July 07, 2026

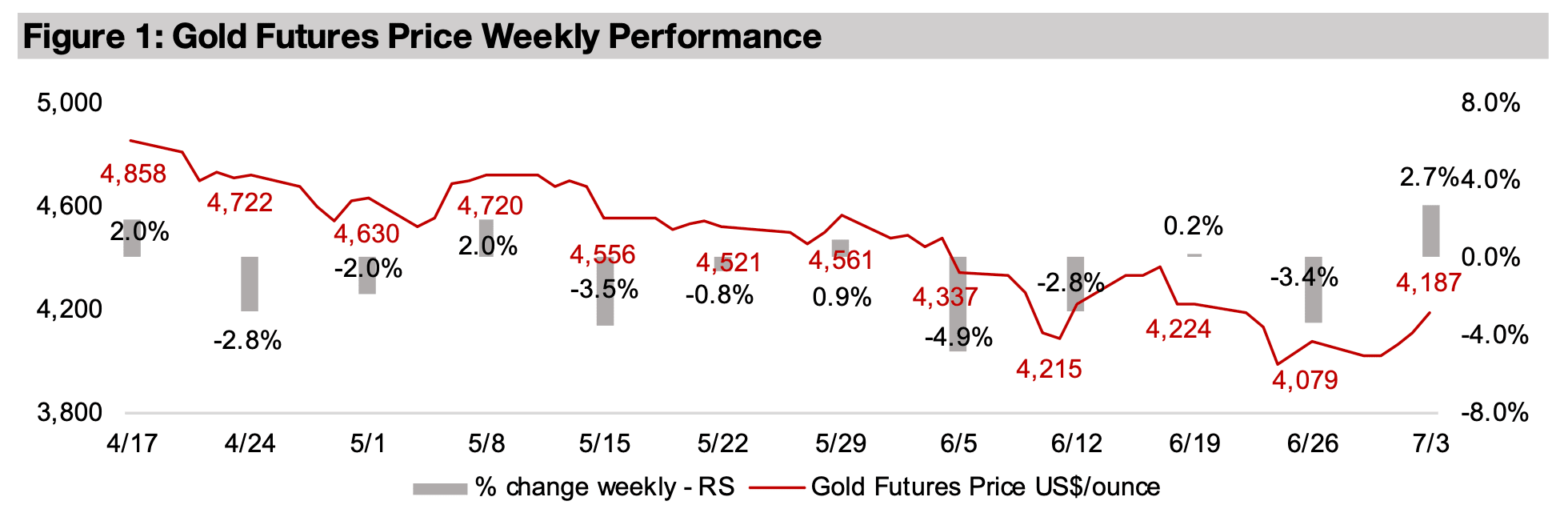

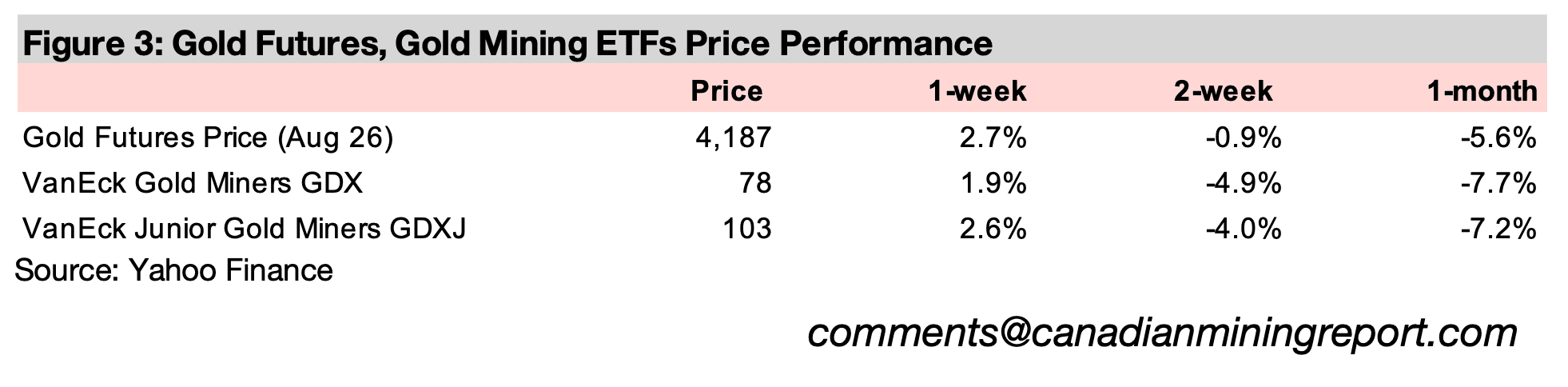

Gold rose 2.7% to US$4,187/oz as relatively weak US jobs data decreased expectations for the potential rate hike this year, which drove down the US$ and yields, although the latter had recovered by the end of the week.

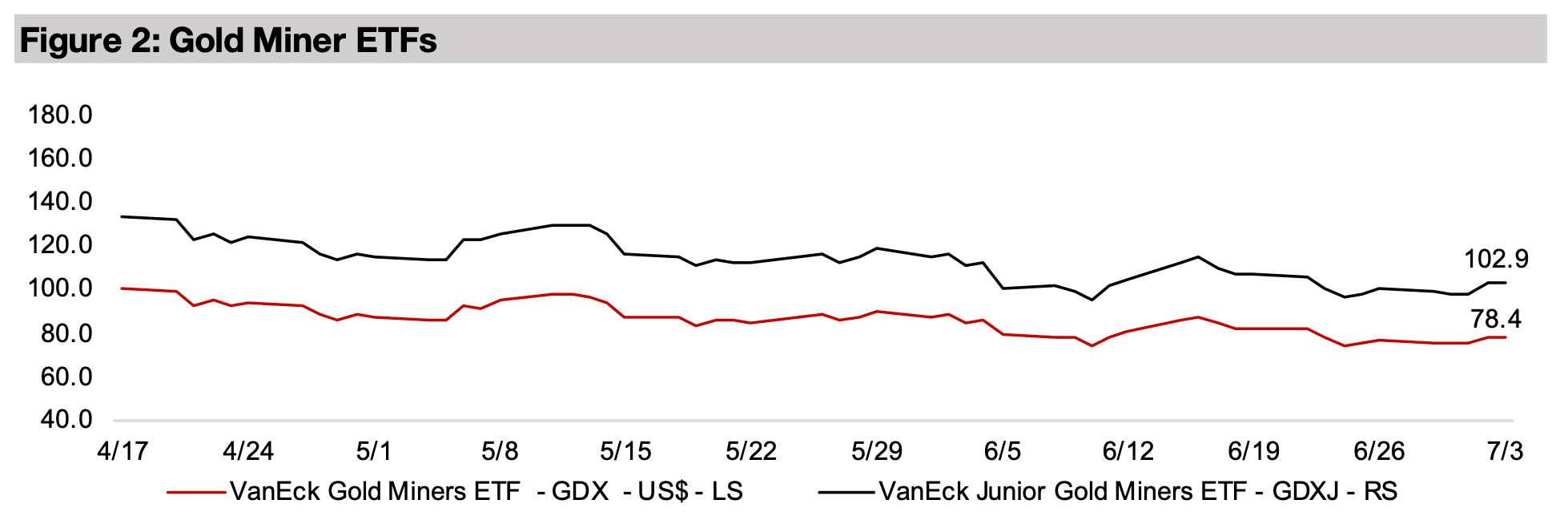

The gold stocks rebounded from near the lows for the year, with the GDX up 1.9% and GDXJ gaining 2.6%, as the metal and large cap equities rebounded, with the S&P up 2.3%, the Nasdaq jumping 2.9%, but the Russell 2000 lagging, up just 0.2%.

The gold rose 2.7% to US$4,187/oz as US jobs came in relatively weak for June 2026,

leading markets to ease off on rate hike expectations that had been driven by recently

very strong employment figures. While this drove a decline in the US$ as would be

expected, an initial drop in the 10-year bond yield was actually reversed by the end

of the week, with it eventually making gains. Even the moderate rise in the potential

that a widely expected rate hike this year could be avoided boosted large cap equity

markets, with the S&P 500 up 2.3% and Nasdaq gaining 2.9%. However, the Russell

2000 small cap index, which outperformed large caps in recent weeks, was near flat,

up just 0.2%, and gold stocks rose with the GDX up 1.9% and GDXJ gaining 2.6%.

The first major US employment report was ADP payrolls for June 2026, which rose

98,000, seasonally adjusted, declining moderately from 122,000 in May 2026 and not

significantly below consensus expectations 110,000. However, US non-farm payrolls

for June 2026 looked weaker, increasing by 57,000, only around half the 129,000 in

May 2026 and considerably below consensus estimates for 115,000. While the US

unemployment rate did decline to 4.2% on the increase in the jobs, it was also partly

driven by a drop in the participation rate of labor.

The biggest single driver in the metals space that could be coming even as early as

this week is the US decision on copper tariffs. The US Department of Commerce

submitted its report on the issue on the June 30, 2026 target date, and this is now

being reviewed by the government. The US tariff issues initially started causing

disruption to the global copper market from early 2025 as the new administration

implemented large new tariffs across many industries. Copper specifically became a

target in February 2025, when the government signed an Executive Order for the US

Department of Commerce to investigate the potential national security risks of copper

imports, with the possibility of imposing tariffs on all products in the sector.

There was an initial conclusion from the Department of Commerce submitted to the

government on June 30, 2025, with recommendations for no immediate tariffs on

refined copper, but 50% on semi-finished and 25% on copper derivatives. With

refined copper imports at US$8.7bn in 2024, this saw exactly half of the US$17.4bn

in total imports of the metal come under significant tariffs. The upcoming decision

could affect refined copper imports, with the potential for tariffs of 15% to be imposed

by January, 2027, which could rise to 30% by 2028. If the government decides to

move ahead, it would see all US copper imports facing substantial tariffs.

This contrasts with prior to 2025, when copper imports faced marginal tariffs below

5.0%, and overall they have been around these low levels for the last century, except

during the Great Depression. This shows the major historical significance of the tariffs

imposed on copper last year as well the upcoming decision.

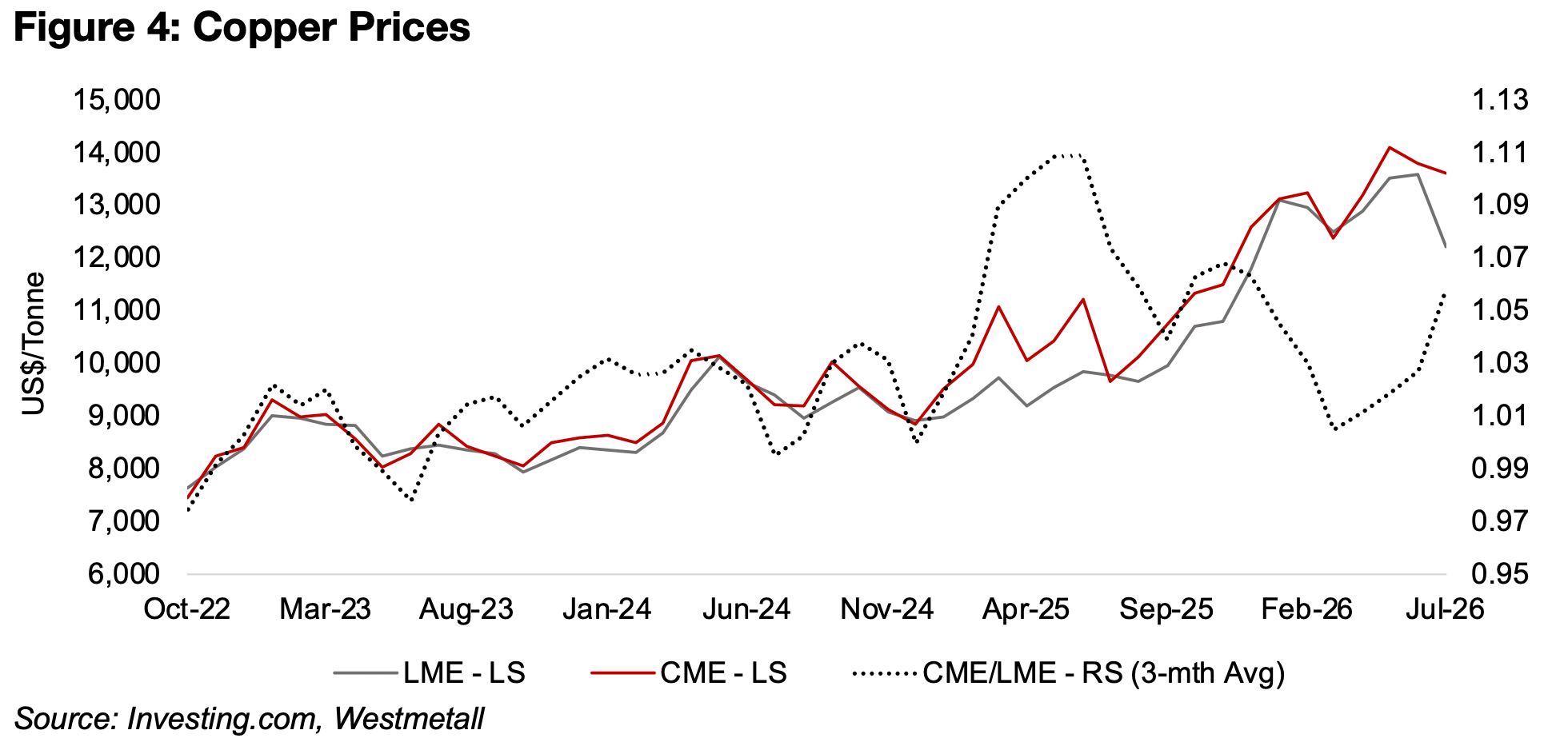

These tariffs issues have caused a major distortion in the relative prices of copper

between the US CME and the UK LME, with the two usually only diverging by around

1.0%-2.0%, but the spread jumping to near 30% in July 2025 just before the July 30,

2025 announcement of tariffs (Figure 4). For the full month of June 2025, the spread

averaged around 14%, and while it trended down in the following months, it was not

back to the historical average around 1.0% until the first four months of 2026.

However, the spread has again started to rise over the past three months, and is now

at 11%, not as high as its peak last year, but still quite elevated.

This has driven a major shift away from the average inventory balances between the

US, UK and China, which from 2014 to 2024 were 21%, 51% and 28% of the total,

respectively. The expectations of US tariffs saw huge flows into the country and

stocking up of inventories, with supply especially from the UK, which in turn

restocked copper by making purchases from China, which then also saw its copper

holdings drop. At the peak last year in June 2025, inventories were 55%, 24% and

21% in the US, UK and China, but total inventories were at just 384,315k tonnes

across the three regions.

This broader trend of a shift in copper inventories towards the US and away from the

UK and China has continued over the past year. Global copper inventories overall

have continued to surge in absolute terms in all three countries, reaching 1,143,648

as of June 2026, with the US and UK shares rising to 59% and UK 29% and China’s

share declining to just 11%. If there is eventually an overall rebalancing of this

situation, with inventories heavily flowing back to China from the UK and from the US

to the UK, there could potentially be quite extreme moves in the copper market still

to come from technical movements alone, apart from other broader underlying

macroeconomic factors driving the metal.

The copper price could see large moves either way based on the US tariff decision.

If major tariffs are imposed, the extreme imbalance in global inventories could worsen,

with flows towards the US likely driving up the copper price in the country. However,

with China inventories down to just 11% of the total, it could near a limit on how much

can be sold to the UK to offset flows to the US, although this could just lead to UK

inventories being depleted. If there is a decision for only moderate, or even no, major

new tariffs, it could potentially prompt a dramatic unwinding of this historical

imbalance of global copper inventories.

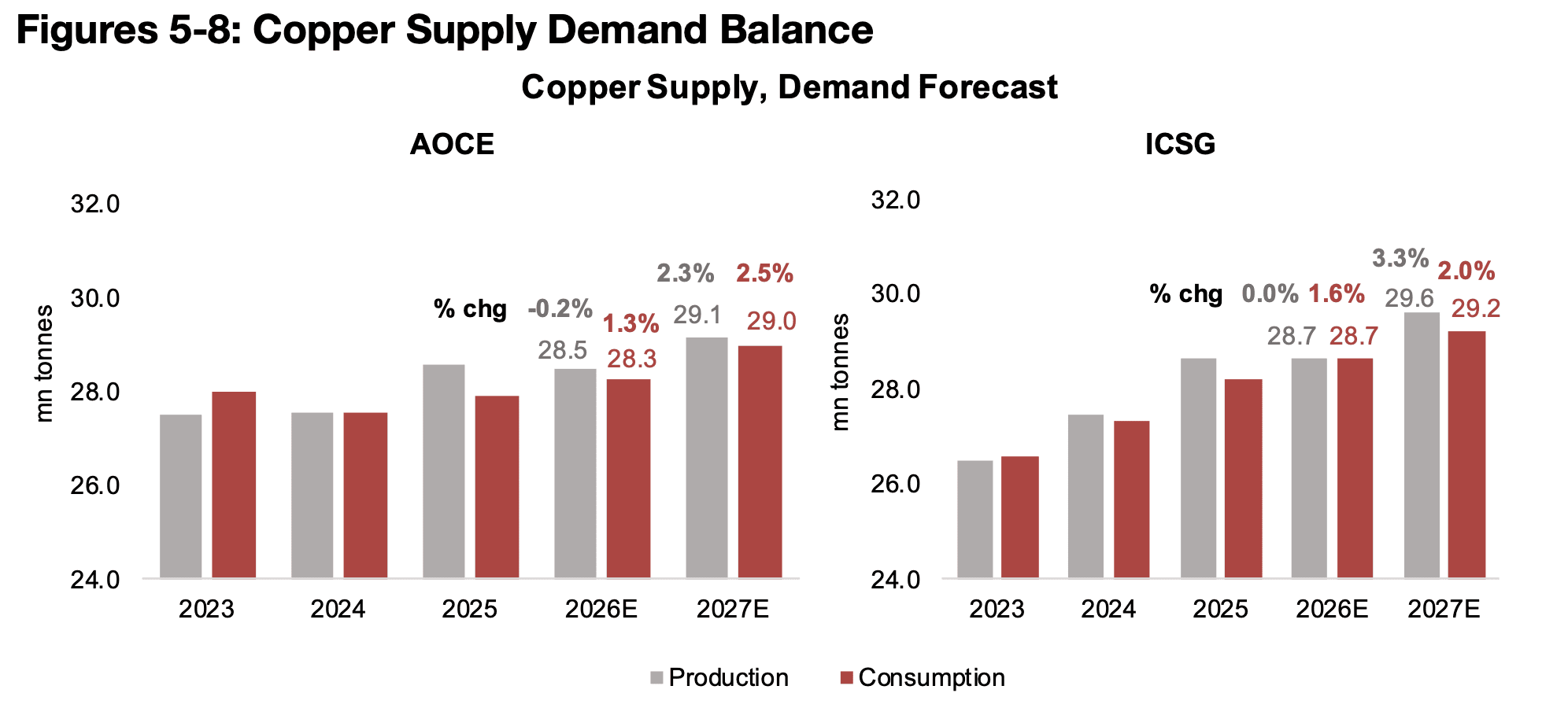

While there could therefore be major volatility in copper short-term, the outlook for the next two years looks relatively bearish based the forecasts from Australia’s Office of the Chief Economist (AOCE) and the International Copper Study Group (ICSG).

The AOCE has finally released new estimates in its June 2026 reported after the

regular March report was skipped, with the institution indicating the difficulty of

forecasting given the sudden disruption at the time to resource markets from the war

in the Middle East. The ICSG forecasts are also relatively recent, having been released

in April 2026 and therefore also incorporate the effects of the war and some major

declines in the global copper supply over the past year.

The AOCE and ICSG both forecast near flat production growth for 2026E, of -0.2%

and 0.0%, respectively (Figures 5, 6), outpaced by similar consumption growth of 1.3%

and 1.6%. However, given slightly different base figures in 2025, the AOCE forecast

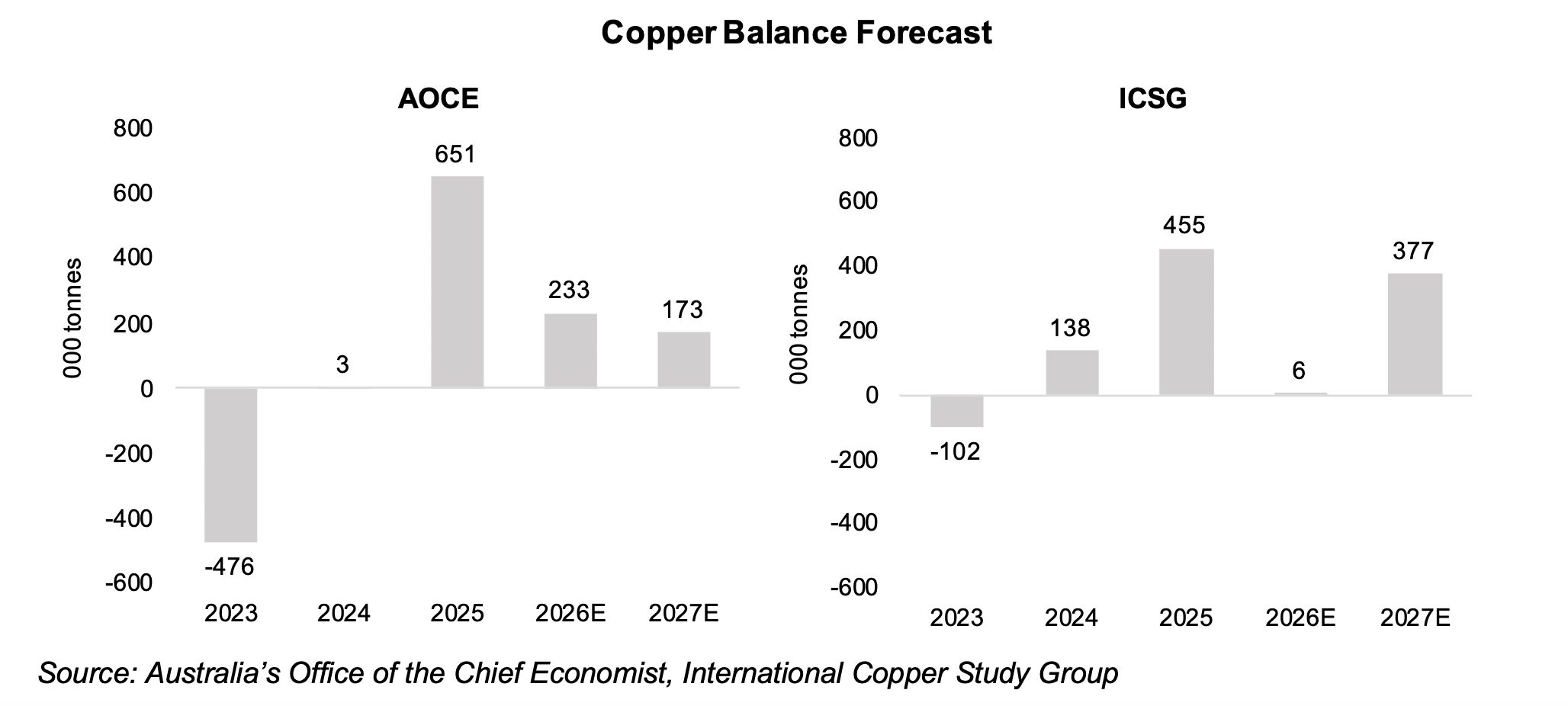

leads to a significant surplus of 233k tonnes, and the ICSG a nearly balanced market,

with a small 6k tonne surplus (Figures 7, 8). However, both expect production growth

to rebound substantially in 2027E, to 2.3% and 3.3%, respectively, with consumption

growth of 2.5% and 2.0%. This drives a substantial surplus for both, although for the

AOCE it declines from 2026E to 133k tonnes, and for the ICSG it jumps to 377k

tonnes.

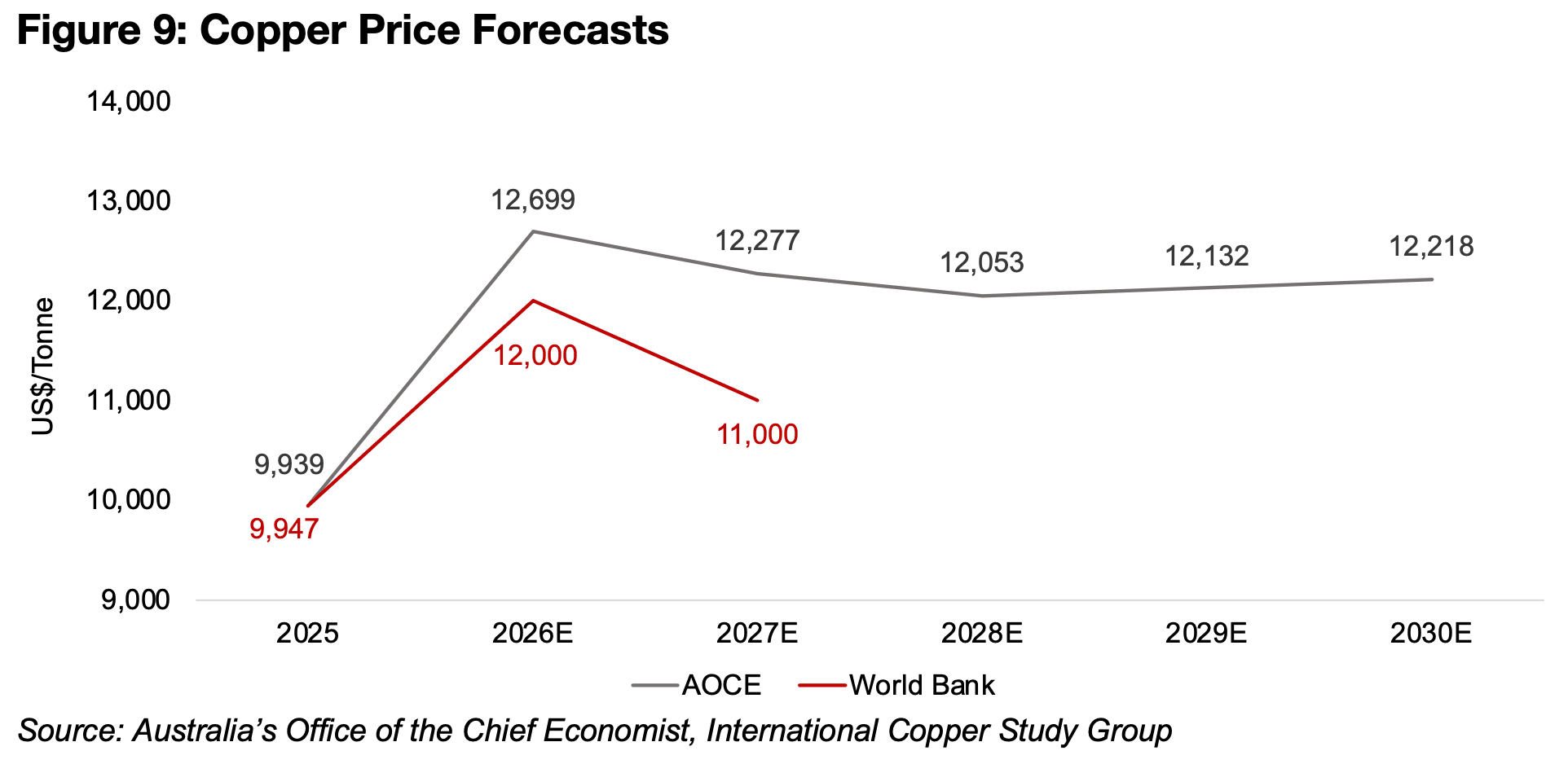

Only the AOCE has copper price forecasts, out to 2031E, with the ICSG not directly

providing estimates (Figure 9). However, the World Bank does provide regular

estimates for metals prices, including copper, but no full supply and demand

numbers, which allows for a comparison with the AOCE figures. While the World Bank

forecasts are also recent, from April 2026, they only extend out only to 2027E. Both

of the sources are expecting copper prices to peak this year, with the AOCE at

US$12,699/tonne and the World Bank at US$12,000/tonne, with a decline to

US$12,777/tonne and US$11,000/tonne, respectively, by 2027E. The AOCE expects

the copper price to continue the decline through to US$12,053/tonne in 2028E, and

then recovery moderately in 2029E and 2030E to US$12,218/tonne, still significantly

below the 2027E peak.

This contrast significantly with some major investment banks, which are forecasting

a potential jump to US$15,000/tonne over the next year, although many do have a

base case of US$12,000/tonne, which would be inline with the World Bank estimate.

The lowest estimate is US$9,500/tonne, which is an outlier, with the next lowest

estimate at US$11,000/tonne, and would effectively see a reversion of the price to

around 2026E levels. The thesis for the low figure is that the currently high prices are

driven mainly by the tariff related distortions, and as these eventually unwind as there

is more clarity on situation, that the price could also decline substantially.

In addition to the tariff related disruptions, the copper price seems to have been

driven recently especially by very bullish expectations for the demand side related to

the tech boom and AI. However, there are growing market concerns over the

sustainability of the growth in this sector, and a slowdown could be a drag on copper.

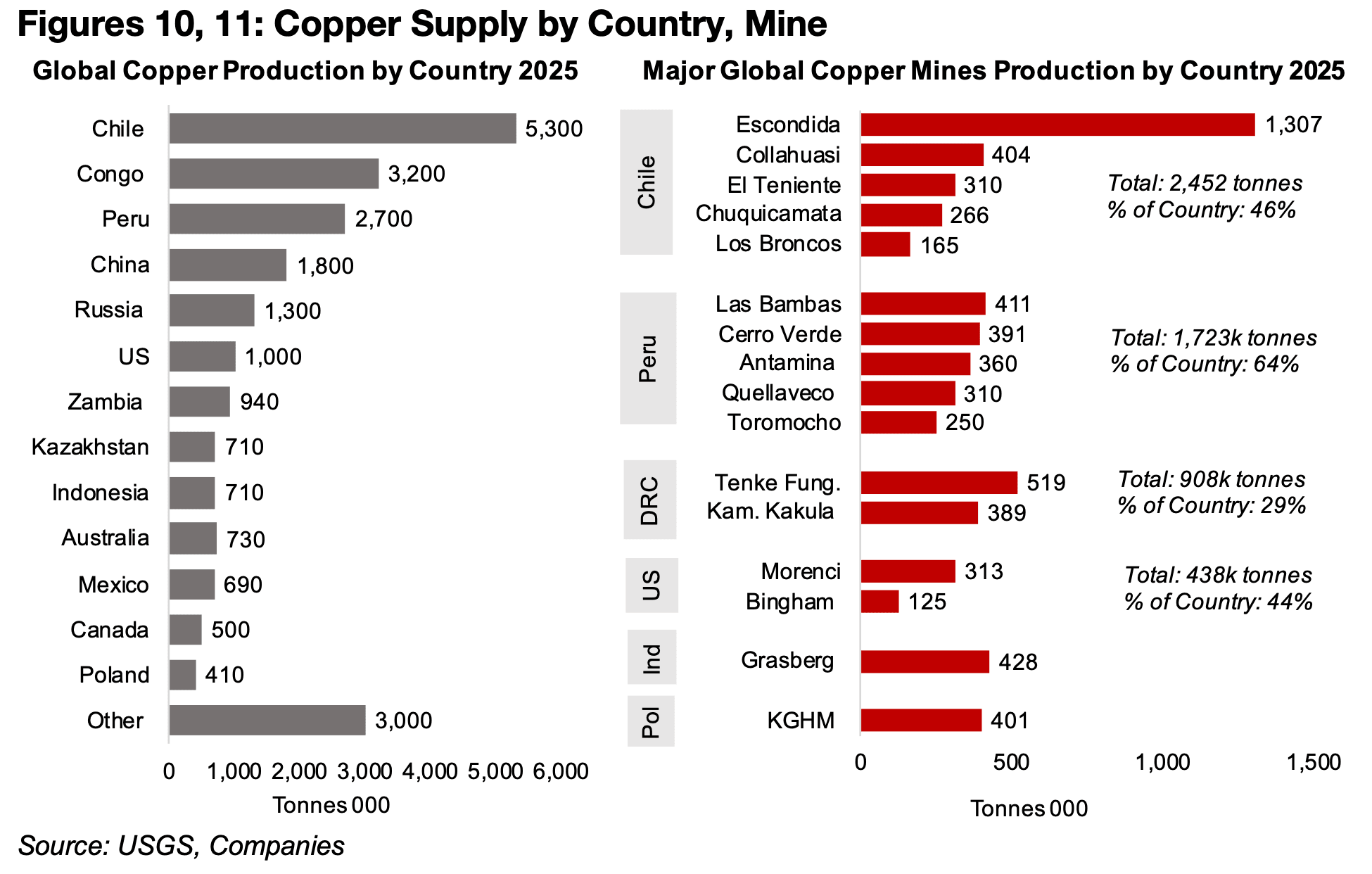

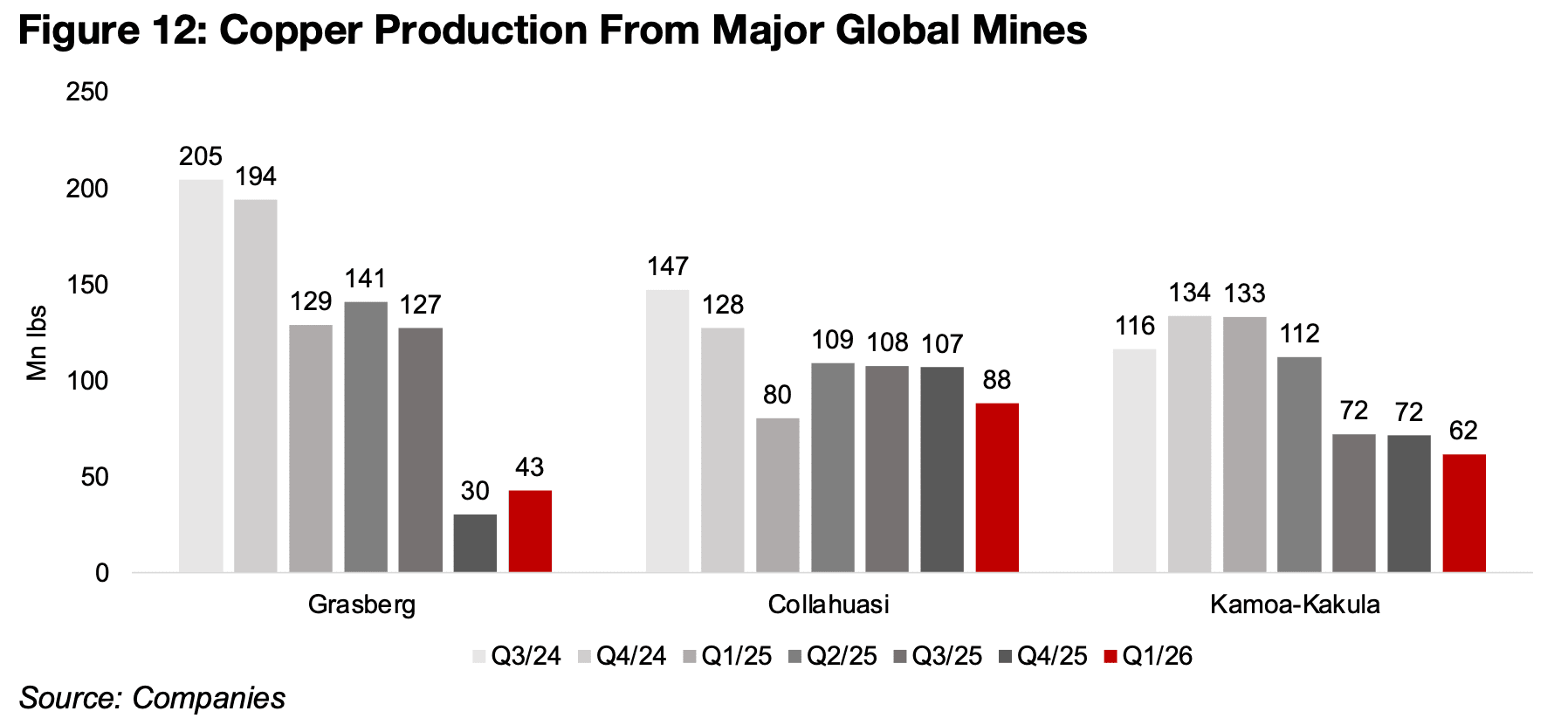

On the supply for copper, there is considerable scope for a rebound in production as

output has declined for several of the largest global mines over the past year, but the

issues causing the drop could start to be reversed in 2026E and 2027E. This includes

Grasberg, which had been the second largest producing copper mine in the world in

2024, but saw a huge plunge in output from Q4/25 after a mudslide in Indonesia

(Figure 9). However, the damage is expected to be repaired this year and production

could rebound substantially by 2027E.

There has also been relatively weak output from the second largest mines in two

major copper producing countries, Collahuasi in Chile, and Kamoa-Kakula in the

Democratic Republic of Congo. These two countries are by far the largest copper

producers globally, and it is expected that the operational issues driving the lower

output could potentially be corrected in the next few years (Figures, 10, 11). Another

major mine in Panama, Cobre, had been producing over 300k tonnes per year prior

to operations being suspended over regulatory issues, and the government is

currently considering restarting operations. A rebound from these mines could put

global copper production on track for expectations of a large rise in output next year.

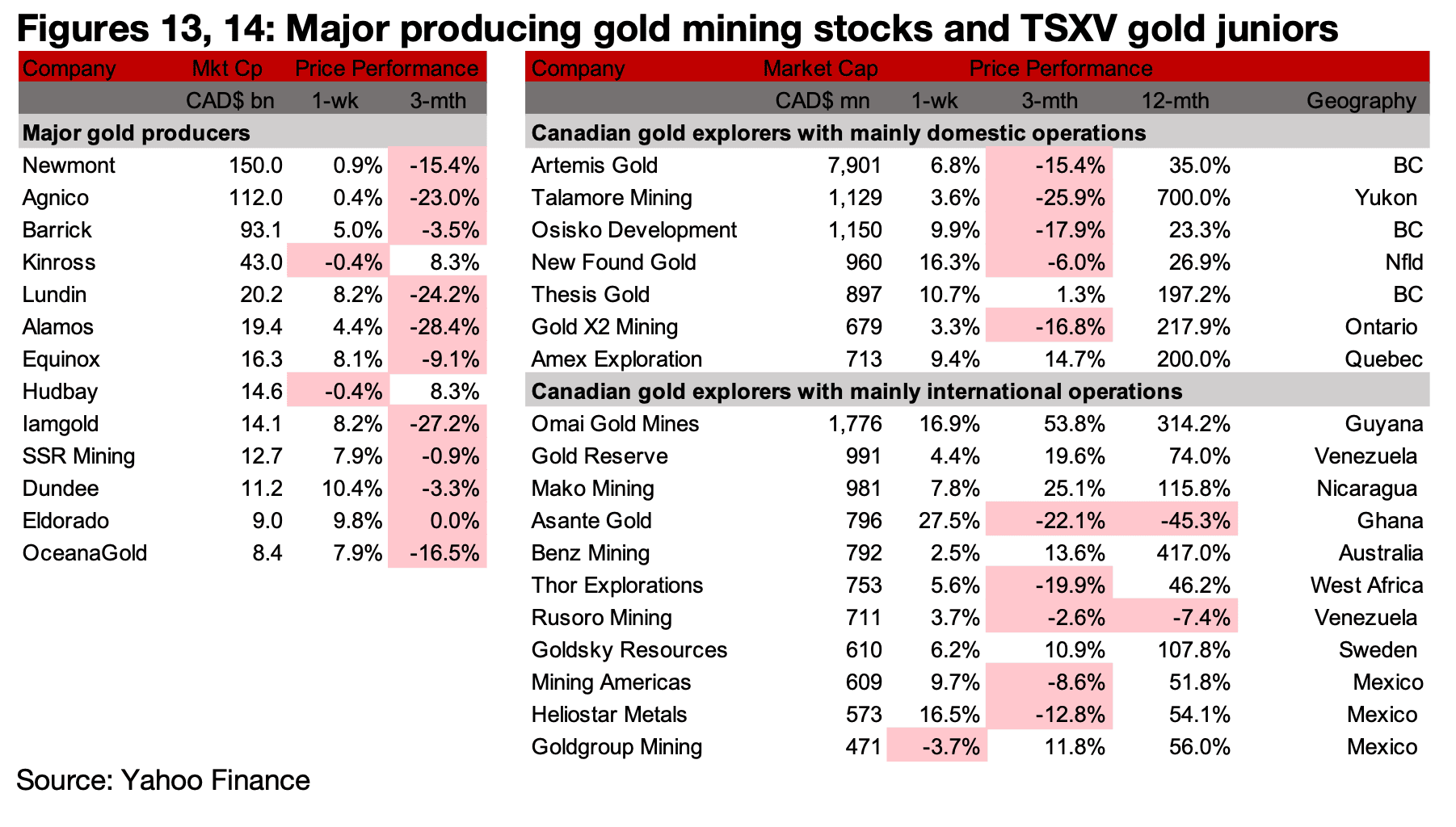

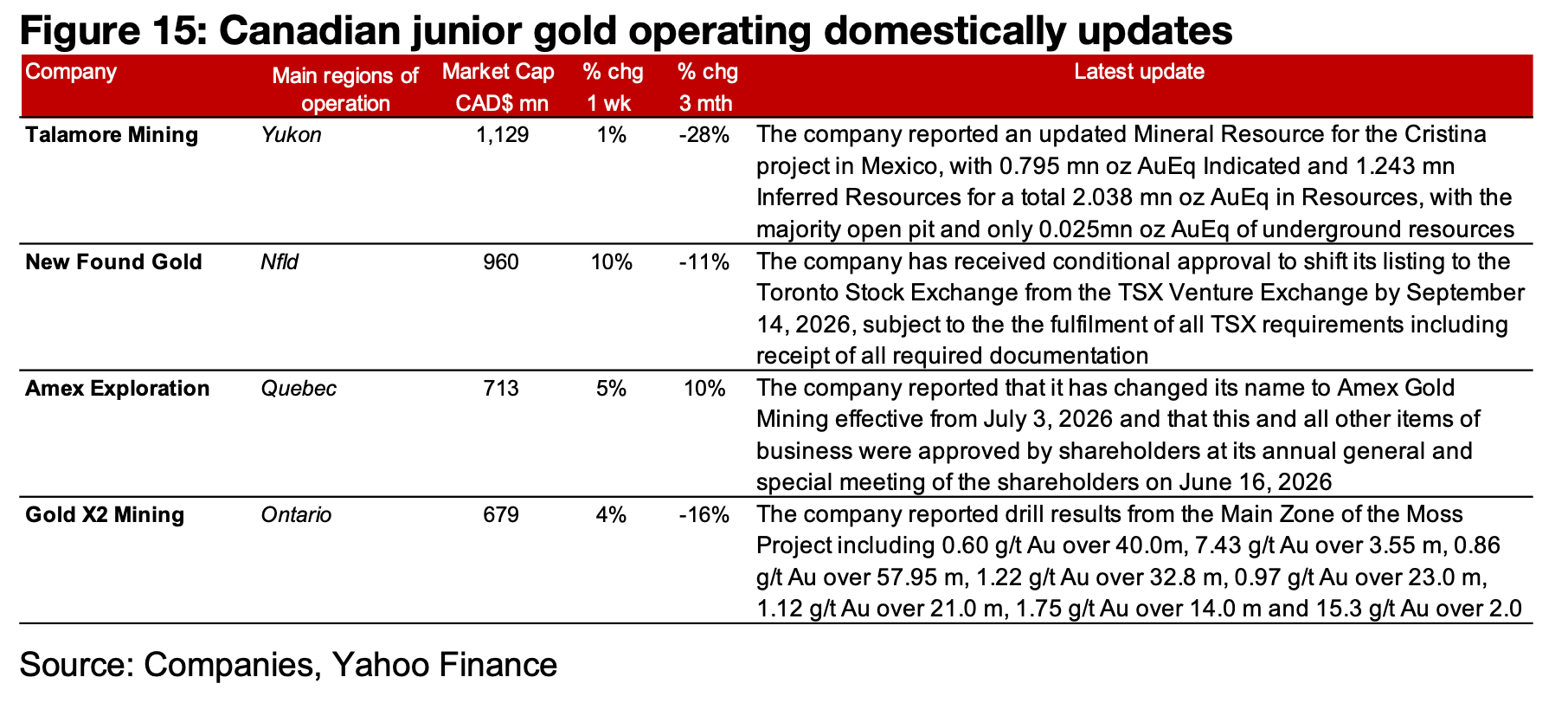

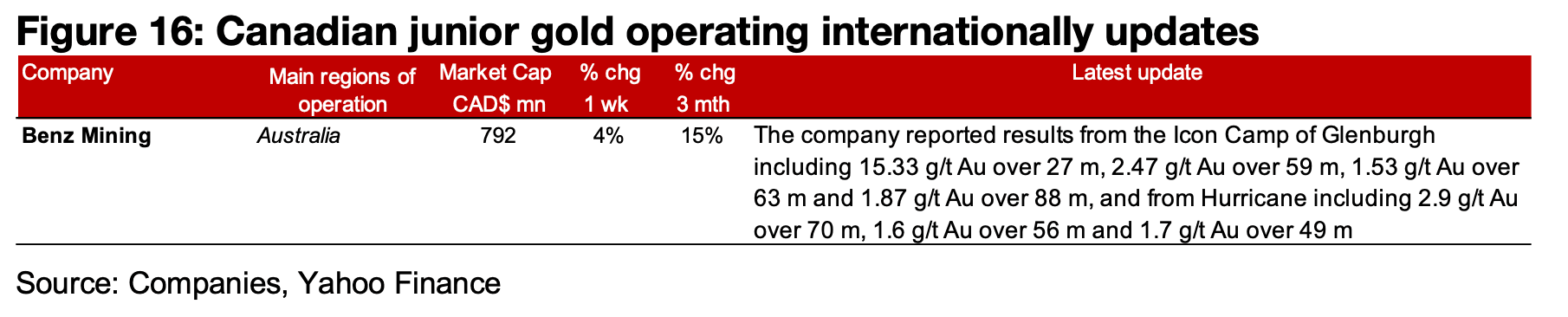

The major producers and TSXV large gold were almost all up on the rise in the metal price (Figures 10, 11) For the TSXV gold companies operating mainly domestically, Talamore mining reported an updated Mineral Resource for the Cristina project in Mexico, of 2.0 mn oz AuEq, which also includes Ag, Cu, Pb and Zn. This puts the project moderately below the total 3.0 mn oz AuEq Resources of its Coffee Project in the Yukon. However, Coffee is at a far more advanced stage than Cristina, with a PEA completed earlier this year, a Feasibility Study expected by the end of 2026 and permitting advanced. New Found Gold received conditional approval to shift its listing to the TSX from the TSX Venture Exchange, Amex Exploration changed its name to Amex Gold Mining and Gold X2 reported drill results from the Main Zone of the Moss Project (Figure 12). For the TSXV gold companies operating mainly internationally, Benz Mining reported results from the Icon Camp and Hurricane Camp of the Glenburgh project (Figure 13).

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.

Author

Ben McGregor authors the Weekly Roundup at CanadianMiningReport.com, providing sharp analysis of the metals and mining sector. With a talent for spotting trends, Ben distills complex market shifts into clear, engaging insights on TSXV junior miners. His weekly updates cover gold, copper, uranium, and more, blending data-driven perspectives with a knack for identifying opportunities. A vital resource for investors, Ben’s work navigates the dynamic junior mining landscape with precision.