April 13, 2026

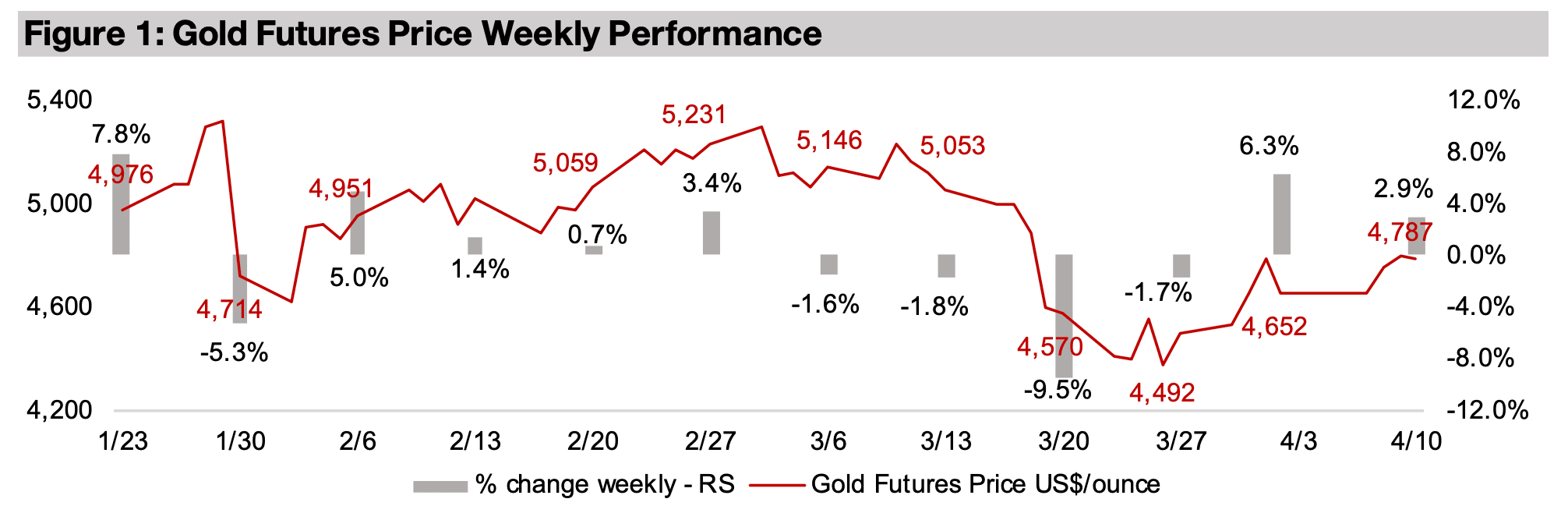

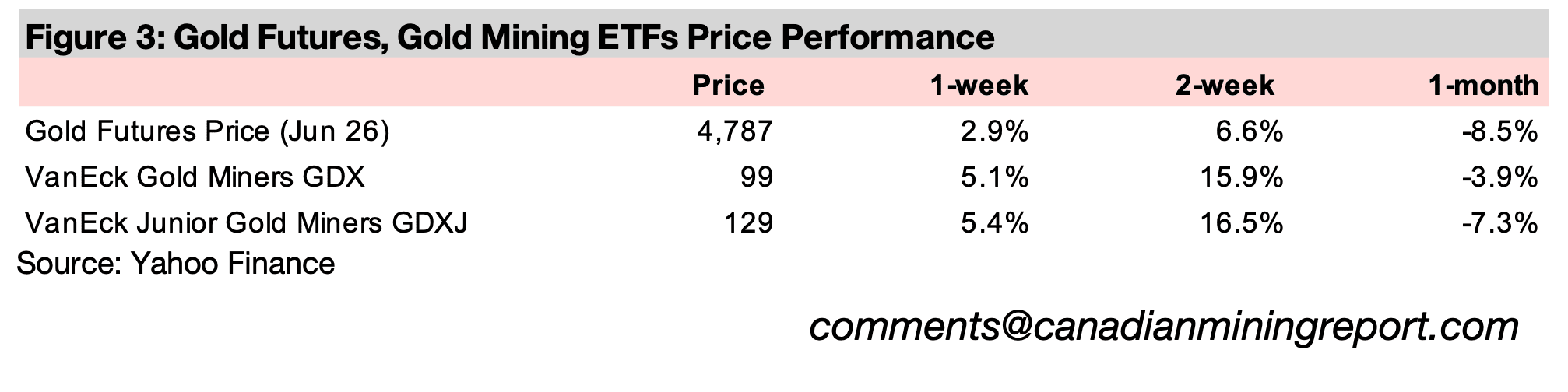

Gold rose 2.9% to US$4,787/oz, recovering for a second week from a historical plunge, as the conflict in the Middle East continued and markets may be pricing in higher geopolitical risk and the potential for stagflation on the oil price spike.

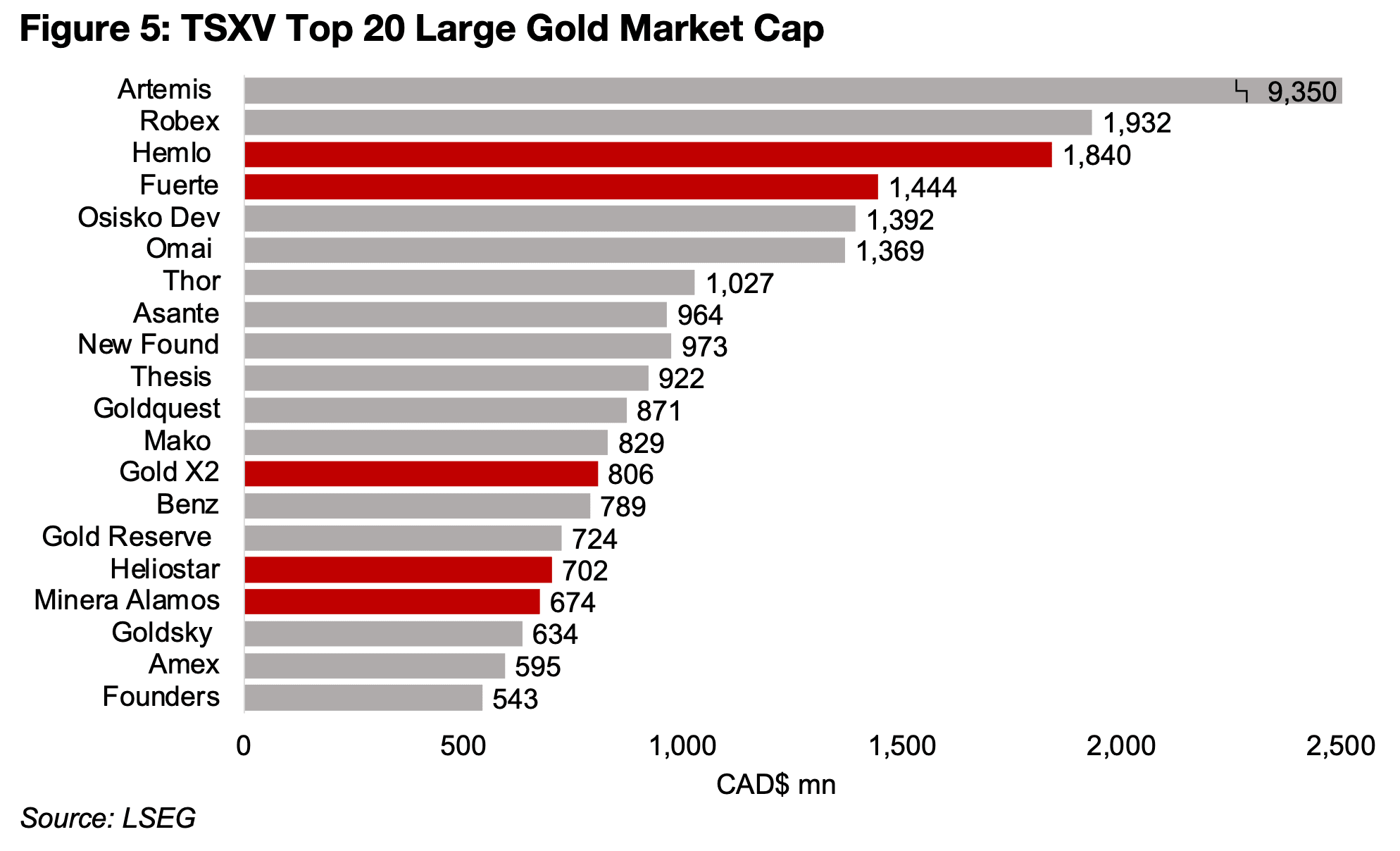

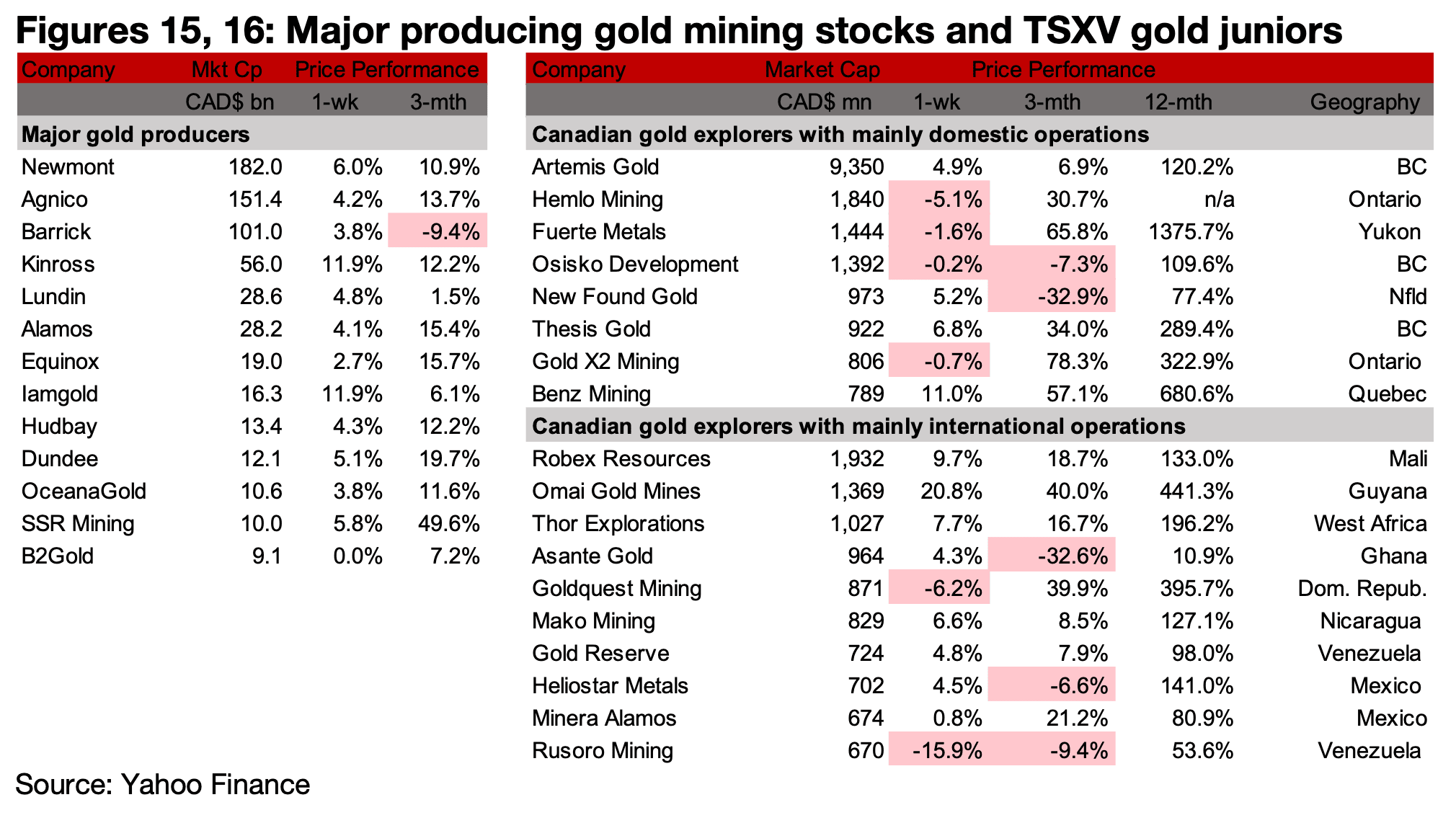

Of five new entrants to TSXV large cap gold, three, Hemlo, Fuerte and Goldsky, have taken over projects from the majors Barrick, Newmont and Agnico Eagle, respectively, with the other two, Heliostar and Gold X2, in production and at the PEA stage.

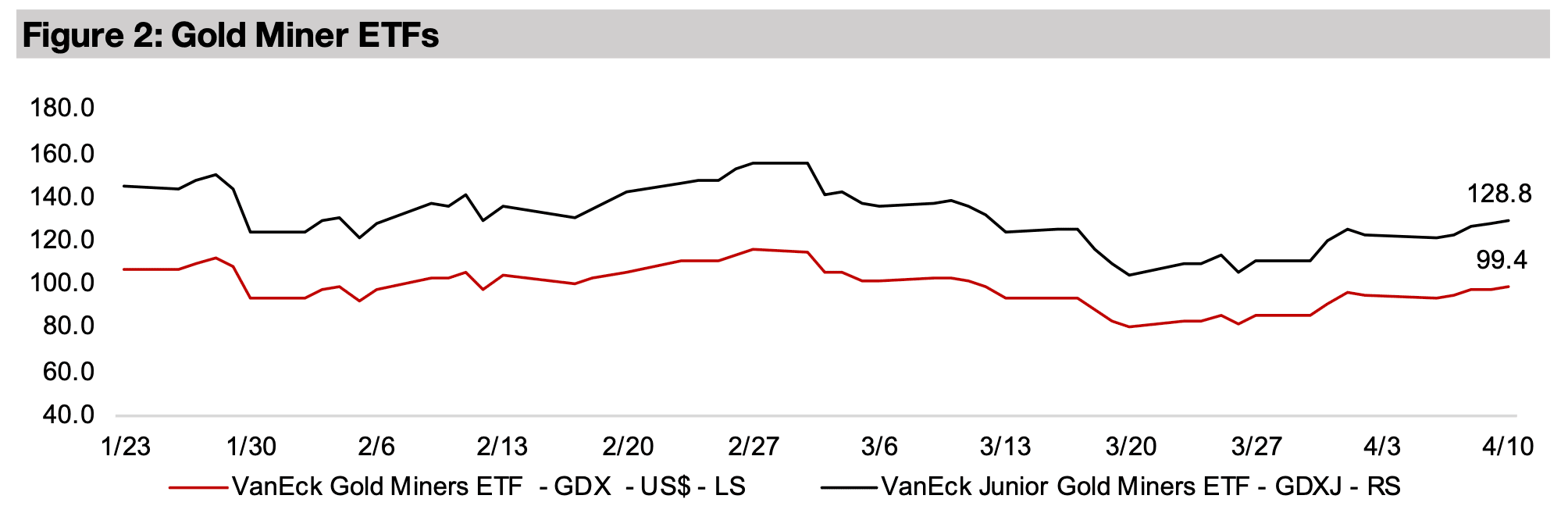

The gold stocks rose for a third week with the GDX up 5.1% and GDXJ gaining 5.4% on the recovery in metals and equities, with the S&P 500 adding 3.5%, the Nasdaq up 4.4% and Russell rising 4.1%, with all three only about -1.0% below pre-war levels.

The gold price rose 2.9% to US$4,787/oz, gaining for a second week and up nearly

US$300/oz from the lows around US$4,500, after a huge drop from a peak over

US$5,200/oz in late February 2026. The main catalyst for the plunge had been a

hawkish outlook from the Fed at its March 2026 meeting on inflation concerns

following the surge in oil on the Middle East conflict. However, there had also been

rising speculative interest in the mining sector overall, but especially for precious

metals, from late 2025, that likely reversed in the crash. Some forced selling as

leveraged bets on the sector were unwound may have driven the metal below levels

warranted by the fundamentals, and with speculators cleared out to a degree, and

long-term buyers may have seen the slump as an opportunity to accumulate the metal.

While the rising oil price could drive up inflation, this does not necessarily mean that

central banks will have significant scope to hike rates, as the increased costs across

most industries caused by this key input could curb economic growth, driving

stagflation. Central banks could then be stuck between pressures to hikes rates to

curb inflation, but also to cut them to boost economic growth. The net effect could

be flat interest rates, which would not be a huge driver for gold in either direction.

Also, in the recent decline there does not seem to have been much of a premium

priced in for the heightened geopolitical risk from the Middle East conflict, as the

market may have been expecting a quick conclusion to the conflict. However, which

such a scenario looking increasingly unlikely over the past few weeks, some of the

gain over the past two weeks could be attributed to markets estimating a rising

probability that the issues in the Middle East persist.

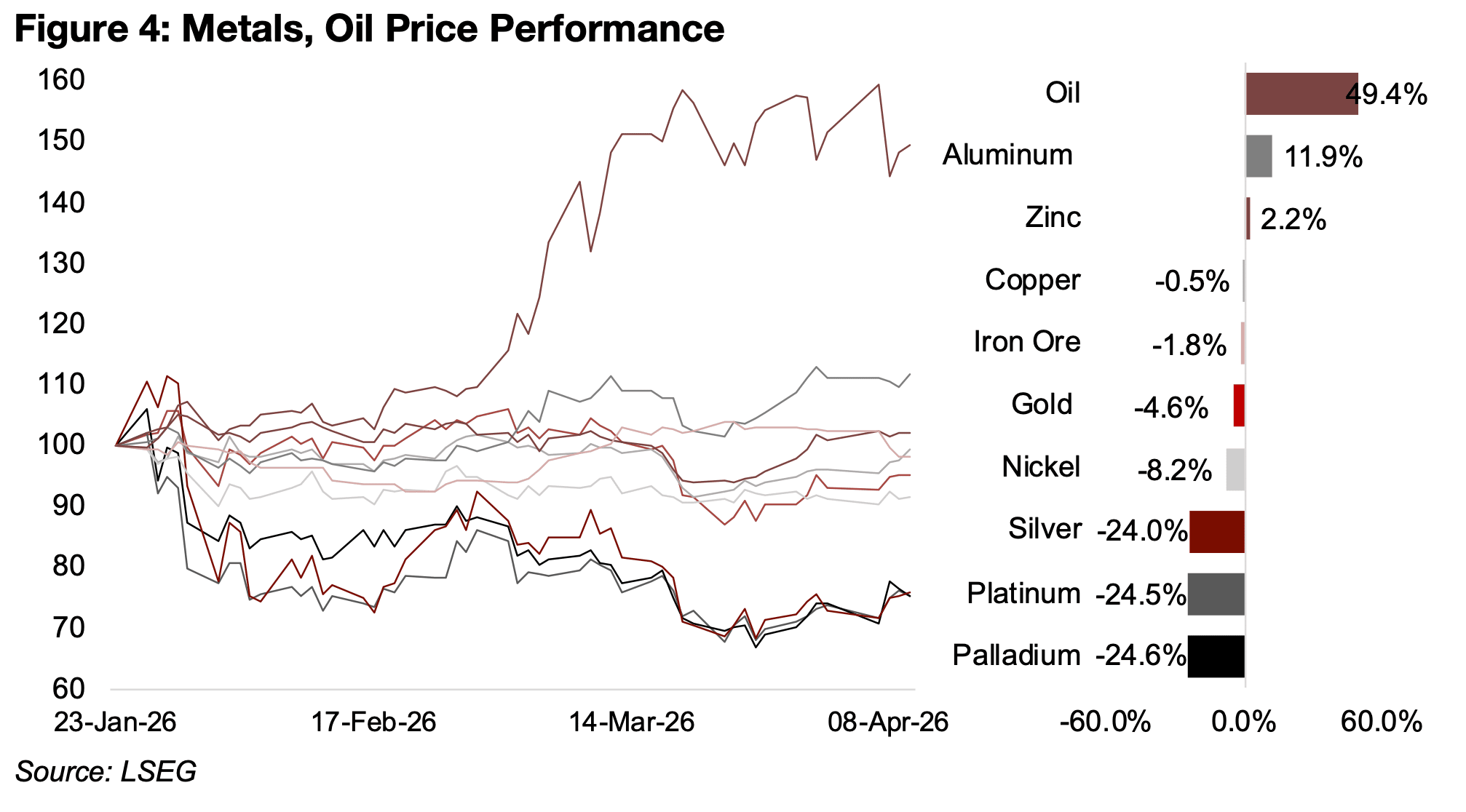

Gold is now down only -4.6% since the start of the last week of January 2026, which

was the highs for the precious metals, far outperforming the crashes in silver,

platinum and palladium of -24% to -25% (Figure 4). This major spread seems mainly

because gold had seen nowhere near the aggressive upward moves of these other

three precious metals. While these other precious metals are driven much more by

industrial factors than gold, which is almost entirely a monetary metal, their drop did

not appear to be based on a decline in economic growth expectations, as other base

metals have held up relatively well.

The copper price is down just -0.5% since late January 2026, iron ore has dropped -

1.8%, and zinc risen 2.2%, with only the heavily oversupplied nickel market down

significantly, by -8.2%. While the aluminum price has jumped 11.9%, this has been

driven by sector specific concerns, with the Middle East a major source of global

supply for the metal at over 5.0% of the total, with some major producing countries

including UAE and Bahrain having been directly attacked in the conflict. However,

even aluminum’s major gains look moderate versus the huge jump in the oil price by

nearly 50%.

The equities markets recovered substantially for a second week, with the S&P 500 up

3.5%, the Nasdaq jumping 4.4% and the Russell 2000 up 4.1%. The three indices

are now down only around 1.0%-2.0% from their late February 2026 levels prior to

the start of the war, having been down between 9.0%-10.0% at their lows at the end

of March 2026. The GDX and GDXJ ETFs of gold producers and juniors also gained

for a second week, up 5.1% and 5.4%, but they are still down -11.3% and -14.3%

from their highs in late January 2026.

There was also a significant gain in silver this week, by 3.8%, which drove up the SIL

ETF of silver producers 4.4%, although the ETF is still down -18.0% from its late

February 2026 highs. The base metals mainly rose, with a 4.5% gain in copper driving

an 8.5% surge in the COPX ETF of copper stocks. Aluminum gained 2.6%, nickel

added 3.0%, which saw the NIKL ETF of nickel stocks rise 3.8%, zinc increased 1.9%

and iron ore was the only major base metal to decline, but by only -1.2%.

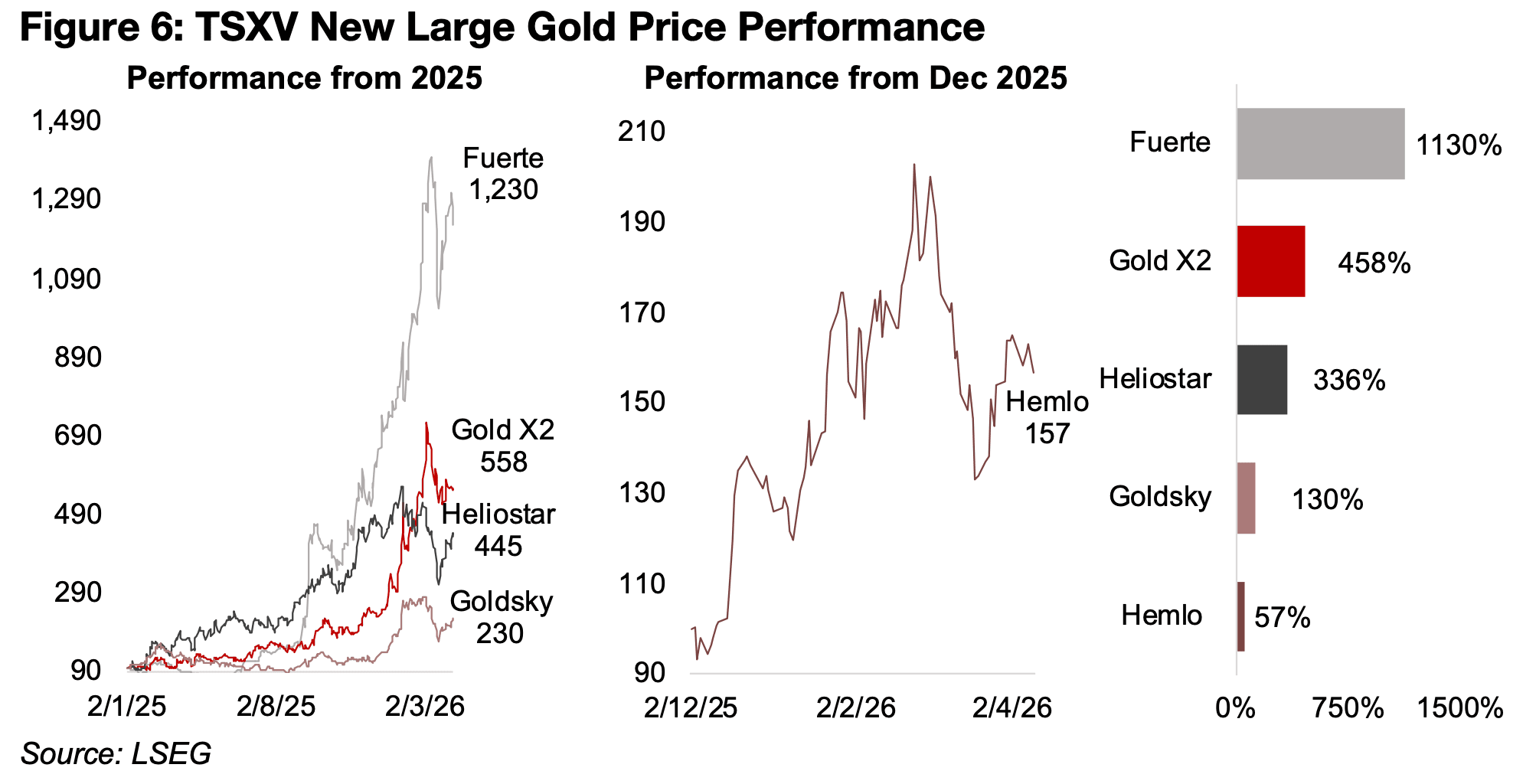

There have been several new entrants to large cap TSXV gold in recent months. Two, Hemlo and Fuerte, have both taken over large projects from majors, which has put them near the top of the ranking, with CAD$1.9bn and CAD$1.8bn market caps the third and fourth largest of the group (Figure 5). Fuerte has seen the largest share price gain of the new entrants by far, up well over 10x in the past year, while Hemlo was only listed at the end of 2025, and has had an over 50% gain since (Figure 6). The other new majors are all mid-caps, with Gold X2 with a market cap of CD$806mn, Heliostar at CAD$702mn and Goldsky at CAD$634mn, with gains of around 450%, 340%, and 130% over the past year.

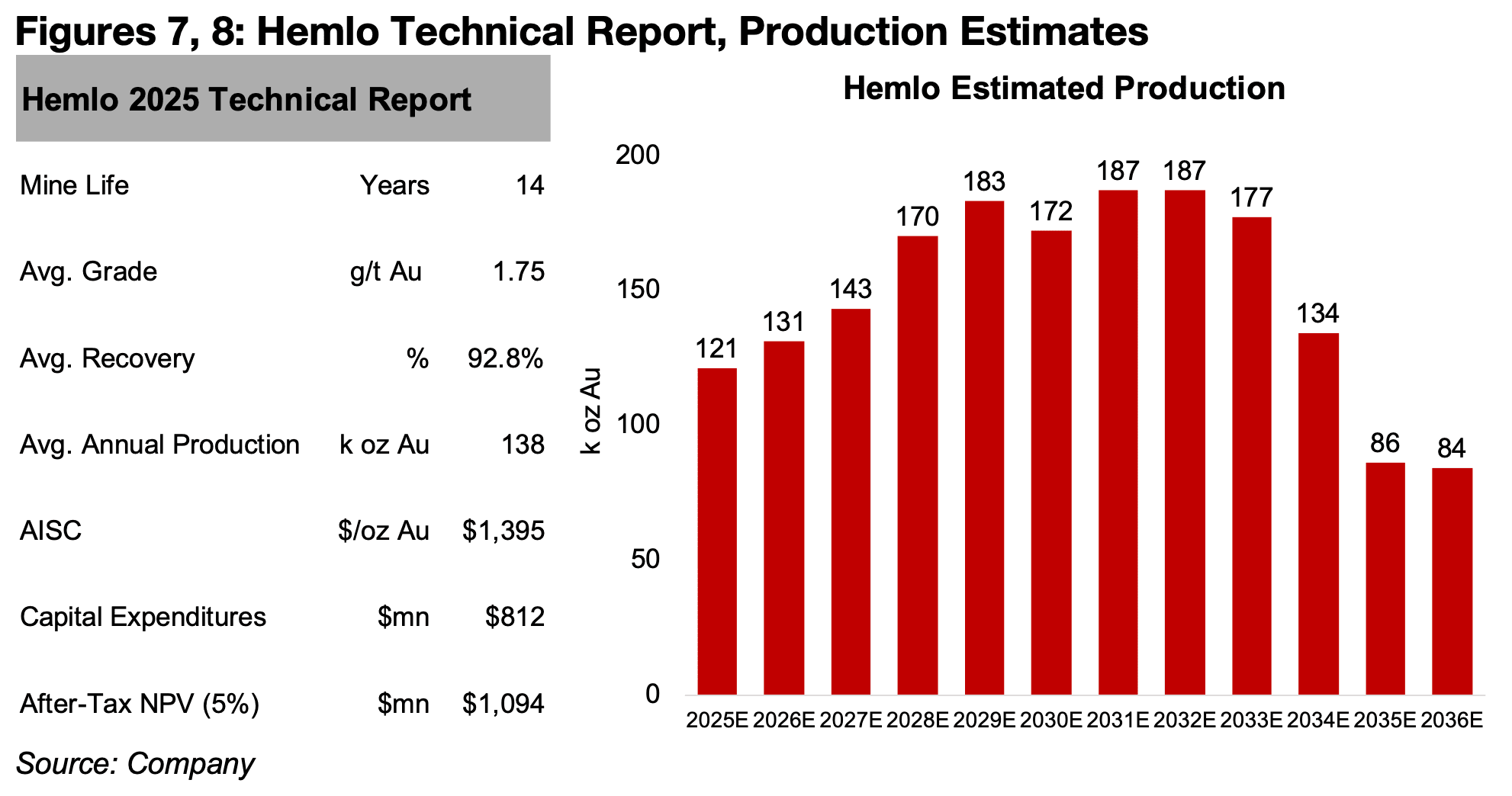

Hemlo is a long producing mine in Ontario, with it the largest mine in the country at

the time of its first gold pour in 1985, and total output of the metal over the decades

at 25mn oz Au. Barrick took full ownership of the mine in 2014, although it had a stake

in the project much earlier, and in November 2025, sold it to the new Hemlo company,

which started trading on December 2, 2025.

The mine is currently targeted to operate for fourteen years, with a grade of 1.75%

and annual production of 138k oz Au at an AISC of $1,395/oz (Figure 7). While the

operation is currently entirely underground mining currently, the company expects to

shift towards a low proportion of open pit from 2028, which will gradually expand

before becoming the entire output by 2035 (Figure 8). Hemlo is also planning further

exploration near the mine to potentially expand the resource and is also identifying

other regional targets. The company sees opportunity for an immediate boost in

output given that its mill is currently operating only at 40% capacity, without

additional costs, with potential for a further boost with additional capex.

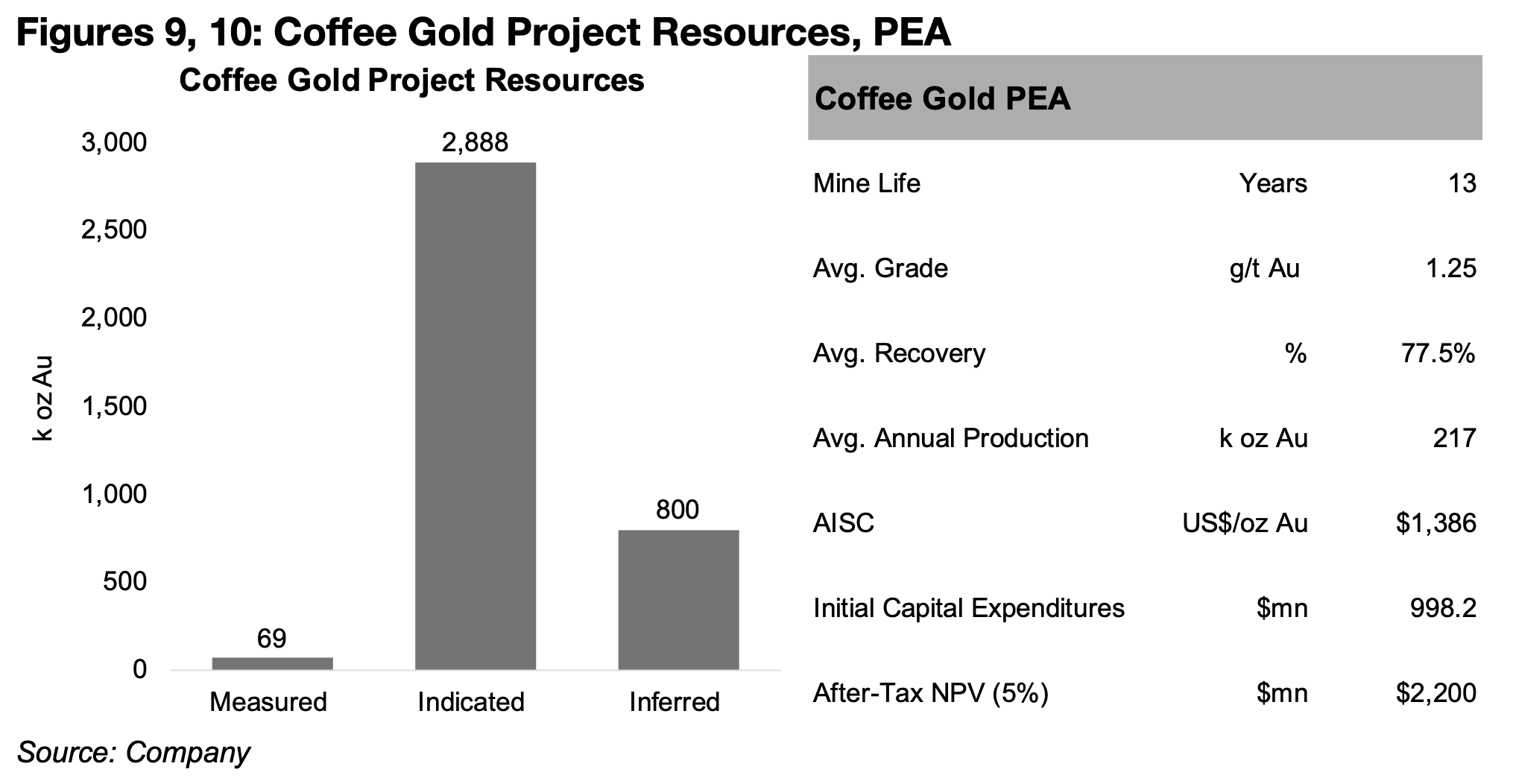

The huge run up in Fuerte’s price started on its announcement that it would acquire

the open pit, heap leach Coffee Gold project in Yukon, similarly to Hemlo, also from

a major, Newmont, on September 15, 2025. Newmont had already advanced the

project considerably with $300mn in investment and feasibility level work has already

been completed. A key environment approval was granted in 2022 and agreements

with local communities have already been in place for several years, and the Yukon

government has major funding available for infrastructure up to $468mn for roads in

areas with active mining and high mineral potential.

The current mineral resource for the project has over 3.0mn oz Au, with most of this

Indicated (Figure 9). The company released its PEA in for the project in Q1/26, with

production of 217k oz Au per annum over thirteen years with a 1.2% grade at an AISC

of $1,386/oz with initial capex of $998.2mn and an after-tax NPV of $2,200mn (Figure

10). The company started 40k metres of resource conversion and exploration drilling

in March 2026, and plans to survey the majority of the 70k hectare property. A

Feasibility Study is currently targeted by Q4/26 to be led by G Mining Services and

further permits for access routes, water use and quartz mining are expected by H2/26.

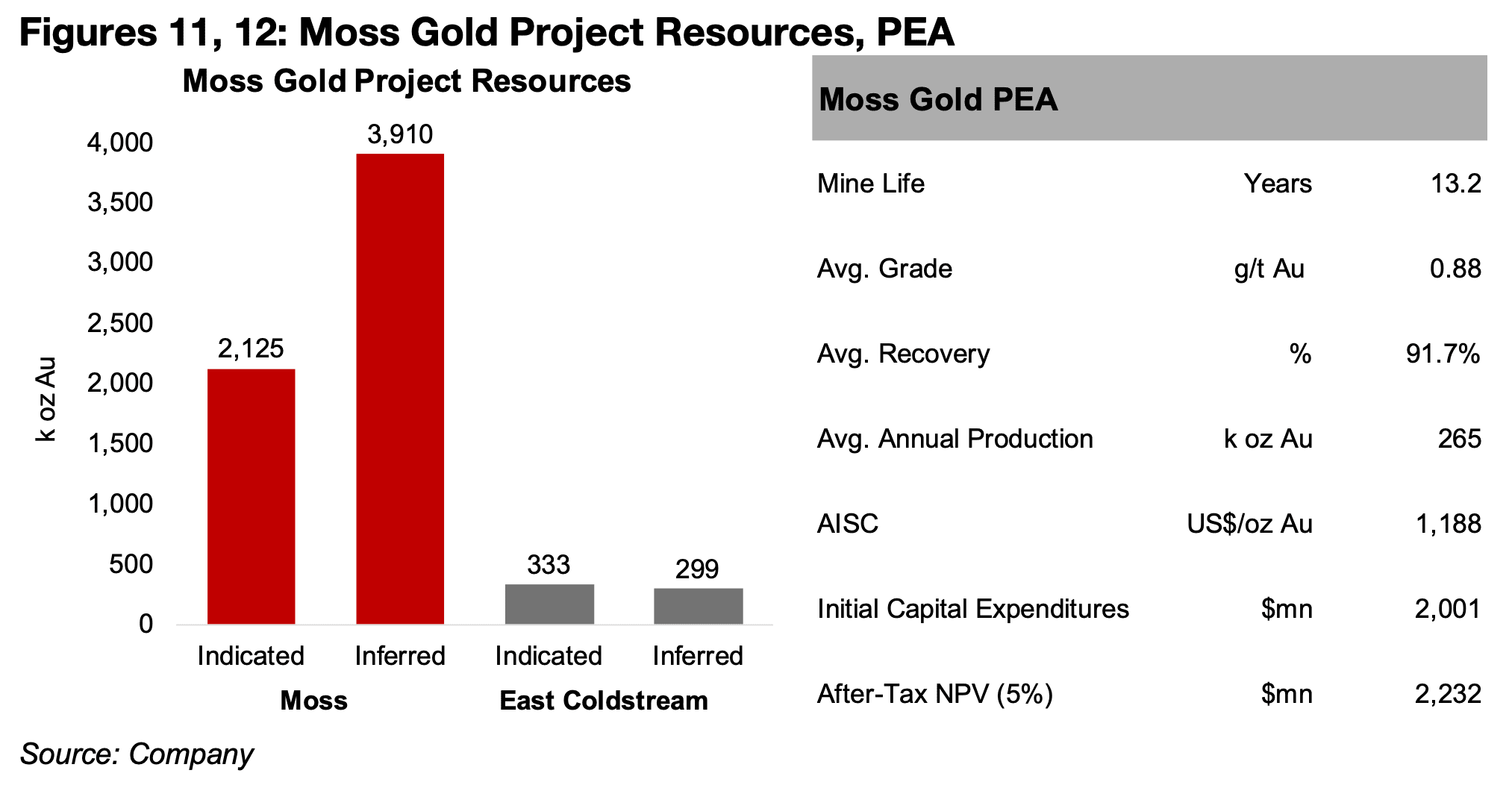

The new mid-cap TSXV gold producers are at different development stages, with Gold X2 at the PEA stage for its Moss Gold project in Ontario, Heliostar already in production at two mines, La Colorada and San Augustin in Mexico, and Goldsky is still in the exploration phase of the Barsele project in Sweden. The Moss Gold project has a large mineral resource estimate for a junior of over 6.0 mn oz Au, although only around 2.0mn oz are Indicated, with 4.0 mn Inferred, and the company just released its PEA for the project in March 2026 (Figures 11, 12).

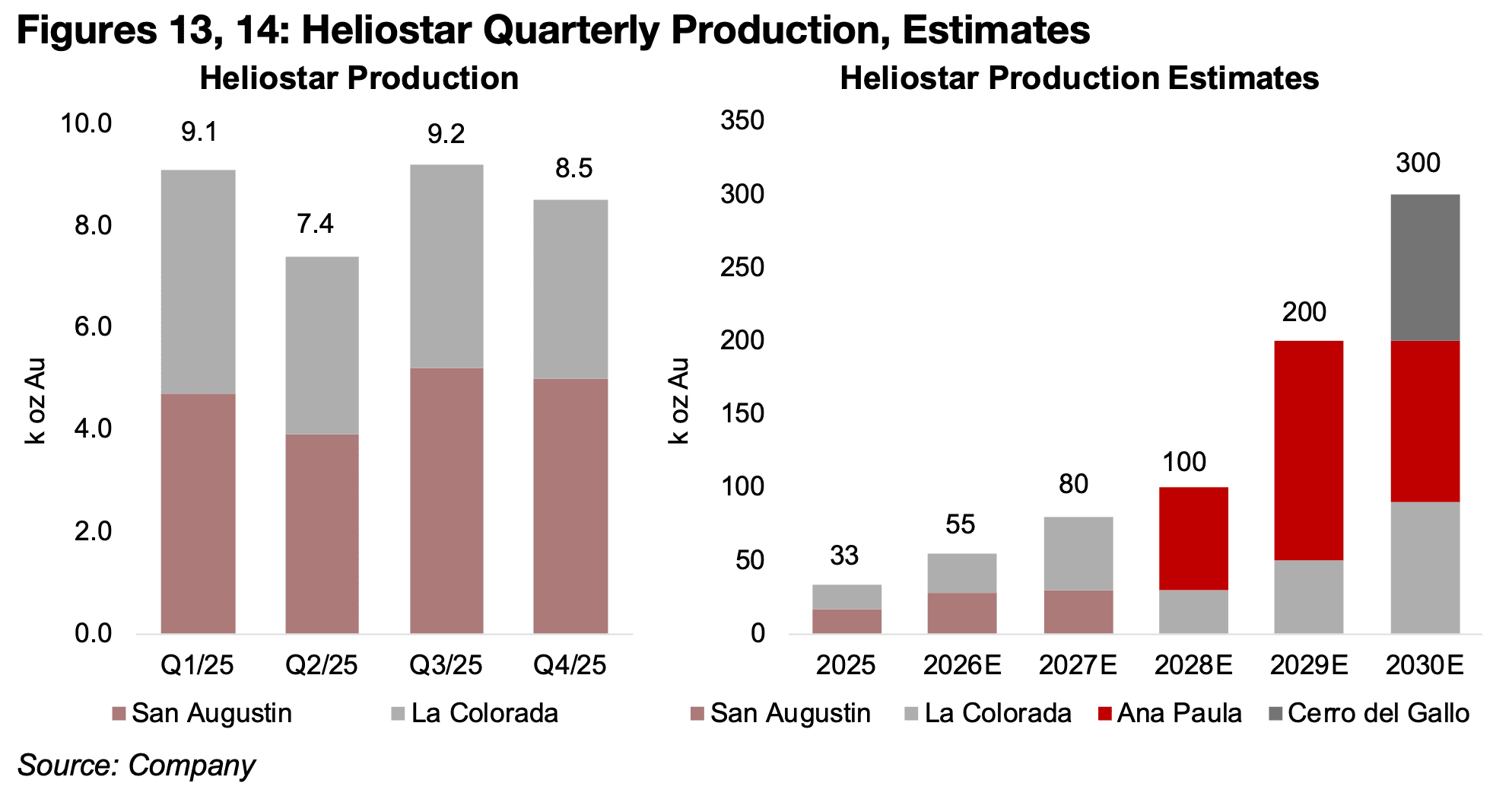

Heliostar estimates a major increase in production over the next two years, from 33k oz in 2025 to 55k oz in 2026E and 80k oz by 2027E, with a major shift in production to the Ana Paula mine by 2028E, driving a rise to 100k oz Au (Figures 13, 14). Goldsky was formed in H2/25 through the merger of First Nordic Metals and Mawson Finland and purchased Agnico Eagle’s 55% of Barsele in January 2026. Agnico Eagle has continued to invest in the project, taking a 32.5% stake in Goldsky, after significant exploration at the project from 2015-2025 with 174.5k m drilled.

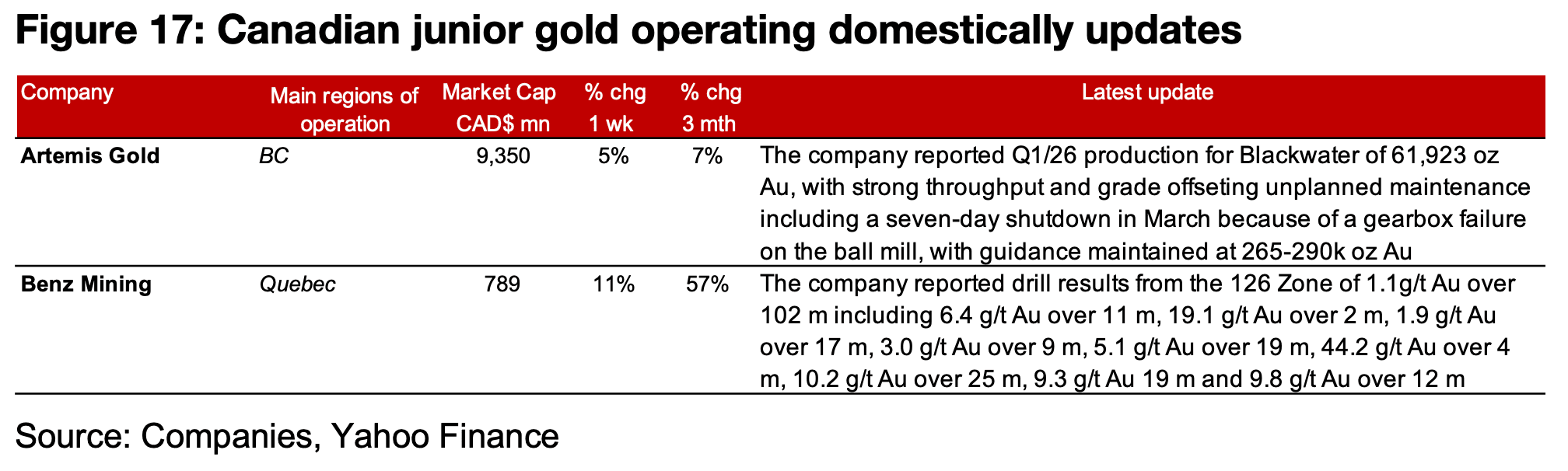

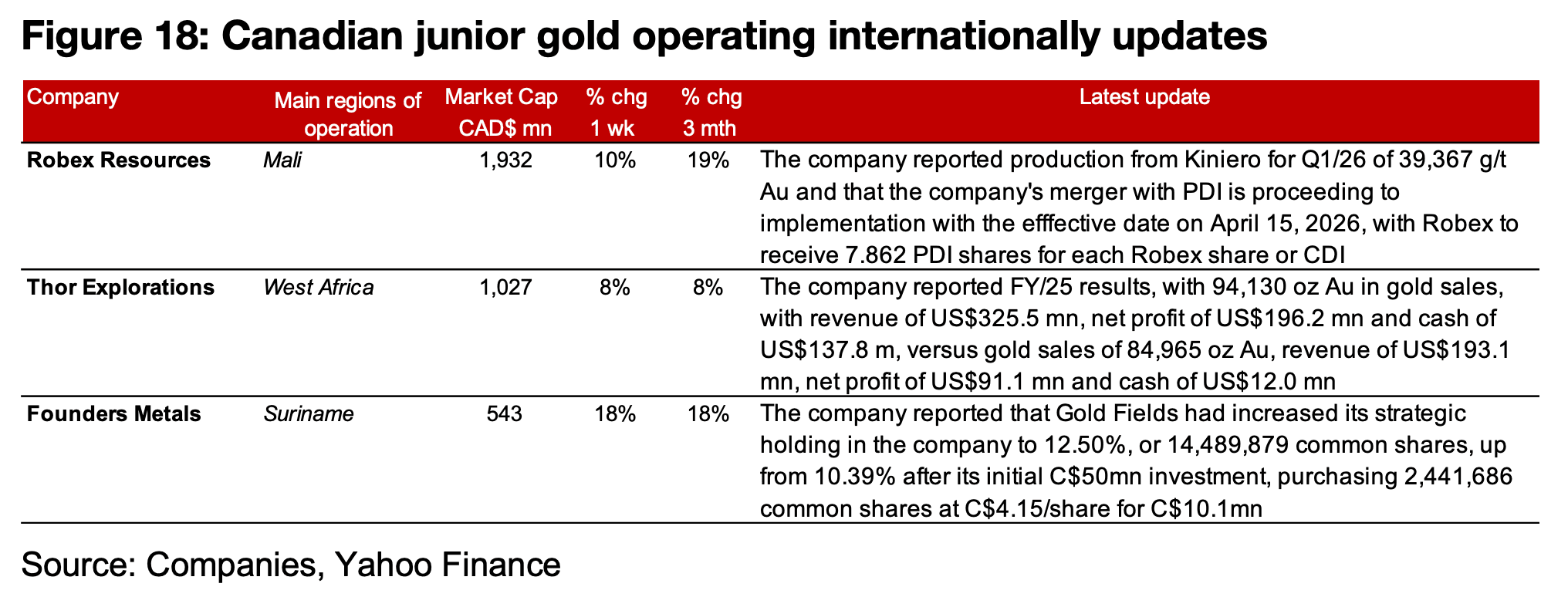

The major producers all rose for a second week and TSXV gold was mixed (Figures 15, 16). For the TSXV gold companies operating mainly domestically, Artemis reported Q1/26 production from Blackwater, with strong processing and grade offsetting a week of shutdown for maintenance, and Benz Mining announced drill results from the 126 Zone of Hurricane (Figure 17). For the TSXV gold companies operating mainly internationally, Robex reported Q1/26 production from Kiniero and that its merger with Predictive Discovery is proceeding to implementation. The merger had all conditions satisfied on April 8, 2026 and is expected to be completed by April 15, 2026, with the company to be listed in Australia and Toronto and the ticker to be PDI. The company reported a suspension from quotation on the ASX with the last trading day on April 10, 2026. Thor Exploration announced Q4/25 results and Founders reported that Gold Fields had increased it strategic shareholding in the company from 10.4% to 12.5% (Figure 18).

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.

Author

Ben McGregor authors the Weekly Roundup at CanadianMiningReport.com, providing sharp analysis of the metals and mining sector. With a talent for spotting trends, Ben distills complex market shifts into clear, engaging insights on TSXV junior miners. His weekly updates cover gold, copper, uranium, and more, blending data-driven perspectives with a knack for identifying opportunities. A vital resource for investors, Ben’s work navigates the dynamic junior mining landscape with precision.