June 08, 2026

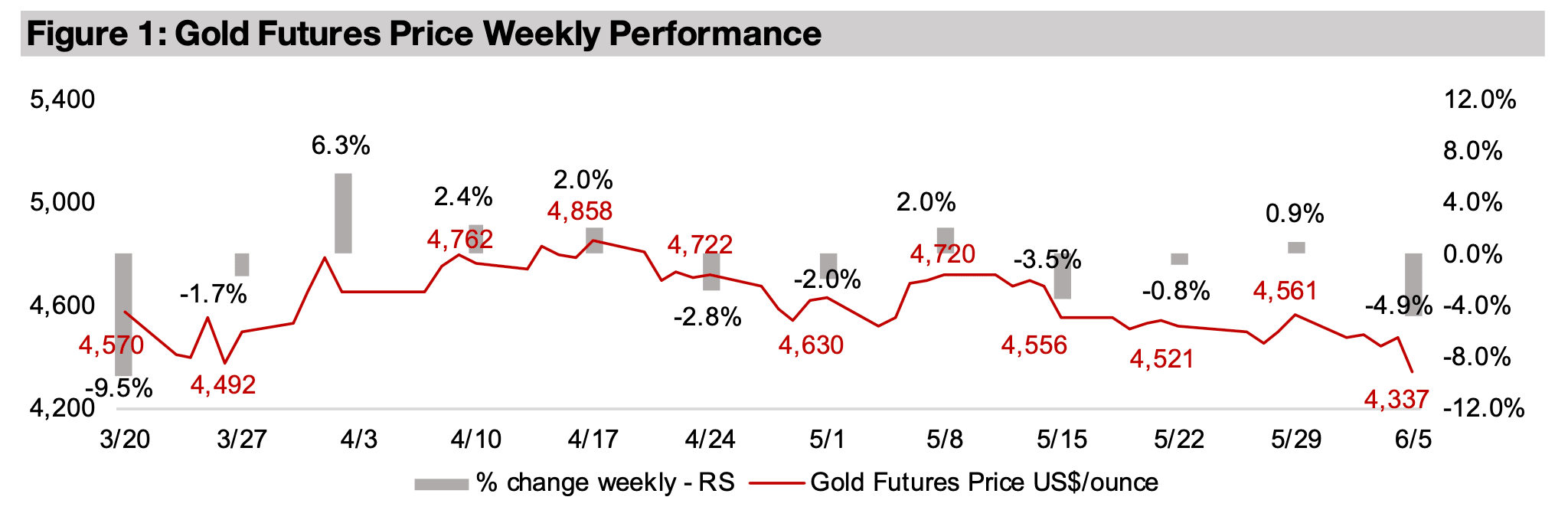

Gold dropped -4.9% to US$4,337/oz, near its lows for the year, as the US$ jumped driven by strong US jobs numbers for May 2025, which combined with high oil prices increased market concerns over inflation and expectations for Fed rate hikes.

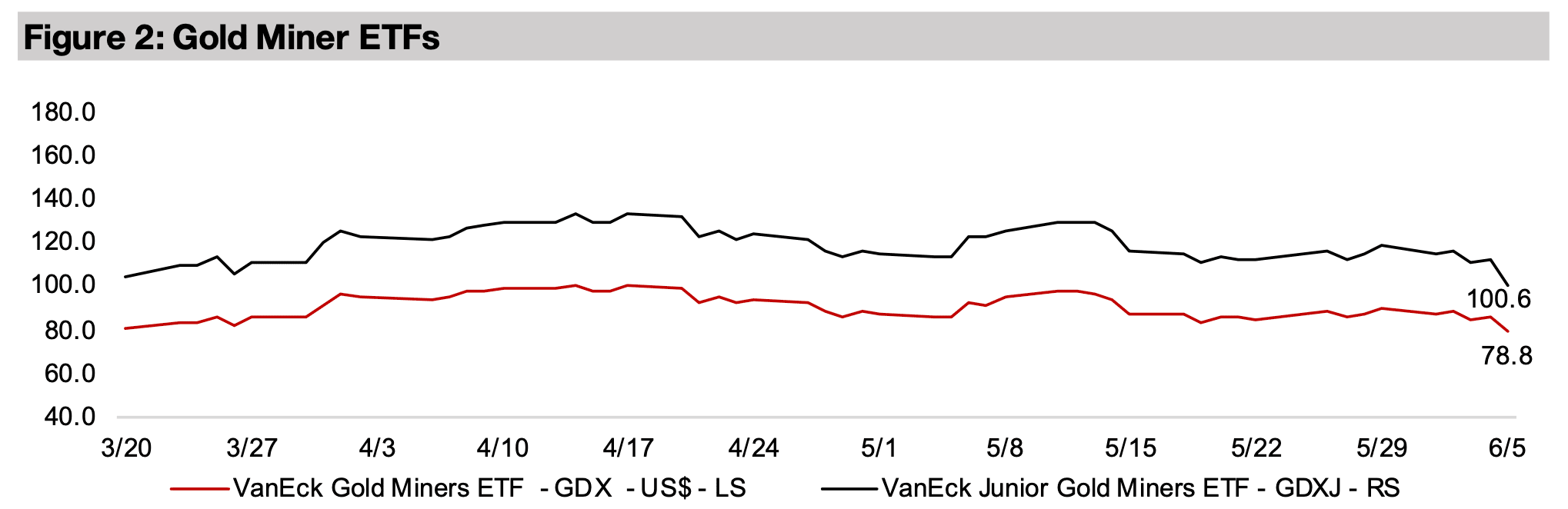

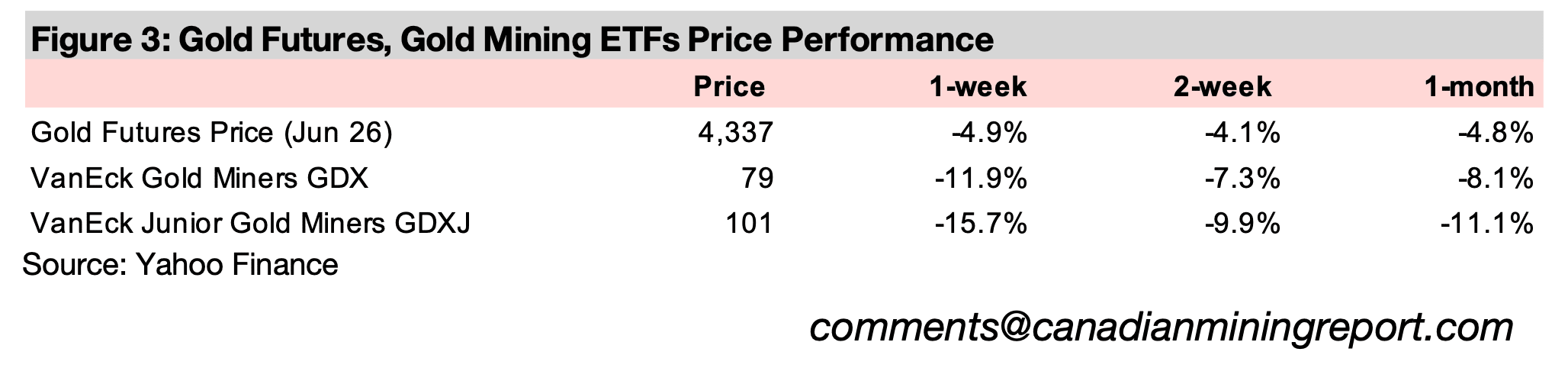

The gold stocks dropped to year to date lows, with the GDX down -11.9% and GDX declining -15.7%, on the pullback in the metal price and slide in equity markets, with the S&P down -2.6%, Nasdaq off -4.6% and the Russell 2000 losing -2.3%.

The gold price was down -4.9% to US$4,337/oz, its lowest level since the start of the

year, on very strong US jobs data, which combined with high oil prices added to

concerns of rising inflation and potential Fed rate hikes, and drove up the US$. The

markets declined substantially on the news, combined with the underlying pressure

of a still unclear situation in the Middle East, with the S&P 500 losing -2.6%, Nasdaq

slumping -4.6% and the Russell 2000 down -2.3%. The drop in the metal price and

slumping equities dragged down the gold stocks to their lows for the year, with the

GDX losing -11.9% and GDX plunging -15.7%.

The other precious metals crashed by around twice the rate of gold, with silver down

-8.9%, platinum declining -9.9% and palladium losing -11.3%. There were also

significant declines in copper, down -4.5% and iron ore, losing 6.3%, while aluminum

and nickel outperformed, with drops of only -2.0% and -2.4%. Aluminum continues

to be supported by major supply constraints from the Middle East war, with the region

accounting for nearly 10% of global output and some of the capacity directly attacked,

in addition to the limits on shipments through the Straits of Hormuz. Output of

aluminum has also reached a limit set by China to reduce emissions from the industry,

which has reduced new supply from the largest global supplier.

These declines in metals prices saw equities for these sectors drop, with the COPX

ETF of copper stocks down -7.8% and the SIL ETF of silver stocks losing -13.2%,

with the latter down for the year, but the former still up over 10.0%. The NIKL ETF of

nickel stocks dropped -12.3% and is down -19.0% YTD, even as the metal price has

gained 10.4% for the year. The rise in the nickel price has been driven by signs of

recovery this year after several years of severe oversupply mainly from an output

expansion in Indonesia, the largest global producer. The country has implemented

strict limits on new capacity for the industry and some forecasts are looking for a shift

to a deficit in 2026 after the huge surplus last year. The PICK ETF of the largest global

miners, which have substantial exposure to the major iron ore and copper producers,

declined -6.1%, broadly inline with the drop in these metals prices.

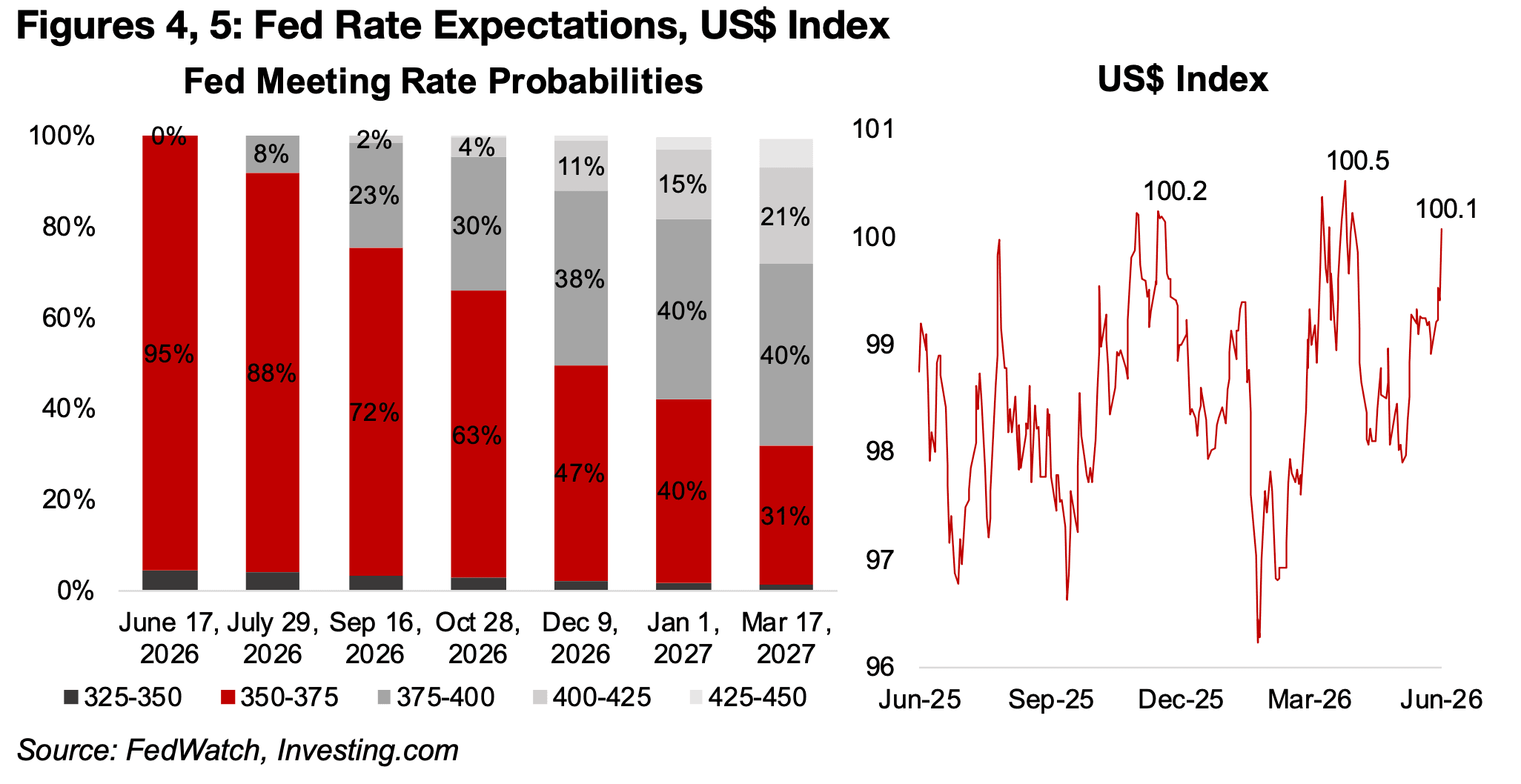

The market still expects the Fed to maintain rates at the current 3.50%-3.75% level

at its meeting this month with a 95% probability, with the chance of a hike at zero

and of a cut to 3.25%-3.75% low (Figure 4). However, from the July 29, 2026 meeting

the probability of a hike starts to rise, to 8%, and by December 9, 2026 it has

increased to over 50% with a 38% chance of an increase to 3.75%-4.00% and 11%

chance to 4.00%-4.25%, and only a small chance of a cut. This is a significant shift

from before the war in the Middle East, where it was widely expected that Fed, and

most global central banks would continue relatively loose monetary policy for 2026.

The expectations for higher rates drove up the US Index to 100.1, near its highest

levels in twelve months, continuing a major rise since the start of war, (Figure 5).

This drove some of the pressure on the gold price this week, with the dollar moving

inversely to the metal, and if the currency remains strong it could continue to hit the

metal price. There had been some concerns over the dollar’s role a safe haven in

2024 and 2025 after the country’s major new tariffs. However, the war has seen the

markets shift strongly back into the dollar, partly because the disruption to the oil

supply has far higher risks for the regions with its major competing currencies in

Europe, Japan and China. These are all major oil importers, while the US is effectively

energy independent and a major global net energy exporter.

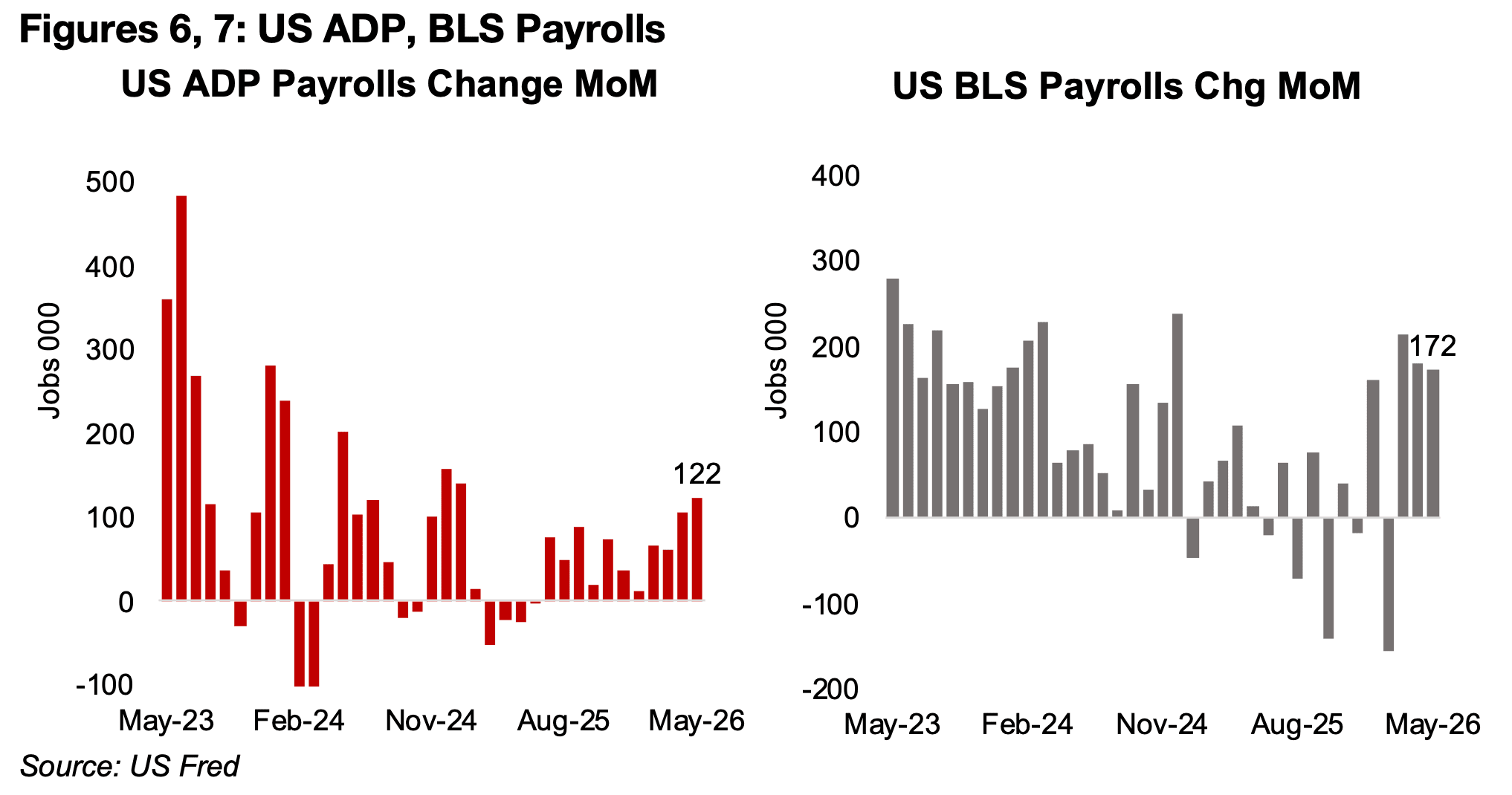

The May 2025 jobs data in the US continued a strong rebound over the past three months. US ADP payrolls rose 122k mom in May 2025, moderately ahead of consensus at 110k, and at their highest level since September 2025, following strong gains of 105k in April 2025 (Figure 6). The US BLS payrolls rose 172k mom, far outpacing the market estimate of just 80k, and marked the third month of strong data, with increases mom of 214k and 179k in March 2026 and April 2026, after a -156k plunge in March 2026 concerned markets over the employment situation in the country (Figure 7). US job openings also jumped far past expectations in April 2026, to 731k mom, after declines of -318k in February 2026 and -35k in March 2026. While the Fed has a dual mandate to keep inflation relatively low and maximize employment, with both of these measures now rising, it would appear that they could drive the Fed toward a potentially more hawkish stance.

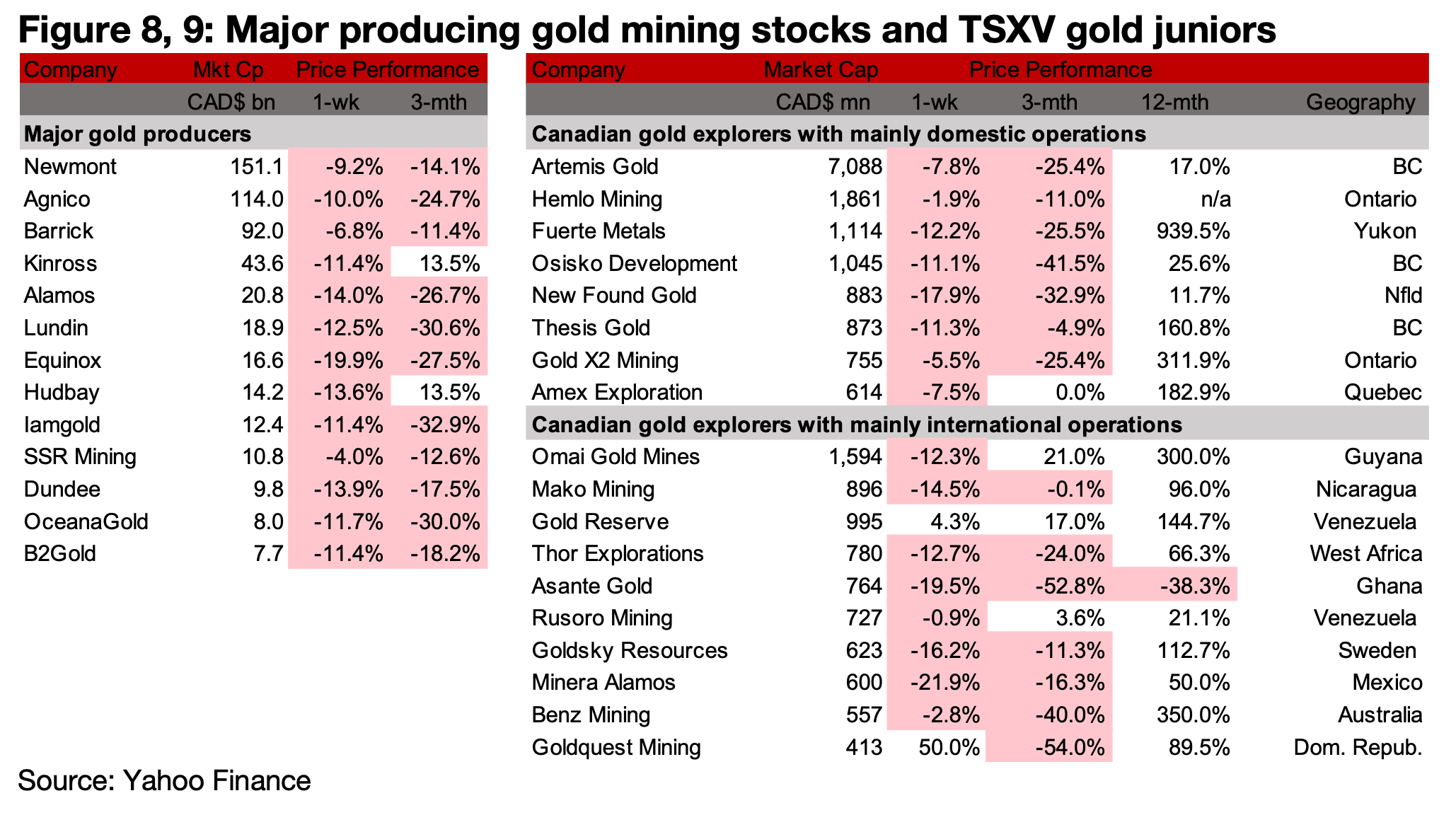

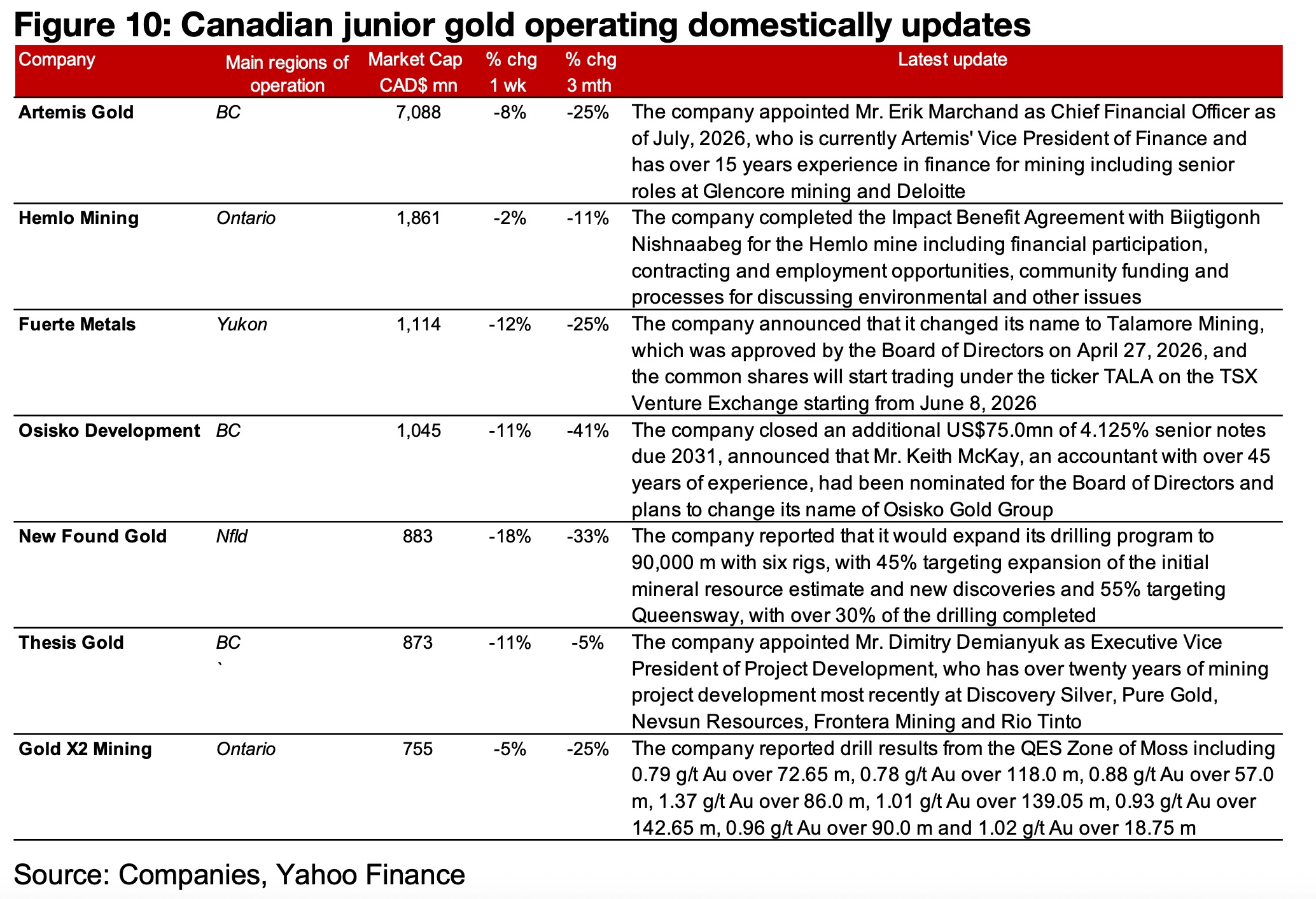

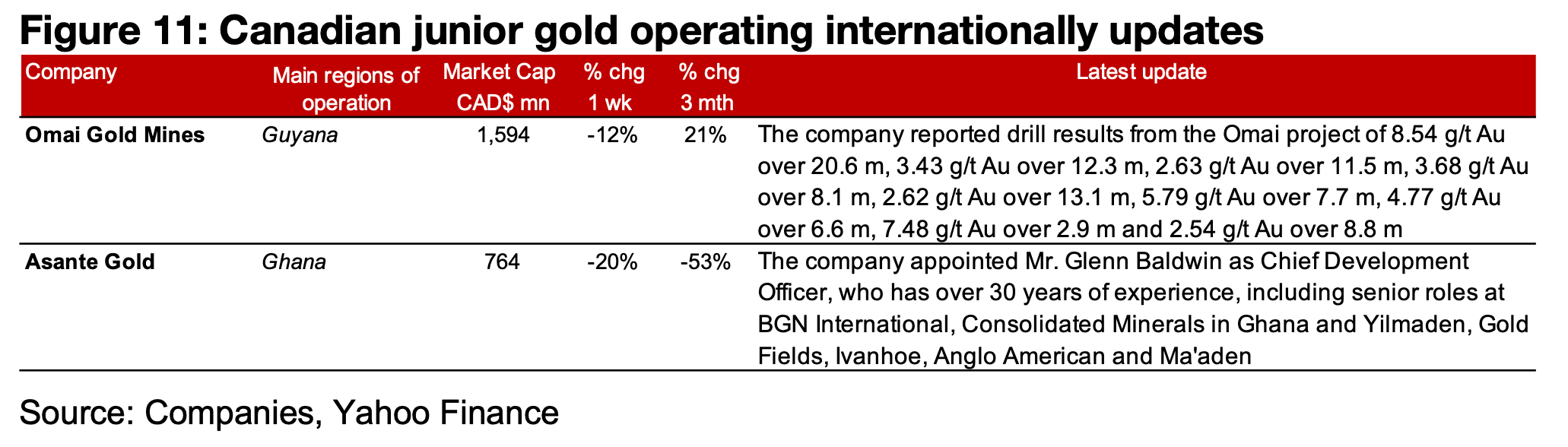

The major producers and most of TSXV gold saw significant declines on the drop in gold and equities (Figures 7, 8). For the TSXV gold companies operating mainly domestically, Artemis appointed its new Chief Financial Officer, Hemlo completed an Impact Benefit Agreement and Fuerte changed its name to Talamore. Osisko Development closed US$75.0mn in senior notes, nominated a new Director to its Board, and announced plans to change its name to Osisko Gold Group. New Found Gold expanded its drill program for 2026 to 90,000 m, Thesis appointed its Executive V.P. of Project Development and Gold X2 reported drill results from Moss (Figure 9). For the TSXV gold companies operating mainly internationally, Omai reported drill results from Moss and Asante appointed a Chief Development Officer (Figure 10).

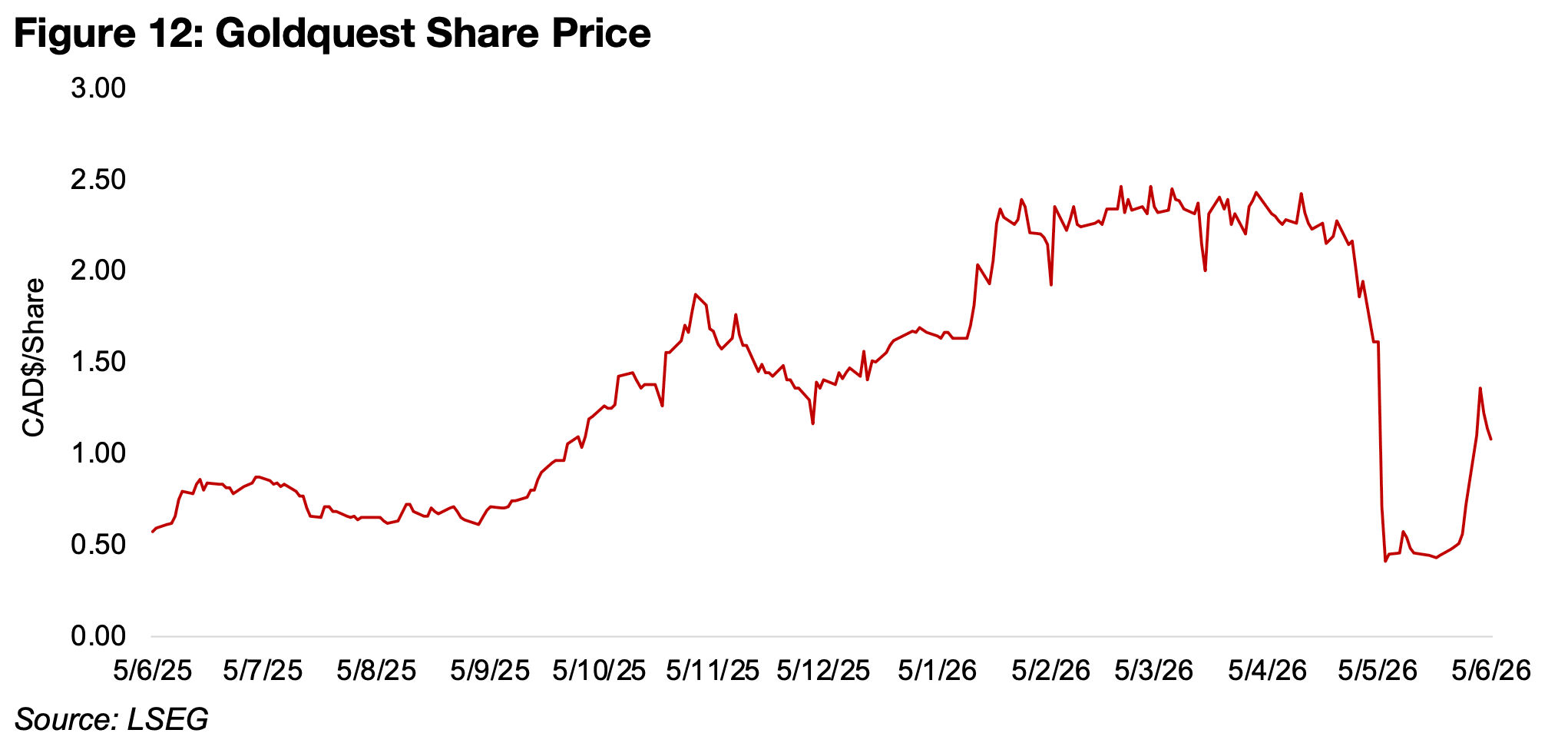

The only major TSXV stock standing out for major gains over the past week has been

Goldquest mining, which has surged 50%. However, this follows an 80% crash in the

share price in the first week of last month, after it averaged over CAD$2.0/share from

February 2026 to April 2026 (Figure 12). The shares started to rebound last week with

a 63% gain, and with the further jump this week, it has reached about half the average

level prior to the crash. The drop in early May was driven by the decision of the

government of the Dominican Republic for a temporary halt to operations at

Goldquest’s Romero project in the country after major protests related to concerns

over potential environmental issues.

The protests were mainly from fears the Romero project could pollute the water

supply in the mainly agricultural local area. This comes after Barrick’s Pueblo Viejo

gold project in the country led to a large number of people from local communities

having either already been relocated, or in the application process to be moved by

the government, because of environmental issues from the mine. The mine has been

operating since 2012, and there have been several significant protests since.

However Goldquest has stated that its underground mine would have a much more

limited environmental impact than Pueblo Viejo, which is an open pit mine and can

create more significant issues for local communities.

One of the key complaints over Pueblo Viejo has been regarding local water pollution

from the tailings dam of the project. However, Goldquest’s Romero would use

methods that would turn tailings into a solid form which is considered a much more

environmentally friendly and less risky method. This avoids one of the most severe

risks, of tailings dams bursting, but also waste slowly seeping into the water supply.

Goldquest made announcements on May 4th and May 5th, 2026, of its commitment

to operate in full compliance with Dominican law, including the environmental process,

engage with communities and stakeholders, and advance its Environmental and

Social Impact Assessment. The company has not received either an Exploitation

Concession or Environmental License which are both required before the start of

development. While the Dominican Republic has not made any official announcement

that operations at Romero can be restarted, presumably there has been some

progress in negotiations between Goldquest and the government which has partly

driven the recovery in the share price. Although the company did announce strong

drilling and metallurgical results on May 28, 2028, just prior to the rebound, even

outstanding operational results would not necessarily drive up the market value if

there were expectations that the project would remain halted indefinitely.

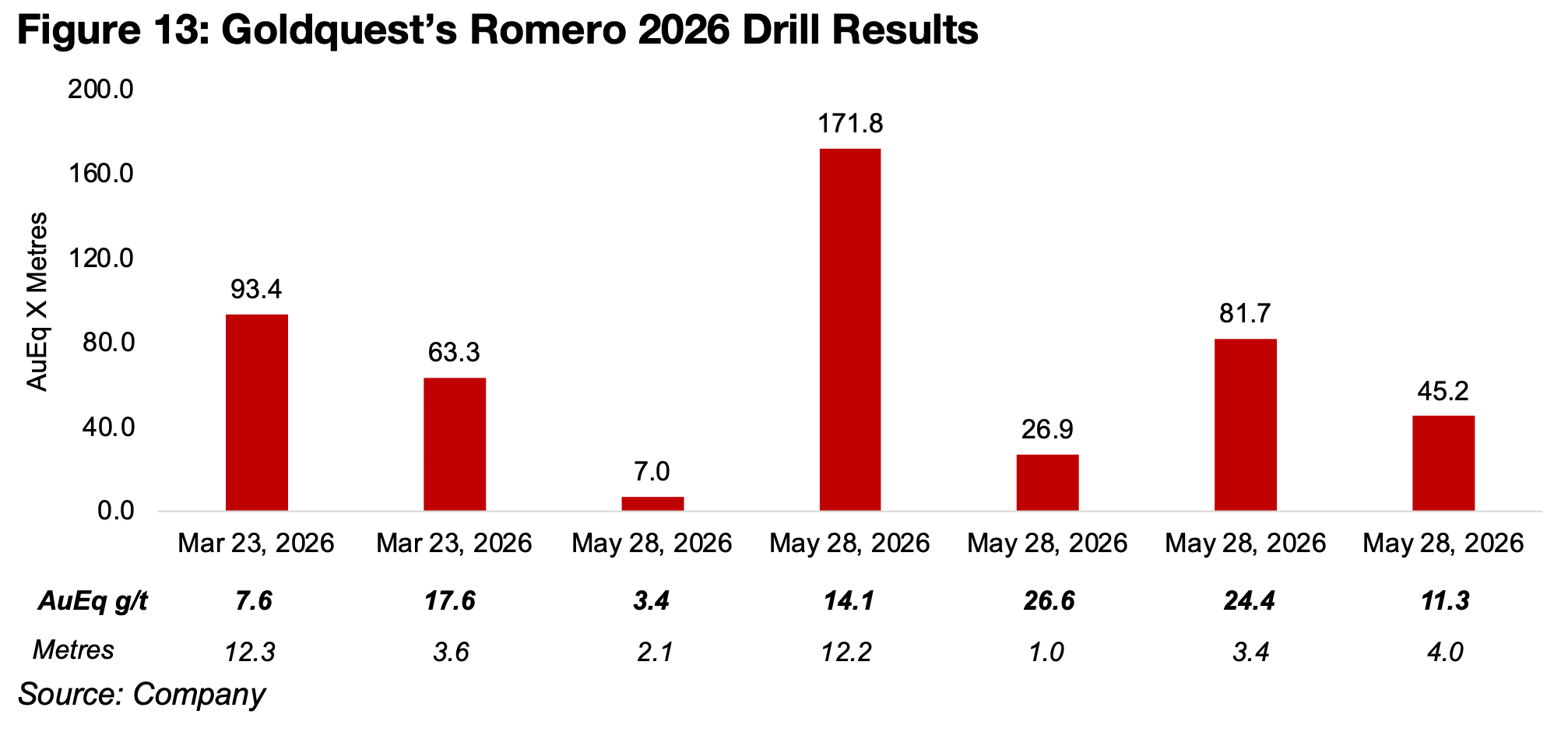

The company reported their strongest drill results from Romero on May 28, 2028 with

a grams-thickness as high as 171.8, comprising 14.1 AuEq g/t Au over 12.2 m and

81.7, with 24.4 g/t AuEq over 3.4 m (Figure 13). This was ahead of the previous

strongest grams-thickness of 93.3 reported on March 23, 2026, with 7.6 g/t AuEq

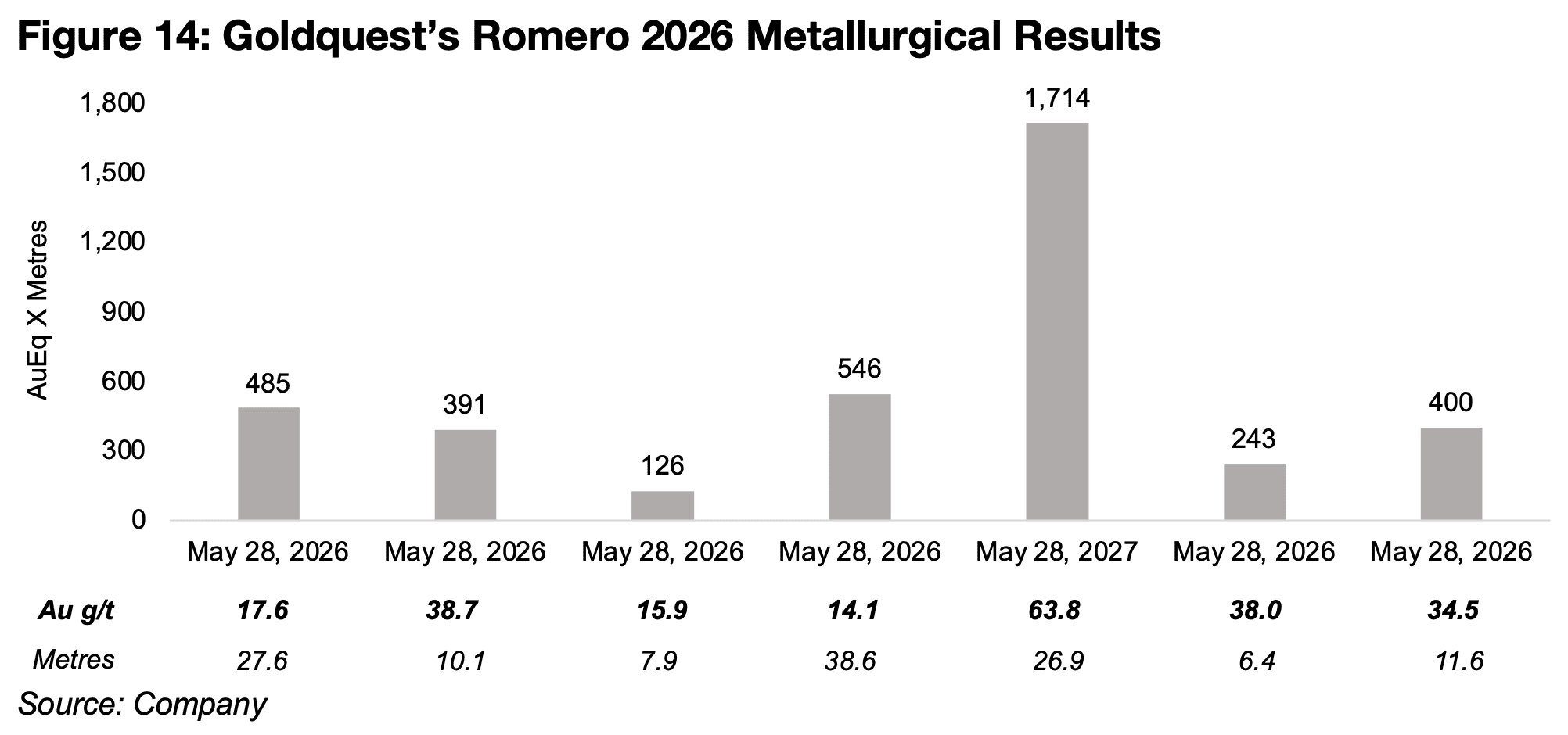

over 12.3 m. The company also reported strong metallurgical drilling results on May

28, including a grams-thickness of 1,714, comprising 63.8 g/t Au over 26.9 m, and

several other results with a grams-thickness of around 400-550 (Figure 14).

The company does have significant participation by holders in the Dominican

Republic, which hold 40% of the shares, which could provide domestic support in

getting government approval to restart the process, while Agnico Eagle is also a large

shareholder, with 10.2% of the company. Goldquest remains well funded, with

CAD$50mn in cash as of May 2026, after completing a private placement of C$43mn

in three tranches, with the first tranche of CAD$31mn completed in December 2025,

and the second and third in January 2026 of CAD$9mn and CAD$3mn.

However, the potential for further protests could remain a major overhang on the

share price until there is a clear indication from the Dominican Republic government

that the company can continue operating. This will leave the share price open to

abrupt moves in either direction on announcements regarding the stance of the

government and local communities on the project. Also, the experience of Barrick in

the country suggest that protests could arise even after permitting. The company’s

exploration has also been almost entirely concentrated in the country and cannot

easily shift to other projects. While it is exploring the Cachimbo project in Dominican

Republic, this is adjacent to Romero, and could face similar opposition from local

communities. However, assuming that the company does resolve the issues to the

satisfaction of the government and local communities, it does have a longer-term

opportunity to develop the relatively large Romero-Cachimbo corridor.

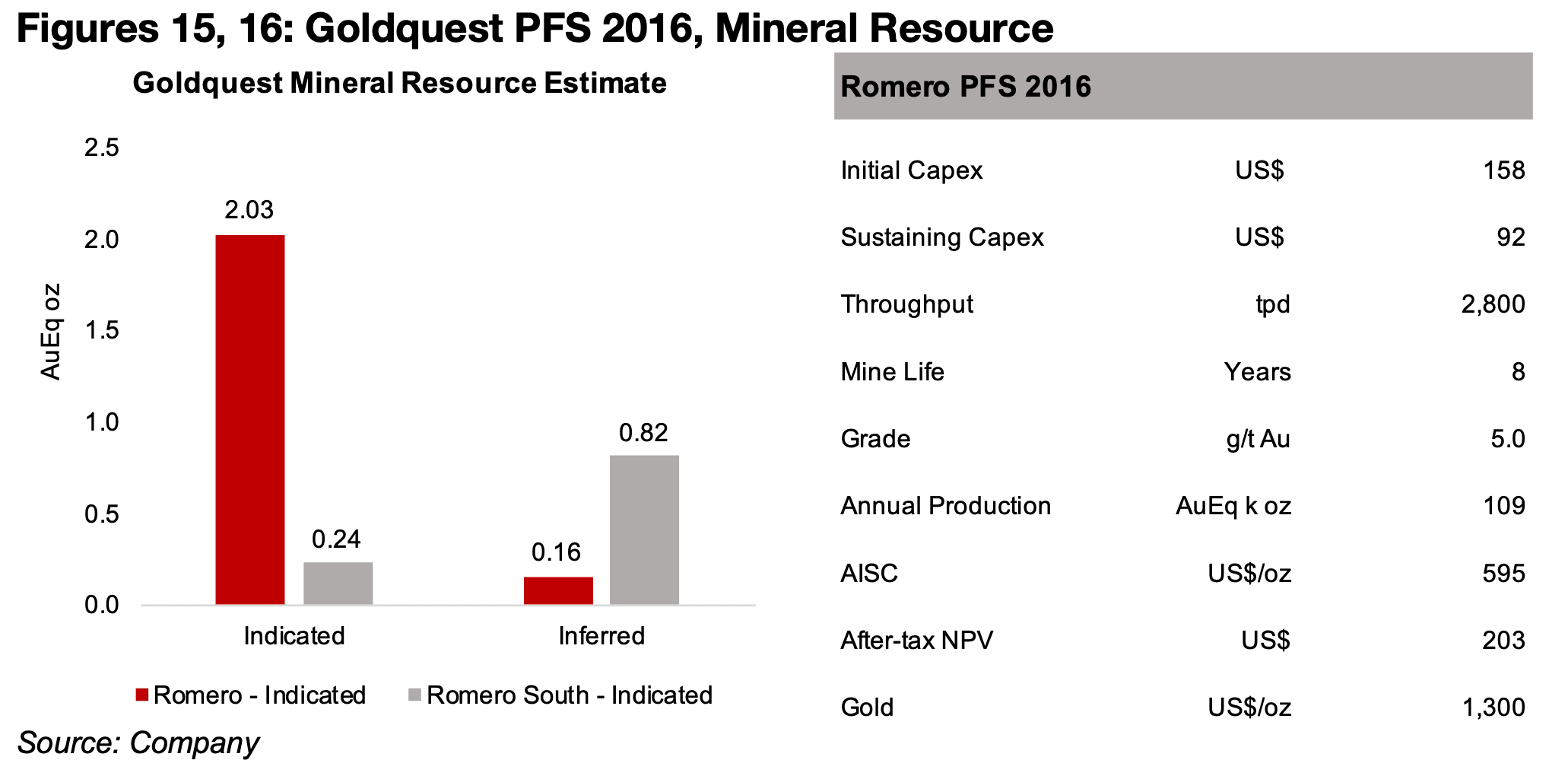

The Romero project has a Mineral Resource Estimate and PFS, but both are from 2016 and therefore significantly dated, and if the company is able to once again proceed, both would see major updates. The current mineral outlines a total 3.2mn oz AuEq, with 2.3mn oz Indicated and 0.9 mn oz Inferred (Figure 15). The PFS shows a high grade of 5.0 AuEq and annual production of 109 oz Au per year for 8 years (Figure 16). The NPV will not reflect the current economics of the project, given cost estimates that are ten years old which will have changed significantly with inflation and a gold price assumption of US$1,300/oz, far below the recent average.

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.

Author

Ben McGregor authors the Weekly Roundup at CanadianMiningReport.com, providing sharp analysis of the metals and mining sector. With a talent for spotting trends, Ben distills complex market shifts into clear, engaging insights on TSXV junior miners. His weekly updates cover gold, copper, uranium, and more, blending data-driven perspectives with a knack for identifying opportunities. A vital resource for investors, Ben’s work navigates the dynamic junior mining landscape with precision.