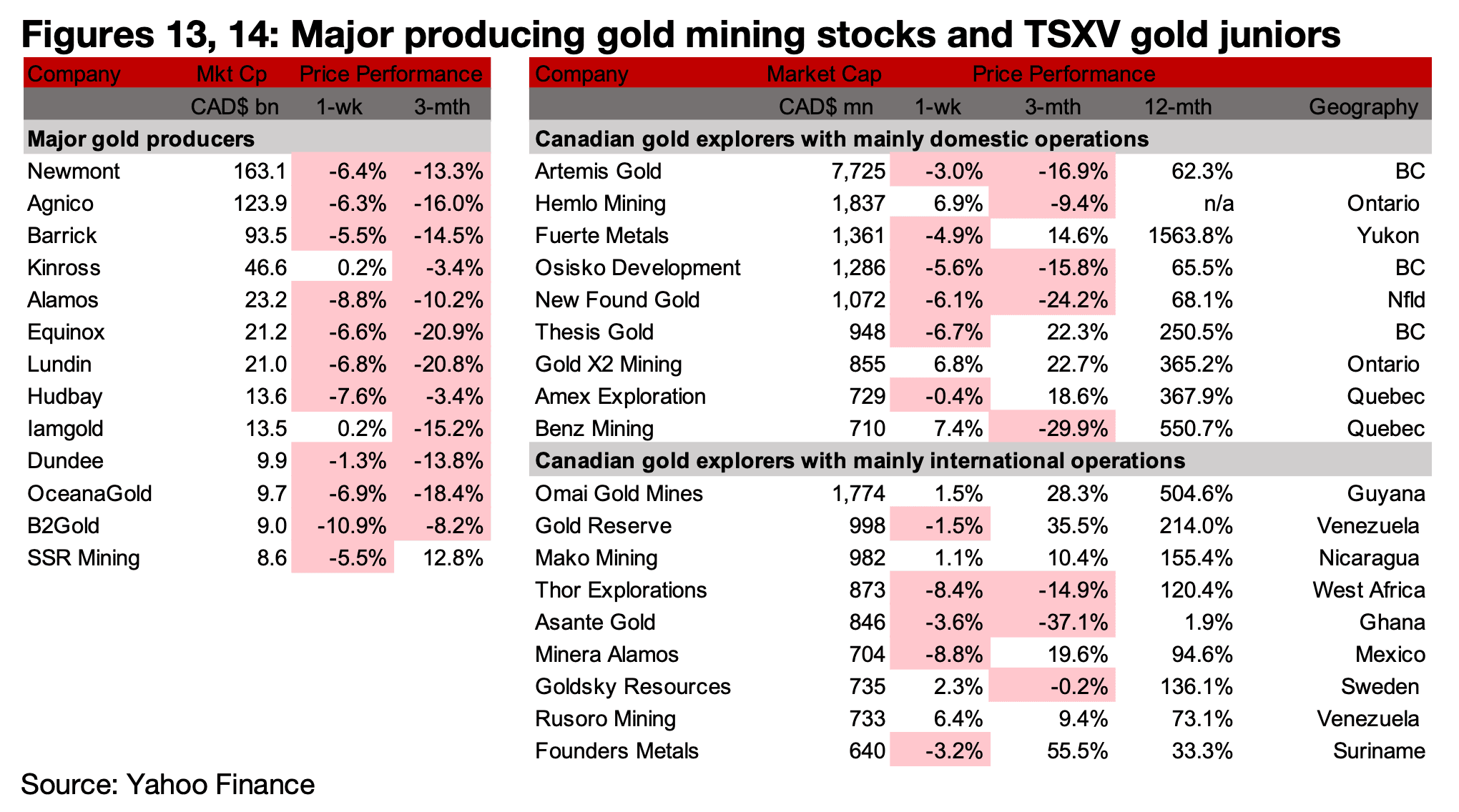

Most of the major producers and TSXV gold declined on the drop in the metal price

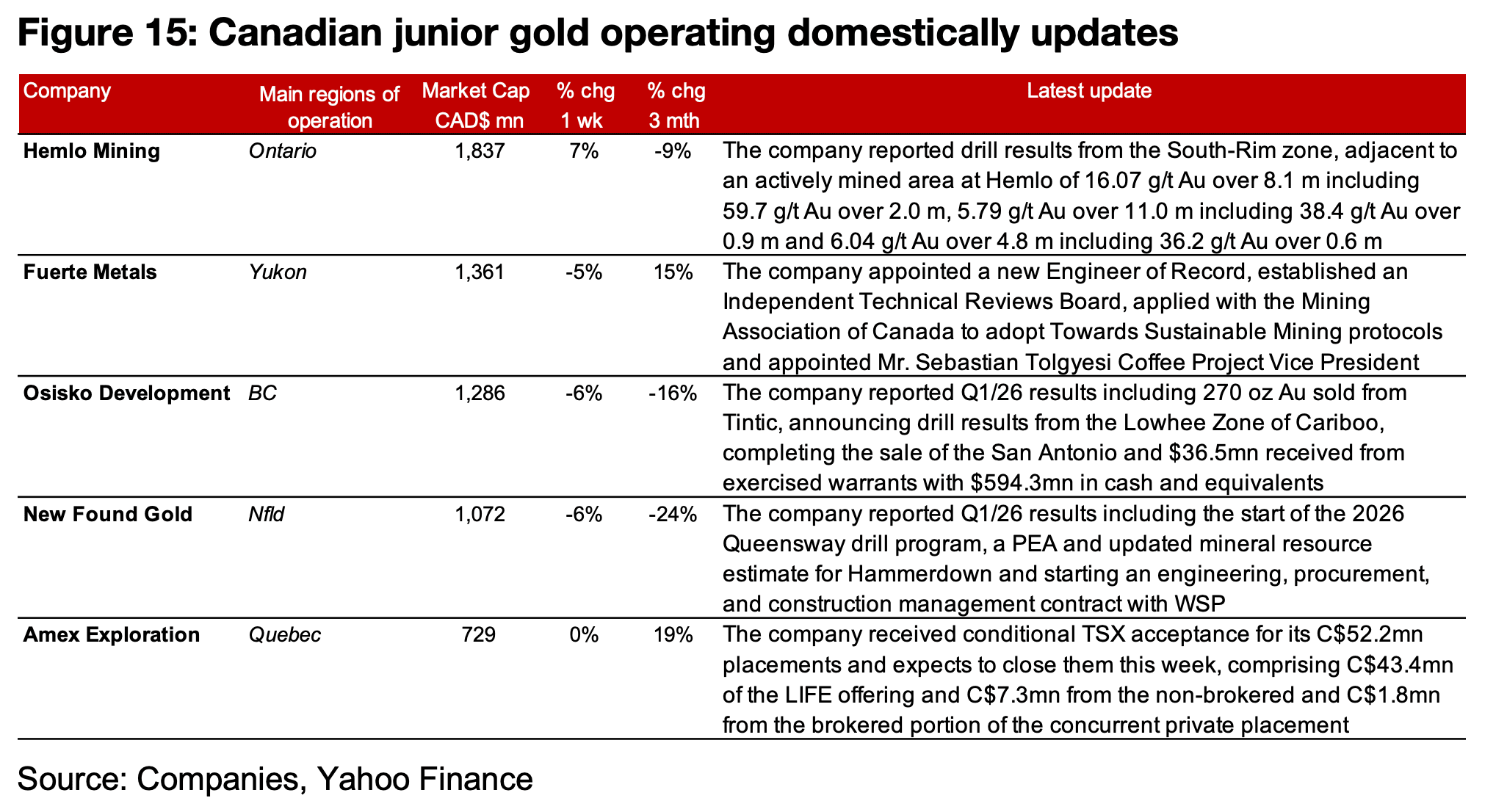

and pullback in equities (Figures 13, 14). For the TSXV gold companies operating

mainly domestically, Hemlo reported drill results from the South-Rim zone, Fuerte

Metals announced operational progress and appointed Mr. Sebastian Tolgyesi at

Vice President of the Coffee Project, Osisko Development and New Found Gold

announced Q1/26 results and Amex Exploration received conditional acceptance for

its two private placements for proceeds of C$52.2mn which it expects to close this

week (Figure 15).

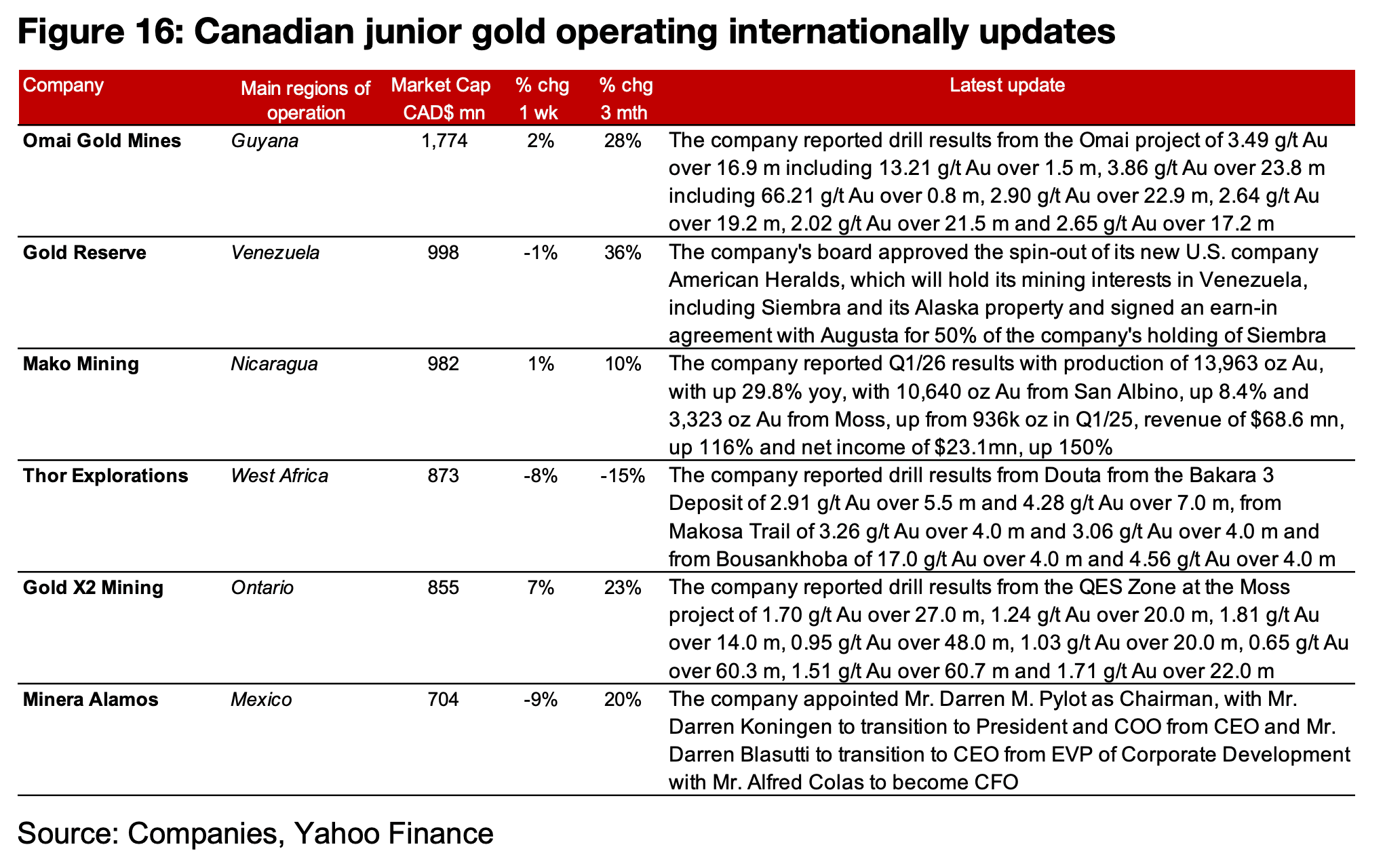

For the TSXV gold companies operating mainly internationally, Omai reported drill

results from the Omai project, Gold Reserve’s board approved the spin-out of its new

US company American Heralds, which will hold its mining interests in Venezuela and

its Alaskan property and Mako Mining reported Q1/26 results. Thor Explorations and

Gold X2 Mining reported drill results from three zones of Douta, and the QES Zone of

the Moss project, respectively, and Minera Alamos announced management

appointments (Figure 16).

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.

Author

Ben McGregor authors the Weekly Roundup at CanadianMiningReport.com, providing sharp analysis of the metals and mining sector. With a talent for spotting trends, Ben distills complex market shifts into clear, engaging insights on TSXV junior miners. His weekly updates cover gold, copper, uranium, and more, blending data-driven perspectives with a knack for identifying opportunities. A vital resource for investors, Ben’s work navigates the dynamic junior mining landscape with precision.