June 22, 2026

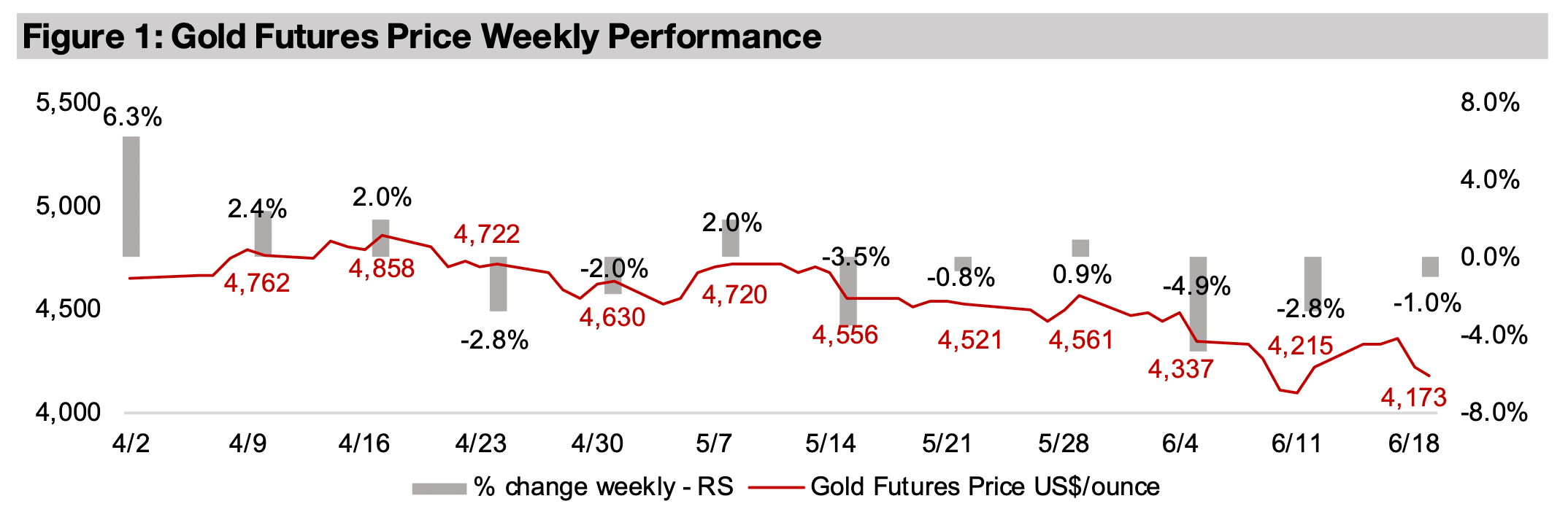

Gold dropped -1.0% to US$4,173/oz, a slower pace of decline than in the previous two weeks when the geopolitical risk premium priced into gold fell on expectations for the US-Iran peace deal realized this week, although the calm remains tentative.

Gold price targets for 2026 have been cut by many major investment banks, Gold Fields’ share price has been hit by Ghana debating renewal of the company’s license for a mine in the country and Alamos has cut estimates after an earthquake.

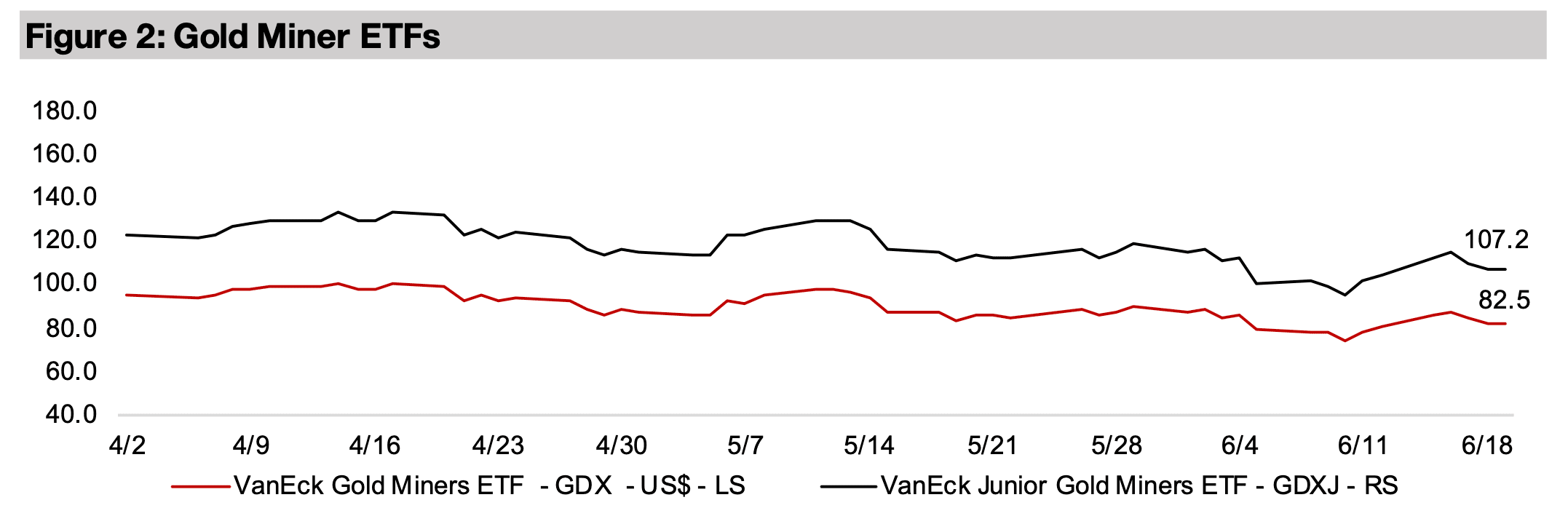

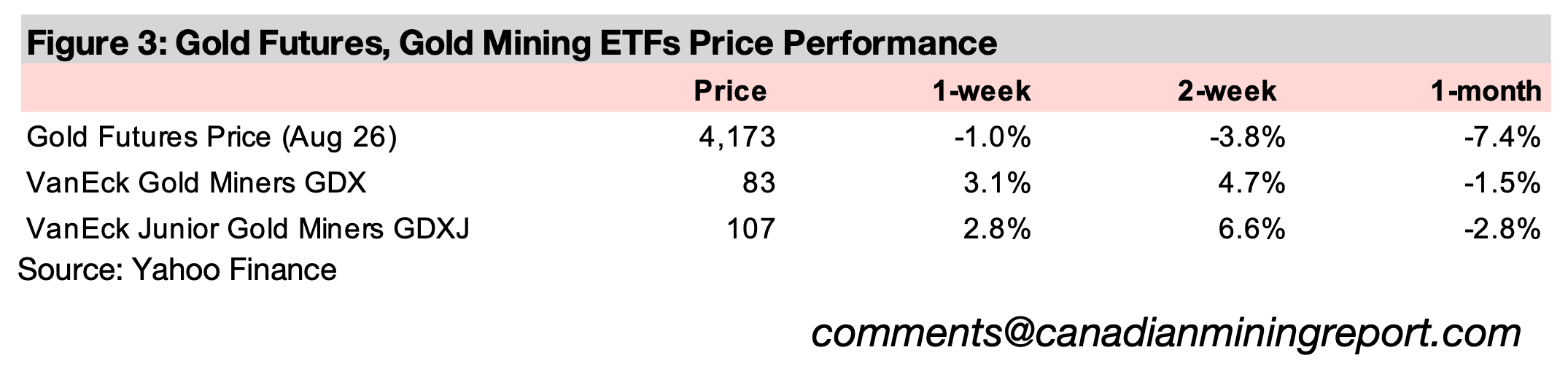

The gold stocks rose even as the metal declined for a second week, with the GDX up 3.1% and GDXJ rising 2.8%, while the decline in geopolitical risk boosted markets, with the S&P 500 up 1.2%, Nasdaq gaining 2.9% and Russell 2000 rising 1.7%.

The gold price dropped -1.0% to US$4,173/oz, down for the third week, -11.6% off

its recent peak of US$4,720/oz on May 8, 2026, and losing -21.5% so far for the year.

The rate of the metal’s decline slowed from the previous two weeks, which had seen

a large drop as the premium priced in for geopolitical risk contracted as the market’s

expectations for a US-Iran peace deal increased. The US announced the reopening

of the Straits of Hormuz on June 14, 2026, the countries signed an initial agreement

at the start of the week on Monday June 15, 2026, and then the formal deal on Friday,

June 19, 2026. As gold only edged down this week on this huge news, it implies that

the markets may view the drop in geopolitical risk as having been sufficiently priced

into the metal in its decline over the past few months.

The markets may also not be entirely convinced that the peace will necessarily hold

long-term, and as they have since 2025, continue to hedge to some degree with metal.

Already over the weekend, Iran made an announcement that the Straits of Hormuz

had one again been shut after Israel’s attacks on Lebanon, and it will likely be some

time before it is clear that tensions in the region have calmed. The markets seemed

focussed mainly on the peace deal with major economic news limited, and this drove

strong gains, with the S&P 500 up 1.2%, Nasdaq gaining 2.9% and Russell 2000

rising 1.7%. The gold stocks also gained, even as the metal price dropped, for a

second week, with the GDX rising 3.1% and GDXJ up 2.8%. This would seem to

indicate that the market views the valuations for gold stocks as having dropped below

even what would be implied by long-term averages for the metal price of around the

current US$4,200/oz level.

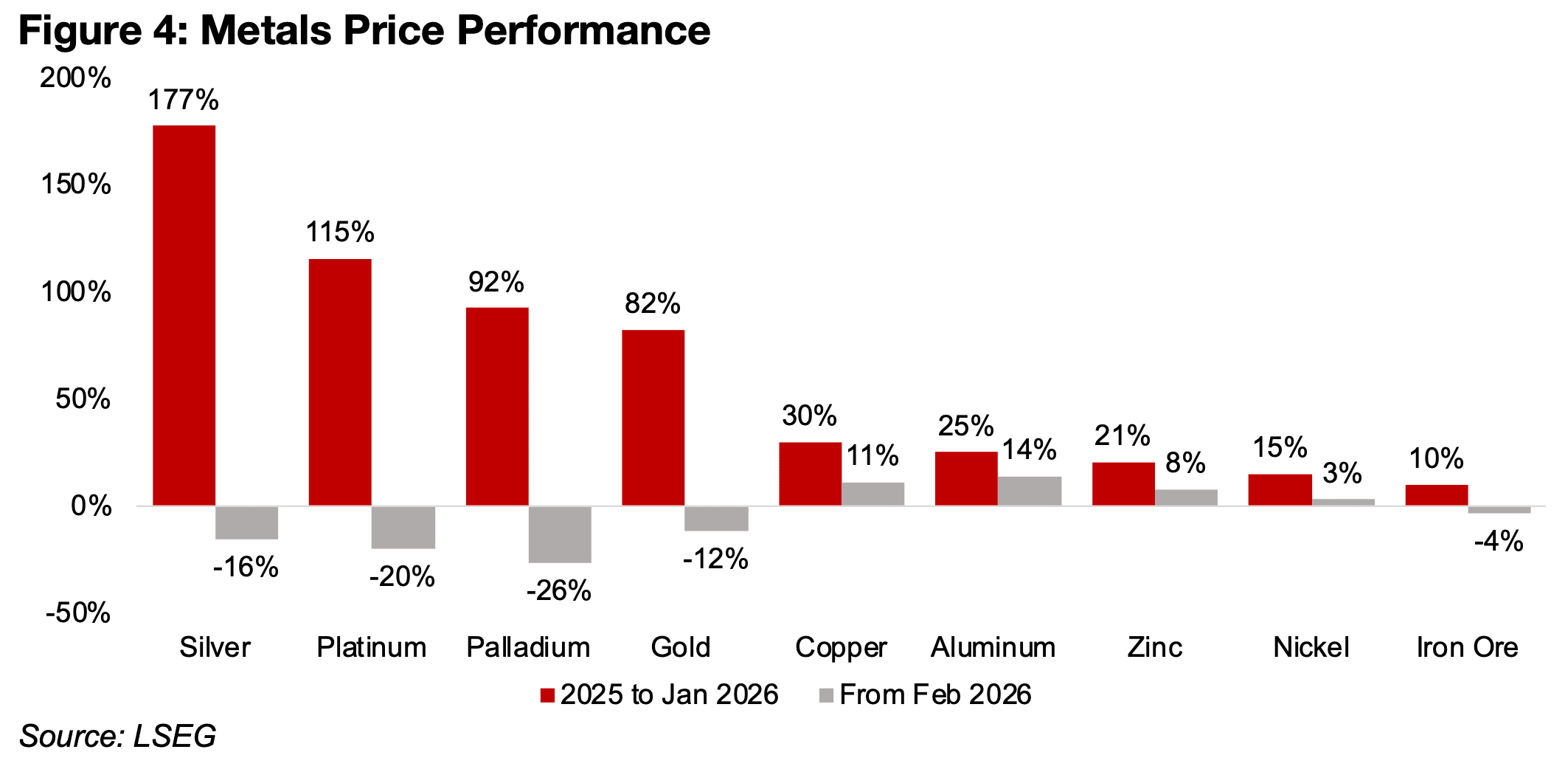

The other precious metals have also seen major weakness this year, with silver down

-16%, platinum losing -20% and palladium off -26% from February 2026 (Figure 4).

All three saw huge surges in late 2025 and into early 2026, and completely dominated

the market in the ‘long year’ from 2025 to the end of January 2026, with silver up

177%, platinum 115% and palladium 92%. However, the moves for all three had

become increasingly speculative by January 2026, and the weakness this year is as

much a continued unwinding of these previous excesses as it is driven by

fundamentals. Gold’s gains in the ‘long-year’ to January 2026 were also strong, with

an 82% rise, but this was somewhat more gradual over the whole period, although it

too was clearly seeing speculative activity near the end of the move.

The market has clearly shifted over to the base metals this year, which have

substantially outperformed precious metals since February 2026, with copper up

11%, aluminum 14%, zinc 8% and nickel 3%, with the only decliner, iron ore, down

just -4%. However, similar to the precious metals, the gains are moderate compared

to the ‘long-year’ of 2025, with copper up 30%, aluminum, 25%, zinc, 21%, nickel

15% and iron ore, 10%.

The decline in the gold price has seen the major investment banks slashing their gold

forecasts for this year over the past few months. Morgan Stanley took the lead as

early as April 2026 with an -8.8% drop to US$5,200/oz from US$5,700/oz previously.

This was followed in May 2026 by UBS, with a -6.8% cut in its US$5,900/oz target,

which had been the highest of the major investment banks, to US$5,500/oz. This

month two major banks have followed, with Goldman’s forecast down -9.3% to

US$4,900/oz from US$5,400/oz and Standard Chartered’s estimate dropping -11.3%

to US$5,100/oz from US$5,750/oz. Only Citigroup has maintained its target, at

US$5,000/oz, although this was already low compared to the other banks.

Macquarie’s forecast is by far the lowest, at US$4,323/oz, although it was released

in February 2026, and is now dated compared to the other banks, and likely to be

revised given the major macro changes since March 2026. The gold forecasts of other

institutions and forecasters are on average slightly below the investment banks, with

the World Bank at US$4,700/oz, Australia’s Office of the Chief Economist at

US$5,020/oz and Fitch Solutions at US$4,500/oz. Historically these organizations do

no tend to estimate major jumps in the gold price as this typically implies negative

economic outcomes.

The investment banks have mainly cited the shift from expectations for a global

monetary expansion prior to the Middle East conflict to a potential contraction since

as the key driver for the decline in their gold price forecasts. A rising money supply

over time tends to be gold’s key underlying driving, and if rates cuts do not come

through, this increase could slow, or there could be a decline if there are substantial

increases in rates. For the four regions with the largest monetary bases, two, the

European Union and Japan, have both already increased rates, with the US and China

still on hold so far this year.

However, the recent peace deal means quite an unclear situation for the path of

interest rates now. Oil prices could drop back to previous levels, and presumably this

would significantly reduce inflation, and once again leave the central banks room to

cut rates. However, there is the issue that the inflation that was already unleashed

globally still feeds through the global supply chain over the next few months and

boosts prices overall. This could drive demands for higher wages, and start a wageprice inflation spiral, as prices had been relatively high for an extended period even

prior to the jump in oil prices, and now appear to be to putting significant pressure

on the global consumer. There is also the big question of whether the peace holds,

with a resumption of the conflict sending the oil price, and inflation, up again. This

will make it quite difficult for central banks to make major moves in rates either way,

and the unclear geopolitical situation looks set to persist certainly through to the end

of this year.

Ironically these cuts in gold price targets could actually be a bullish signal, however,

for the gold price. The investment banks all the way through the gold bull market from

2019 to 2025 had targets that significantly lagged the realized gold price, and it has

only been in late 2025 and 2026 that they had finally boosted prices enough to get

ahead of the gold price for the first time. This also came around the time of the

increasingly speculative and unsustainable gold boom of late 2025 and into early

2026 that saw a huge move by retail investors into the metal, which had become a

very crowded, consensus trade. That the gold trade has become less popular could

actually offer an opportunity for long-term gold investors that made large purchases

when the metal was far under US$4,000/oz.

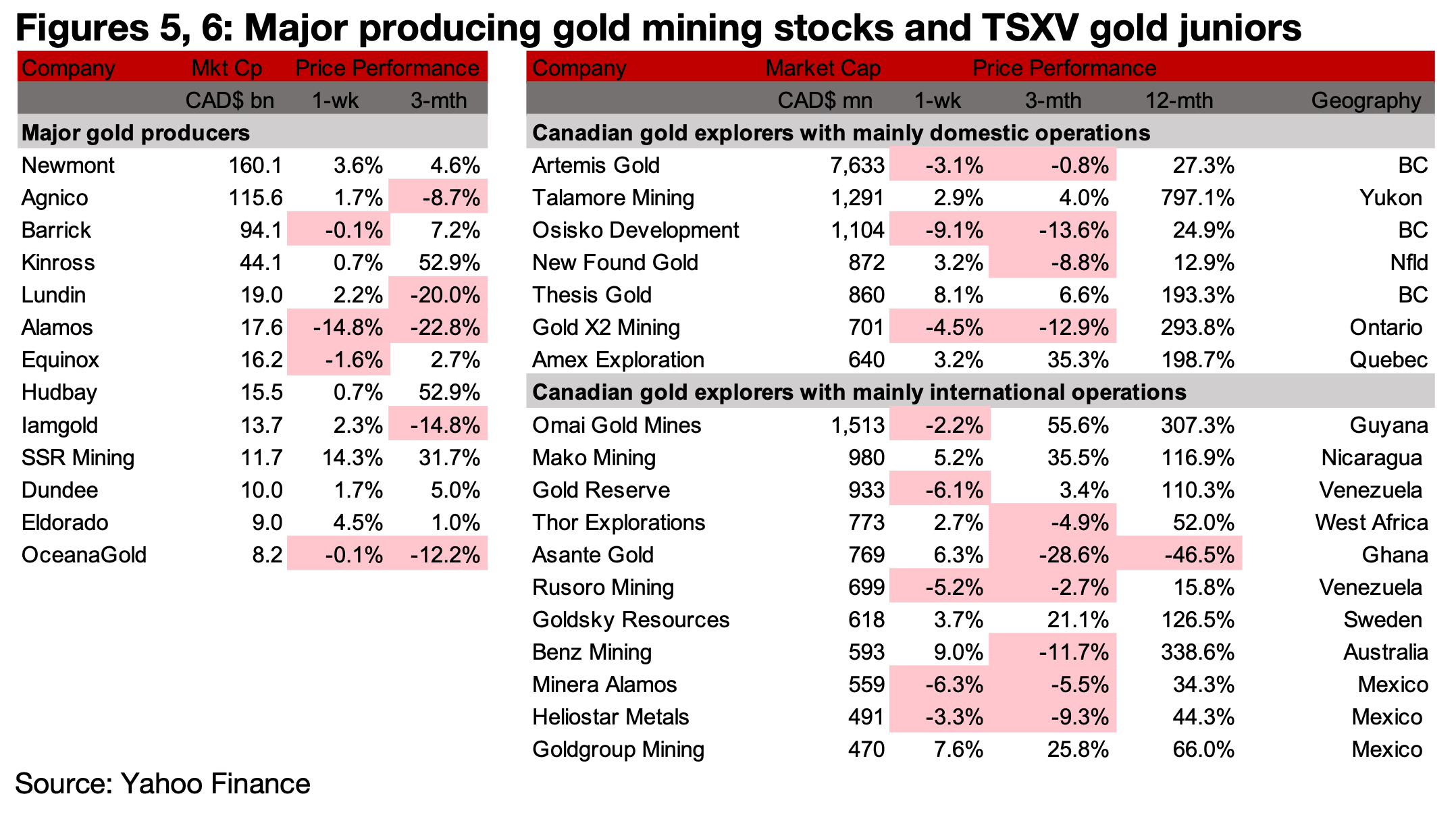

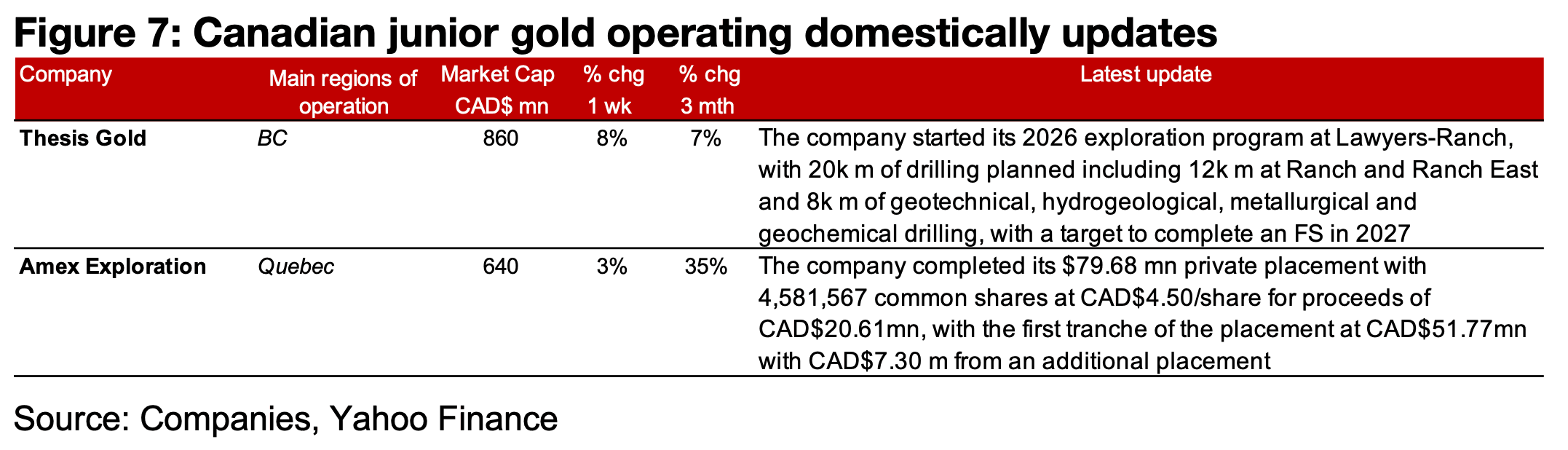

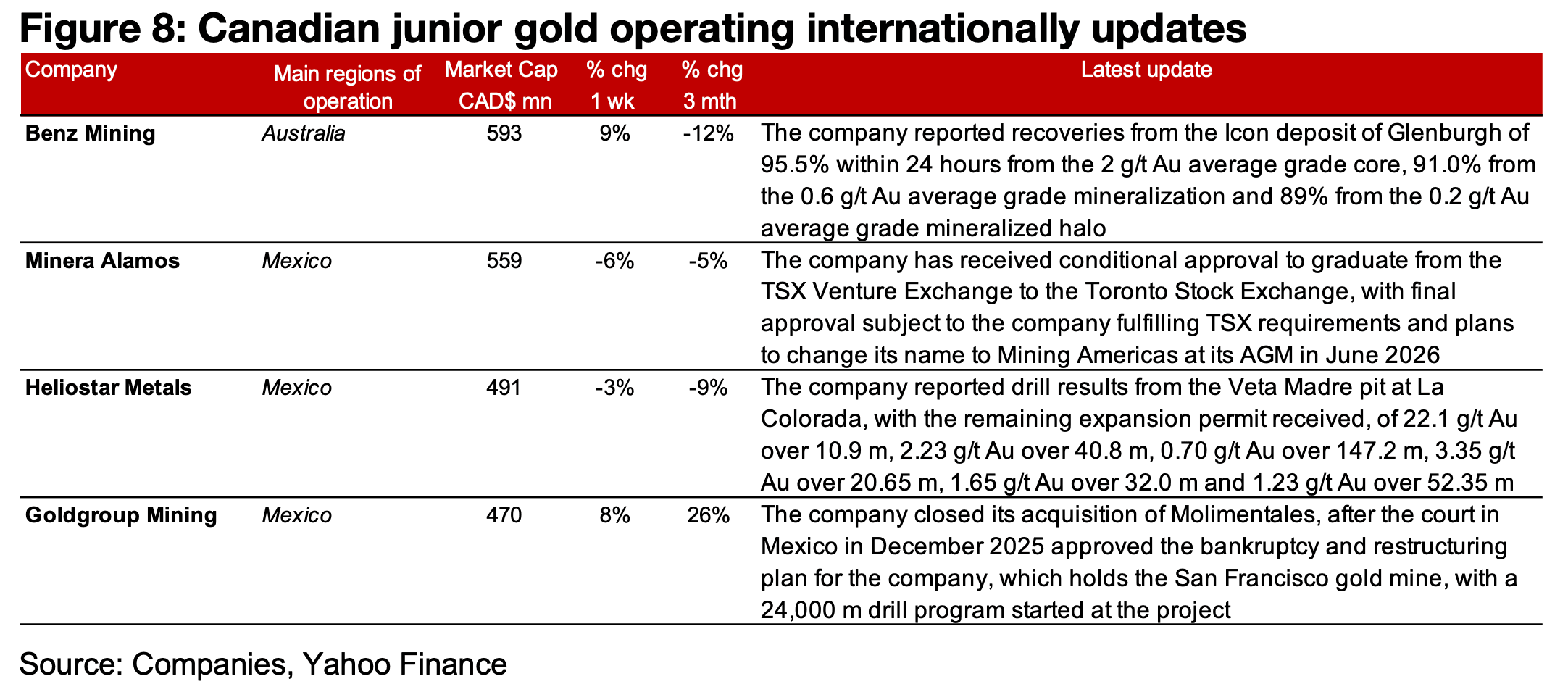

The major producers and TSXV gold were mixed as the metal price edged down (Figures 5, 6) For the TSXV gold companies operating mainly domestically, Thesis Gold began its 2026 exploration program at Lawyers-Ranch with 20,000 m of drilling planned to support a Feasibility Study by the end of 2027. Amex Exploration completed its private placement for proceeds of CAD$79.68mn, with a second tranche of US$20.61mn, after a first tranche of CAD$51.77 and additional placement of CAD$7.30 mn (Figure 7). For the TSXV gold companies operating mainly internationally, Benz reported recoveries from the Icon deposit of Glenburgh, Minera Alamos received conditional approval to graduate to the TSX from the TSXV and plans to change its name to Mining Americas at its June 2026 AGM. Heliostar reported drill results from the Veta Madre pit at La Colorada, and received the remaining expansion permit, and Goldgroup completed its acquisition of Molimentales, which holds the San Francisco gold mine, with the company having started a 24,000 m drill program at the project (Figure 8).

The largest decline this week for the major Canadian producers was from Alamos,

which dropped -14.3% after an earthquake damaged its Young-Davidson mine in

Ontario. This has stopped the company from being able to mine ore that had been

targeted for Q2/26. While the Young-Davidson mine is the company’s smallest, at

174k oz Au it was still 30.7% of output in 2025, as its three mines are relatively close

in production, with the largest, Mulatos, at 205k oz Au last year and the second, Island,

at 188k oz.

The company’s full year guidance was previously for 570k-650k oz Au for 2026, which

implies about 142k-163k oz per quarter. However, the company has revised down its

Q2/26 guidance to 130k-135k, or by -8.8% and -16.9% for the two estimates. It also

expects that its full year production will now come in under the 570k oz lower estimate.

The decline from Young-Davidson has been partly offset, however by strength from

Island. The company has also indicated that costs will be ahead of the previous

guidance for the 2026 and that it would provide a further update on the YoungDavidson in July 2026 after the situation had been fully assessed.

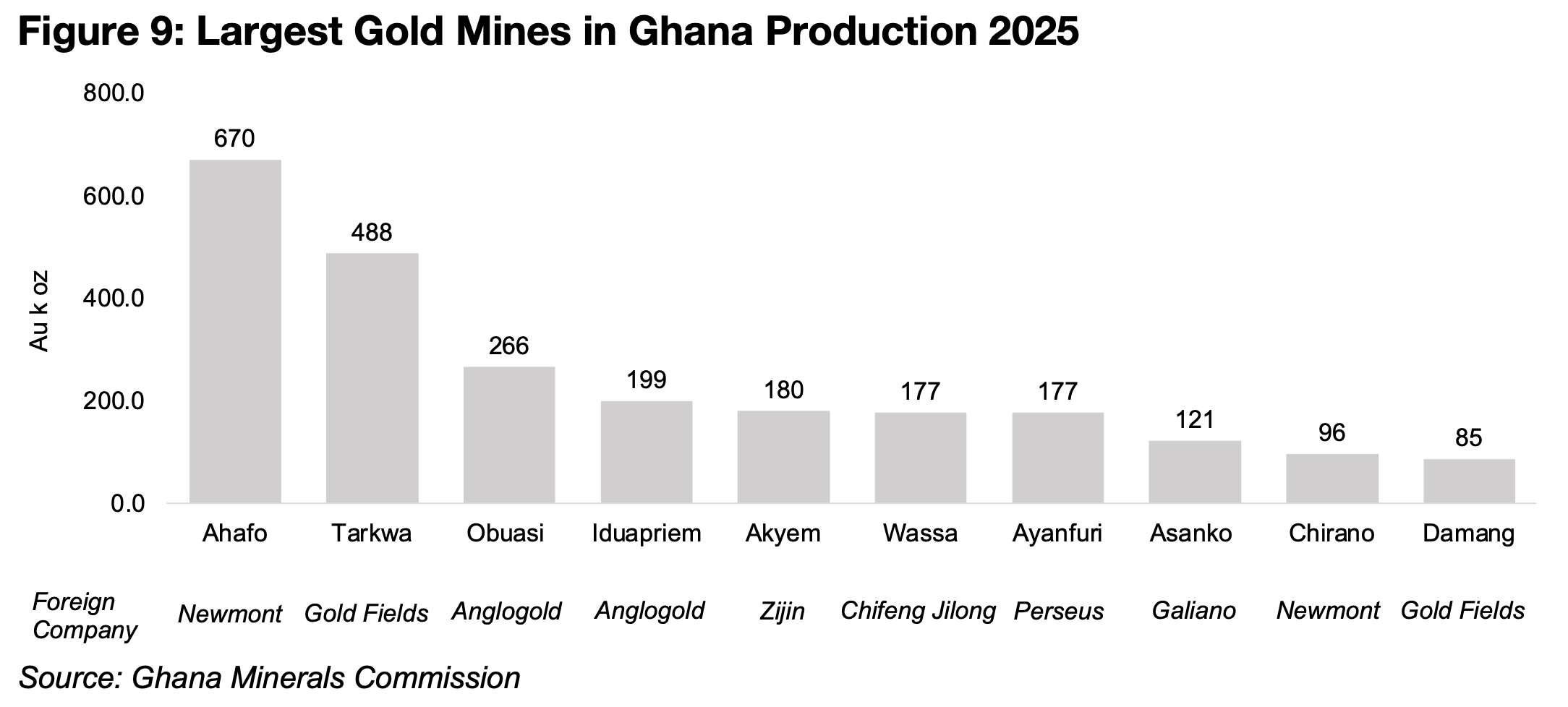

Another of the largest global gold producers, Gold Fields, saw major volatility in its

share price this week, with a 12.6% gain through to Wednesday, but then an -16.3%

decline on Thursday, which it saw it down -5.8% for the week overall. The decline

came after Ghana announced that it may not necessarily renew the company’s lease

on the Tarkwa gold mine, which was the country’s second largest producer of the

metal in 2025, at 488k oz Au (Figure 9). This has been part of a broader trend of the

government pushing for more increased domestic participation in the sector. This

included major new regulations in December 2025 that required local contractors to

be hired for the operations of foreign-owned mines by December 2026. The country

has also declared that open pit mining will now be 100% domestically owned, with

underground mining 50% or more controlled by Ghanian companies. The country is

also proposing scaled mining royalties as high as 12% from the current 5% flat rate

and could reduce leases for mining to 15 years from 30 years.

All of the major gold mines in Ghana have large foreign ownership, with Goldfields

also operating Damang, the tenth largest gold producer in the country, at 85k oz in

2025. Newmont is a major shareholder of the largest mine in the country, Ahafo, with

output of 670k oz Au in 2025, and the ninth largest, Chirano, at 96k oz, and Anglogold

operates Obuasi and Iduapriem, with production of 266k oz and 199k oz. China has

also become a major gold producer in Ghana, with Chifeng Jilong purchasing the

Wassa mine in 2022, which had output of 177 oz Au in 2015, and Zijin buying Akyem

in 2025 from Newmont, which had production of 180k oz Au. The other two major

major mines in Ghana, Ayanfuri and Askanko, are operated by Australia’s Perseus

and Canada’s Galiano Gold, with output of 177k oz Au and 121k oz Au in 2025.

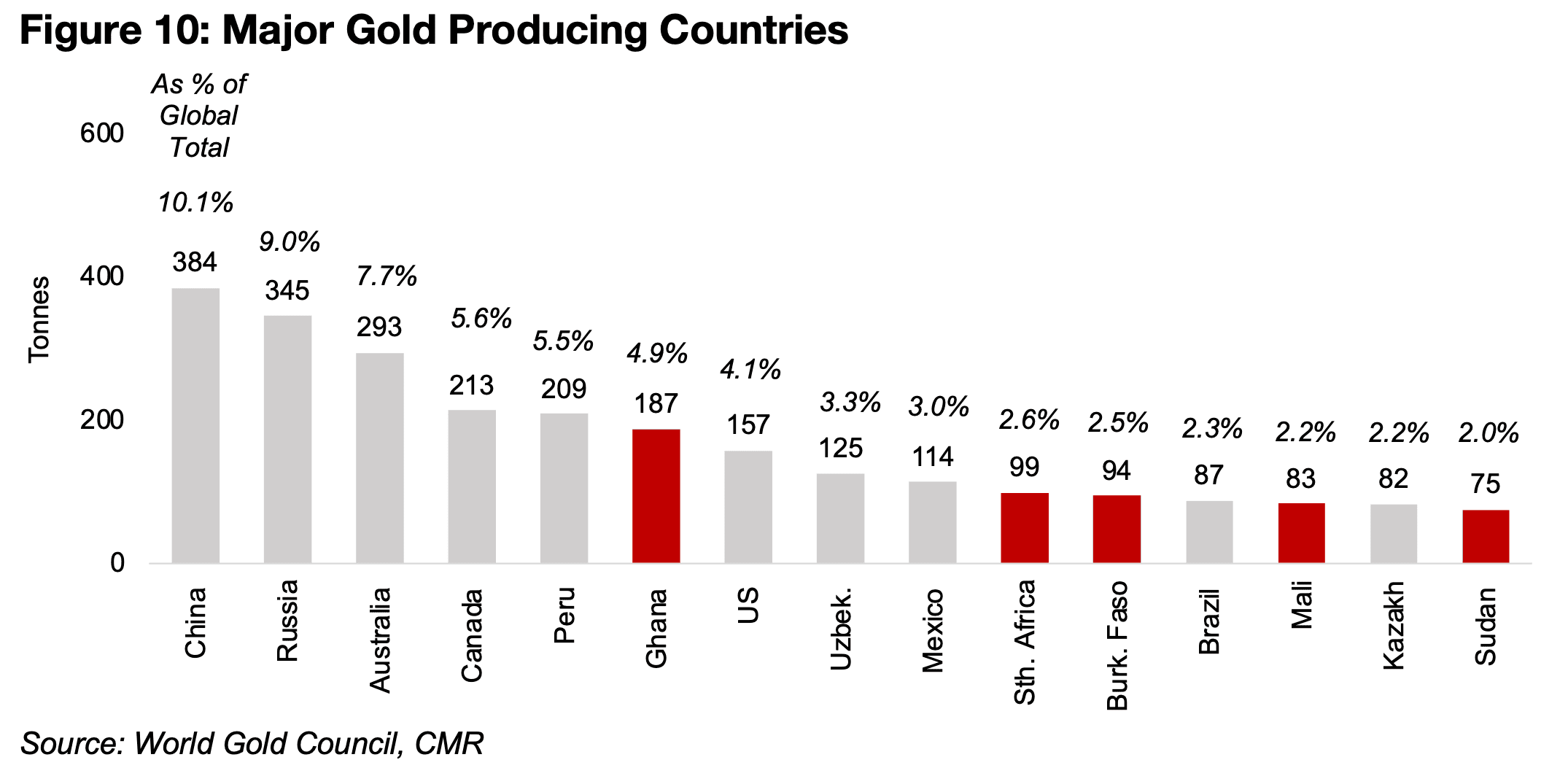

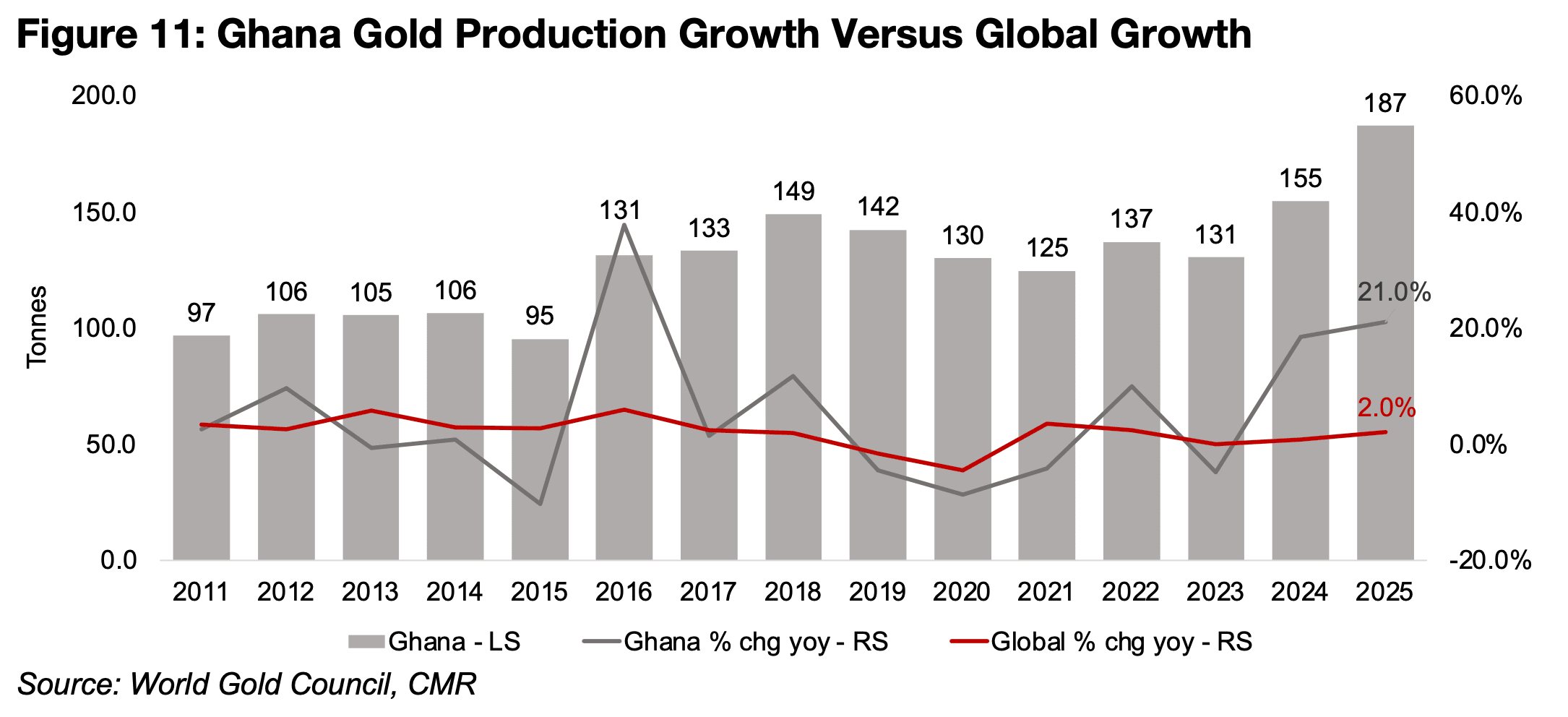

Ghana has become an increasingly important global gold producer, the sixth largest

at 4.9% of the total, and only moderately behind Canada, at 5.5% (Figure 10). This is

up from around only 100k oz Au per year from 2011 to 2015, with a rise to around an

average 135k oz Au from 2016 to 2023, and the last two years seeing especially large

gains to 155k oz Au in 2024 and 187k oz Au in 2025. The growth rate for Ghana’s

gold production in 2025, at 21.0%, far outpaced the 2.0% rise in world output overall.

The changes in Ghana follow more severe developments in the rest of West Africa

with regards to resource nationalisation, including Burkina Faso and Mali, which have

both had recent coups. These two countries are important for the gold industry as

they are the eleventh and thirteenth largest producers globally.

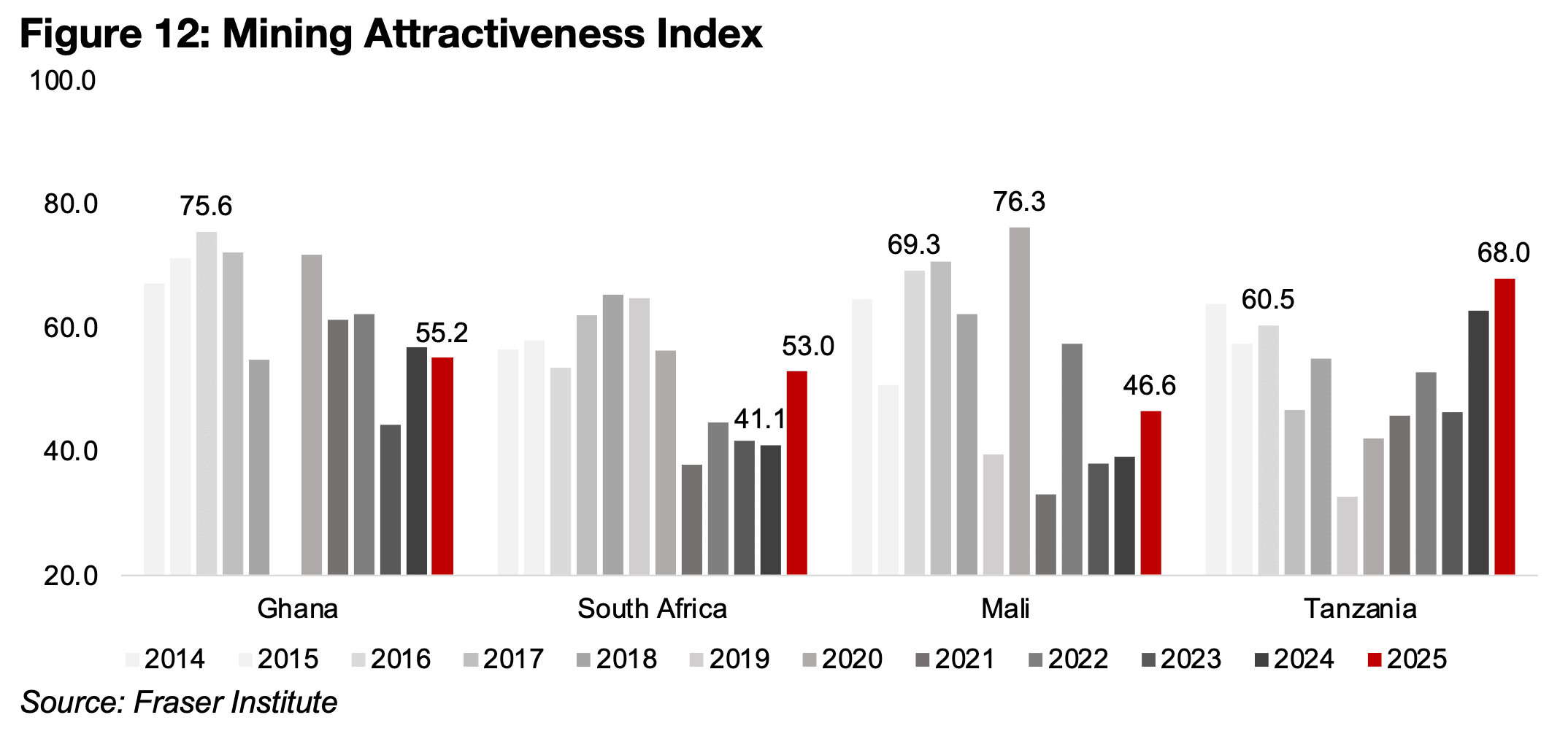

The degree of nationalisation has varied across the countries with the changes in

Ghana viewed as more gradual and accommodating of foreign companies than the

direct seizure of mines that has occurred in Burkina Faso. Mali has increased the

government’s holding of new mining projects to 30% from the previous 20%. The

Mining Investment Attractiveness Index for both Ghana and Mali have declined

substantially from their peaks in the late 2010s at 75.6 and 76.3, respectively, to just

55.2 and 46.6 in the 2025 Fraser Institute Mining Survey.

Disclaimer: This report is for informational use only and should not be used an alternative to the financial and legal advice of a qualified professional in business planning and investment. We do not represent that forecasts in this report will lead to a specific outcome or result, and are not liable in the event of any business action taken in whole or in part as a result of the contents of this report.

Author

Ben McGregor authors the Weekly Roundup at CanadianMiningReport.com, providing sharp analysis of the metals and mining sector. With a talent for spotting trends, Ben distills complex market shifts into clear, engaging insights on TSXV junior miners. His weekly updates cover gold, copper, uranium, and more, blending data-driven perspectives with a knack for identifying opportunities. A vital resource for investors, Ben’s work navigates the dynamic junior mining landscape with precision.